Price growth edges lower despite reasonable economy

Insight

The RBA is front and centre in local markets this morning.

https://soundcloud.com/user-291029717/is-the-rba-preparing-to-go-harder?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

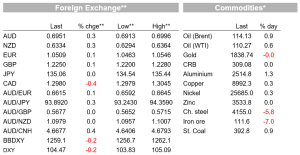

Predictably quiet/calmer start to the week after last week’s ructions, given the US Juneteenth holiday celebrating the abolition of slavery, with both US stock and bond markets closed. Risk sentiment is somewhat improved, with US futures up 1% and European stock markets similarly so, while bond yields are up +/- 10bps at 10 years in Europe. The USD is a touch softer, but AUD failed to recapture the 0.70 level overnight, 0.6996 the best it could muster and currently back down nearer 0.6950. The RBA is front and centre in local markets this morning.

US stock futures are about 1% stronger than where they finished in New York last Friday, The Eurostoxx 50 finished +0.9% and the UK FSE100 1.5% stronger, alongside which 10 year Bunds finished 9bp up at 1.75% and gilts +11bps at 2.60%. In FX last Friday’s sharpest toy, USD/JPY, is unchanged on Friday’s NY close while all other G10 currencies are firmer against the USD with NOK leading the way with oil prices up +/-$1 after last week’s savaging, followed by SEK (+0.5%) CAD (+0.4%) and AUD (+0.3%).

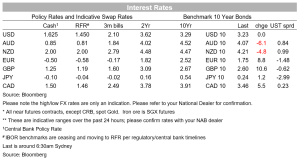

To central bank speak. BoE MPC Catherine Mann, who last week was one of the 3 MPC members who dissented from the consensus, favouring a 50bps rate rise, said part of the reason was that in light of the size of rate rises happening elsewhere, failing to keep up risked seeing the exchange rate weaker, in doing so adding to inflation. But as with every central bank, no-one is targeting their exchange rate of course, Mann was quick to add!

Across the English channel, ECB President Lagarde said inflation is too high and that the ECB must act but went no further than to reiterate that rates will rise by 25bps in July. Chief economist Philip Lane has popped up on the wires in the last hour saying that that the rate hike increment in September is still to be determined (in which respect the market has already decided it will be at least 50bps and indeed is currently priced for more than +75bps). On the anti-fragmentation instrument, Lagarde said that the tool must be ‘effective’ and proportionate’ and that fighting fragmentation is ‘right at the core of the ECB’s mandate’. In this regard, the ECB’s Villeroy de Galhau says that the mechanism for doing so should be available ‘as much as is necessary’. No hints whatsoever – and rightly so – on what the tolerance will be in terms of the likes of Italian yield spreads vis-à-vis core benchmarks.

Also to note from Lane are comments that the rate hike path could slow if the economy slows more than expected (presumably meaning it might not be a hike every meeting) and that when base rates go up, all kind of risk premia widen (read: financial conditions will tighten more than that implied just by the Deposit Rate alone). Lane is still to be marked out as one of the more dovish Governing Council members.

The lone Fed speaker has been James Bullard , who it has to be said has been prophetic in expressing his views all year and which have quickly become mainstream inside the Fed. He didn’t come down firmly on the side of 50 or 75bps for the size of the July meeting rate hike, so respecting the words of Jay Powell in the post-June meeting press conference but says that the Fed must meet market expectations (currently around +73bps, so a touch of revealed preference there). This is after Bullard’s protégé, Fed governor Waller, made clear at the weekend he was currently in favour of +75bps next month.

On the Fed, and likely to be capturing a lot of newswire headlines this morning, ex-US Treasury Secretary Larry Summers , a bete noire of the current administration and Fed and long at the forefront of the ‘secular stagflation’ movement, has been out on the last couple of hours claiming that the United States needs five year of unemployment above 5% to curb inflation and that the Fed need to make ‘much more difficult choices’.

No data of note overnight, but New Zealand has just reported its Q2 Westpac consumer confidence reading, which at 78.7 from 92.1 is a big fall and to record lows, consistent with the monthly ANZ measure which recently went to sub-GFC levels.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.