While we can debate the pros/cons of individual policies, the key message is the profound shift in the government’s fiscal strategy to even more willingness to extend the bridge to the recovery.

The 2020-21 Budget is set to record a deficit of around $200bn, up from a deficit of $85.3bn in 2019-20, while Treasurer Fyrdenberg has indicated the budget will be in deficit over the forward estimates (i.e. over the next four years). This “first phase” of deficits is expected to last until “the unemployment rate is comfortably back under 6%”. In this phase the automatic stabilisers will be allowed to work, fiscal support will be temporary and proportionate, while there will be likely structural reforms.

As for possible measures, the press suggest: bringing forward of the phase-2 tax cuts to July 2021; an investment tax allowance; a possible “JobStart” program that would see the government subside new employment for SMEs; and additional infrastructure spending of up to $10bn.

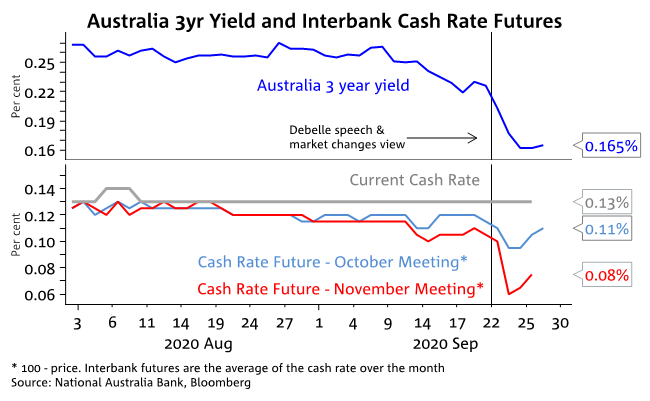

NAB’s rate call – rate cut and QE in October or November (November now more likely)

NAB changed its RBA rate call last Tuesday and is expecting the Bank to cut the cash rate to 0.10%, along with the 3-year yield target (YCC) and the TFF rate. We also expect the RBA to announce outright QE purchases in the 5-10 year area of the curve.

NAB expects these further easing measures to be announced at the either October or November Board meetings. Since then, journalists with known links to Martin Place suggest November is more likely at this stage as do markets.

Week ahead

Australia: It is a quiet week ahead of the October 6 Budget and RBA October Board Meeting. Datawise there is a smattering of data, including Credit and Building Approvals on Wednesday, Job Vacancies on Thursday, and a final read on Retail Sales on Friday. House Price data on Thursday though could create a few headlines with weekly data showing house prices have actually increased in Perth, Adelaide and Brisbane.

International: The China PMIs are on Wednesday with little change in positive momentum expected. The first US presidential debate is on Tuesday, while Congress continues to be unable to agree on the size of a 4th fiscal package amid signs of stalling in the labour market – Jobless Claims on Thursday and Payrolls on Friday will be watched closely. The Manufacturing ISM is also out on Thursday, along with Personal Income/Spending. EU/UK: possible restrictions to combat the resurgence in COVID-19 is the focus. The Times report the UK may announce a hard lockdown in Northern England and London. Outside of that, UK-EU trade talks continue.

Please open above report for further details.

Chart of the week

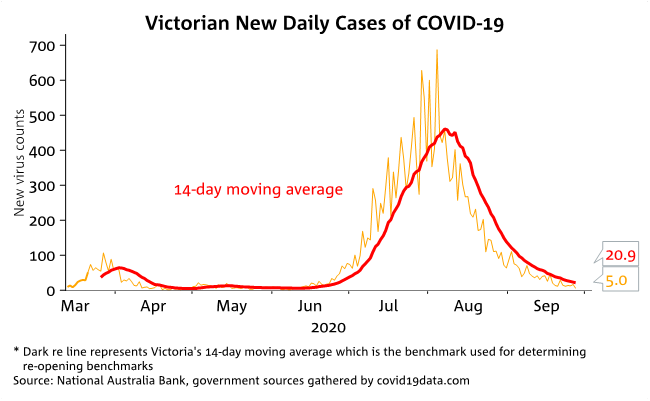

Markets expect an RBA rate cut in November, while Victorian new virus numbers fall to just 5

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.