Luxury market outperforms the wider market.

Article

The market has been largely focussed on the US Election over the past month – and is now dealing with a fundamental change with the election of Donald Trump as President.

Welcome to our monthly market update.

The market has been largely focussed on the US Election over the past month – and is now dealing with a fundamental change with the election of Donald Trump as President. There has been wild swings on global markets in the aftermath of the election – as the market was wrong-footed and surprised by the result. This continues the theme that middle-class workers are feeling disenfranchised by globalisation and the outsourcing of jobs and income inequality that has developed. Investors now have to deal with a new regime and need to interpret what has been said in the Trump campaign and what is likely to be implemented. While there will be undoubtedly positives for the US economy from the Trump policies, the impact on global financial markets and trade are less clear. Any impact on global trade will have a large impact on our trading partners and the Australian equity market.

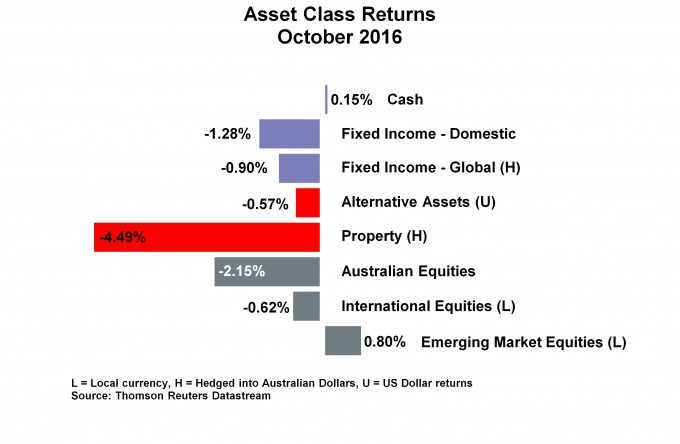

Equities: We remain underweight Australian equities. The President Elect has campaigned strongly on re- negotiating trade deals with China, Japan and South Korea in our region. These are our largest trading partners and any slow down in their exports to the US is likely to impact on their demand for our resources. In general, the reversal of the globalisation trend is unlikely to be favourable to a country as heavily exposed to the traded-goods sector as Australia. Also bank earnings growth was very soft in the recent reporting season and the fear is that regulators will continue to push for higher capital requirements in 2017. This is also likely to weigh on the Australian equity market. We have remained neutral on international equities despite this uncertain period. US growth could benefit from higher infrastructure spending and cuts to corporate tax rates should help US corporate earnings. Emerging markets are likely to be under considerable pressure as funds return to the US and the full extent of trade restrictions are revealed.

Fixed income: We continue to be underweight fixed income. Bond yields have pushed higher on the election result as the prospects of higher fiscal spending in the US, and more restrictive trade policies, are likely to lead to a period of higher inflation (or at least higher inflation expectations) and higher government debt. With the recent reversal in language by the ECB and BoJ hinting at prospect of tapering their quantitative easing programs (and relying more on fiscal spending), this is likely to see bond yields continue to rise in those regions. While it is not expected that we see a 1994-style bond market sell-off, the prospects are for bond yields to continue to rise over the next few years

Property: We remain underweight property. With bond yields rising, property has started to underperform and we believe this trend should continue. While we are not anticipating a major shock to global bond yields, property valuations remain elevated and are vulnerable to the rotation away from yield-sensitive sectors.

Alternative assets: Although equity market volatility typically drops after US elections, we expect that it may remain elevated for a few more months due to the heightened levels of US policy uncertainty. This is an environment that should suit many alternative asset strategies. We continue to expect that strategies targeting returns that are non-correlated with the major asset classes should continue to add value to portfolios and we remain overweight in both defensive and growth alternatives.

Currency: The Australian Dollar has benefited from low US interest rates and Chinese stimulus and mine closures that boosted iron ore and coal prices. However, we expect that the Australian Dollar will moderate against the US Dollar over the next year as US inflation rises, the Fed tightens policy and US companies repatriate foreign earnings. Furthermore, any slowdown in Asian exports to the US would be likely to place downward pressure on demand for commodities.

What’s changed in October?

October was a challenging month for investors with both bond and equity markets declining as investors worried about higher interest rates in the United States as well as the US election outcome.

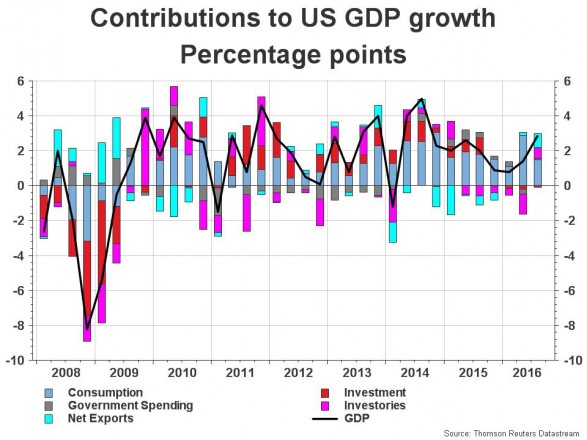

Leaving aside the macro-economic implications from the recent US Election, the economic data in the United States has been more or less in line with expectations. The initial estimate of third quarter GDP growth showed annualised growth of 2.9%, which was the strongest rise in two years, although it was helped by some one-off factors. The October non-farm payroll figures were also relatively robust with evidence of higher wages growth and the broader U-6 measure of unemployment, which includes people marginally attached to the labour force, fell to new post-financial crisis low of 9.5%. The recent data, showing moderate economic growth, has meant that markets have priced in an 80% chance that the US Federal Reserve lifts interest rates in December.

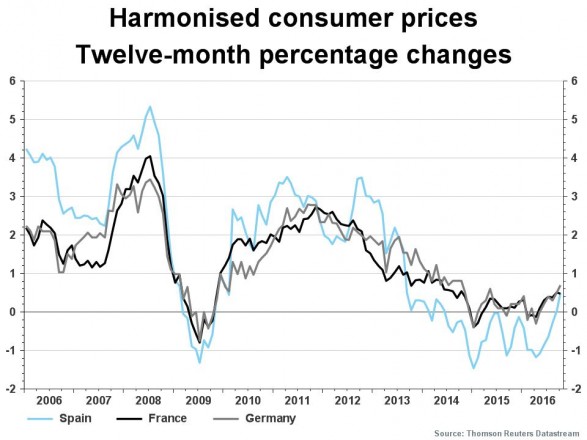

In Europe, GDP growth in the third quarter was as expected, at 1.6% year-on-year. However, purchasing manager indices for both the manufacturing and services sectors were better than expected. Industrial production in Germany, France and Spain also grew more strongly than expected and consumer price inflation, which had been very weak, appears to have picked up in countries such as Spain.

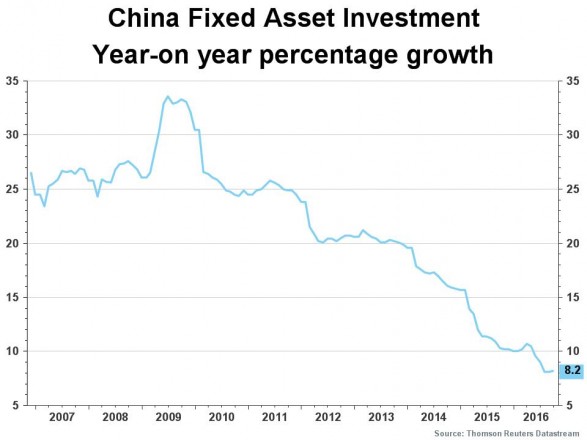

In China, the economy grew at an annual rate of 6.7% in the third quarter, which was as expected. Economic growth is being supported by fixed asset investment which grew 8.2% year-on-year in September, helped by strong credit growth and a booming property market, which policymakers are expected to reign in, particularly in cities such as Beijing, Shanghai and Shenzhen.

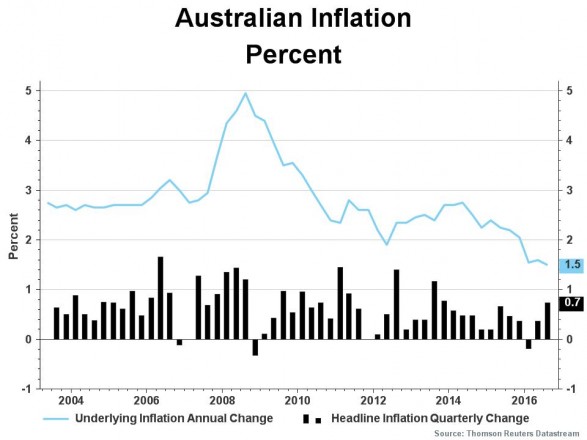

In Australia, employment fell for the second consecutive month in September and the trend continues to show weakness in full-time employment, partly offset by strength in part-time jobs. Although the unemployment rate fell to 5.6%, the employment data continues to show that there is some spare capacity in the labour market which is keeping a lid on wages growth. Soft wages growth is also helping to hold down the rate of inflation. CPI data for the third quarter showed that the underlying rate of inflation was 1.5% per annum, which is below the RBA’s 2-3% target range.

Luxury market outperforms the wider market.

Article

You don't have to be an expert stock picker to get the long term returns you expect from your share investments. We delve into the simplicity of Index Investing

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.