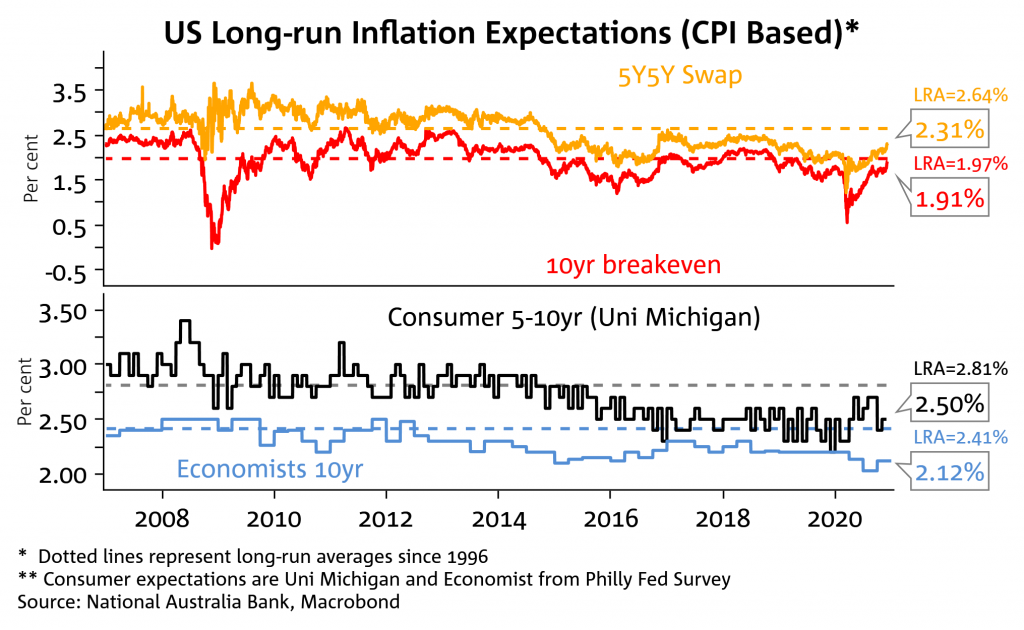

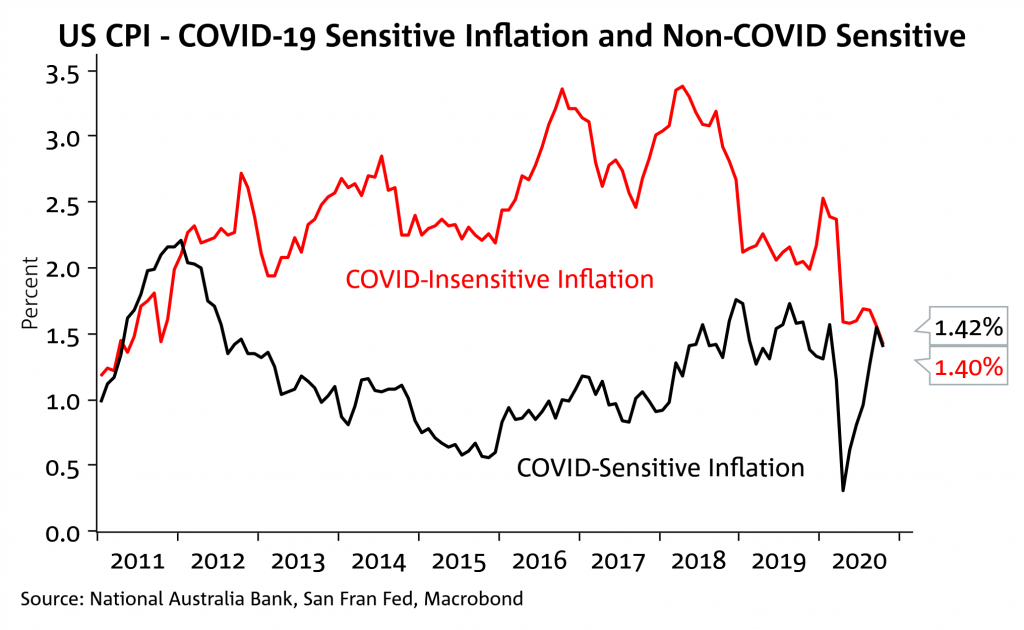

Price growth edges lower despite reasonable economy

Insight

The prospect of a COVID-19 vaccine being deployed from mid-December (US/UK) is helping drive market expectations of a sharp cyclical rebound in 2021.

The week ahead

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.