Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

The Australian Budget is set to be unveiled next Tuesday night, ahead of the federal election that must be held on or before 21 May 2022.

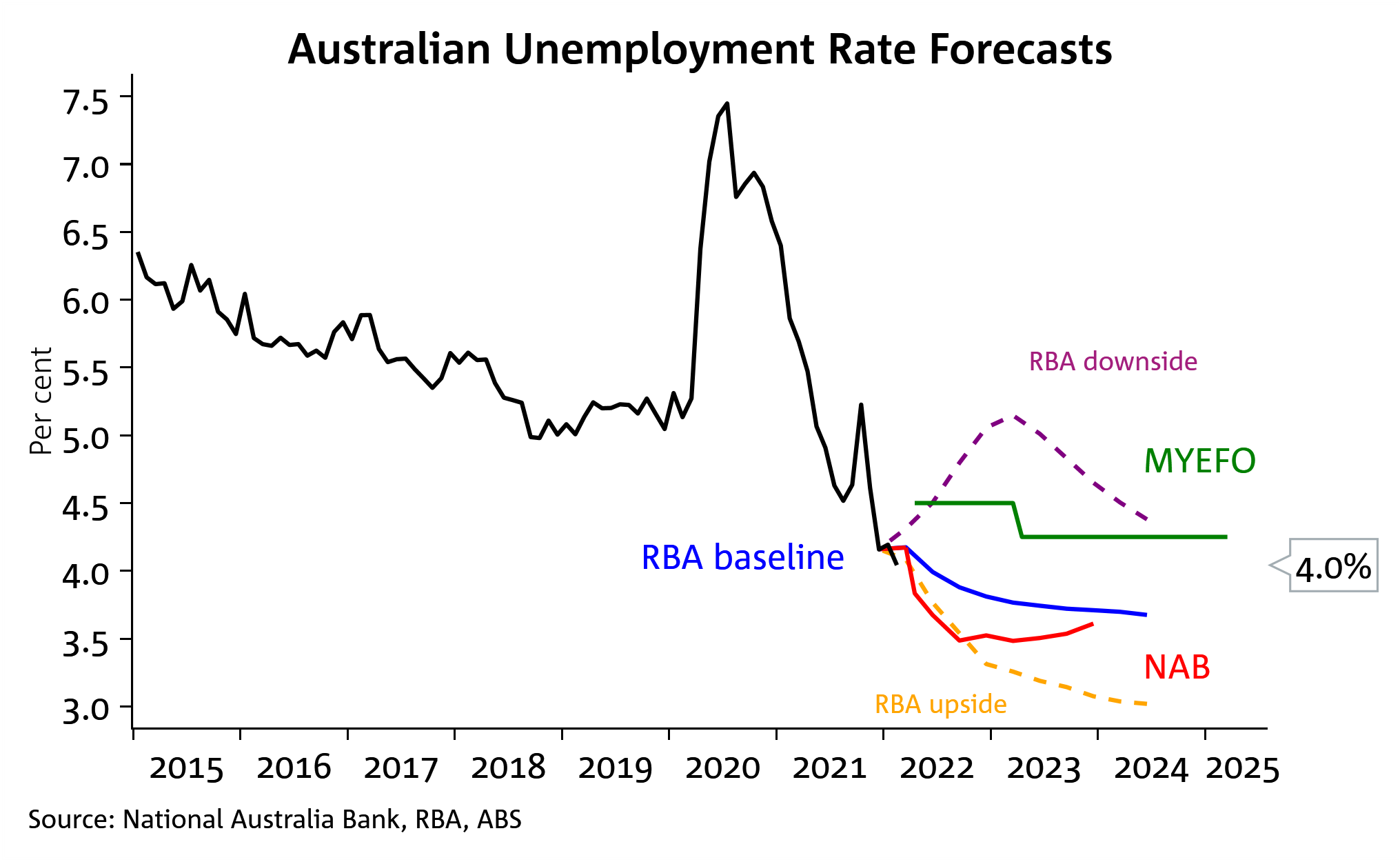

Chart 1: Economy has performed much better than expected than in MYEFO

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Labour market strong, housing supply falling behind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.