Households to feel the squeeze if the RBA follows the market path

How high rates will go in this cycle is a key question that is being asked by clients. Much of the debate has centred around where central banks see the neutral rate. We have previously published on this topic with the model-based estimates likely seeing a nominal neutral rate around 3%, while market proxies of terminal (i.e. the peak of the cash rate cycle) such as 5Y1Y FWD OIS are now at 2.7%. RBA Governor Lowe has mused that he hopes the real neutral rate is not negative, putting nominal neutral >2.50%.

In this note we abstract from the above theoretical models and focus on the household cash flow channel, principally looking at what the market path of interest rates means for mortgage payments. We make several simplifying assumptions, including the banking sector matching changes in the RBA cash rate in variable mortgage rates. We also do not distinguish between variable and fixed with around 70% of fixed rate loans expiring between now and December 2023; fixed rate loans comprise 38% of loans.

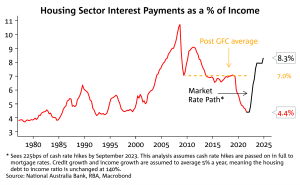

Our analysis finds that passing on the 225bps of rate hikes that markets have priced between now and September 2023 would lift housing interest payments as a share of household income to the highest level since September 2012. The housing interest payment share on our modelling increases to 7.9% of household sector income from its current 4.4%, meaning there would be a 3.5 percentage point increase in the ratio. The average during 2009-2021 was 7.0% and prior to the pandemic stood at 5.7%.

While it is clear the household sector will be able to service a higher mortgage rate (especially given APRA’s minimum serviceability buffers), a rise in interest payments relative to income of 3.5 percentage points will have to be financed by a reduction in saving and/or lower consumption than otherwise unless the economy remains very strong and wages growth accelerates considerably.

What does this mean for neutral? It is unclear given household cash flows are just one transmission mechanism for monetary policy and the economic backdrop also matters. Household mortgage interest payments approached 11% of household income in the mining boom just prior to the GFC, when the unemployment rate last got to 4% and wages growth was running considerably hotter at 4½% compared to 2¼% currently.

As an alternative exercise, we modelled what interest rate increase would be required to see housing interest payments lift to their long-run average as a share of income. This implied a smaller 175-200bps worth of hikes. Much of the analysis on whether the household cash flow channel proves restrictive is dependent on household income growth assumptions. In our analysis we have assumed 5% y/y growth. Of course, rates may need to go beyond neutral if inflation remains high and the economy is strong.

Not considered in this analysis is the sharp accumulation of household savings during the pandemic (households have accumulated some $240bn in deposits, though much of the rise in deposits is likely held by households who do not hold a mortgage as offset balances have only risen by $50bn during the pandemic). Households in aggregate are also around four years ahead on their mortgage repayments.

Chart 1: If the RBA follows the market path for rates, interest payments as a share of income will hit their highest level since 2012. Note in 2012 wages growth was running at 3.8% y/y, considerably hotter than the current 2.2%

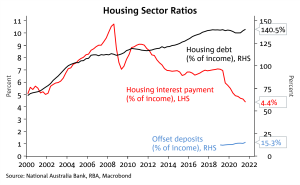

Chart 2: The post 2012 period saw a large divergence between housing debt and housing interest payments, driven by the decline in the RBA cash rate from 4.75% in 2011 to the current 0.10%.