Price growth edges lower despite reasonable economy

Insight

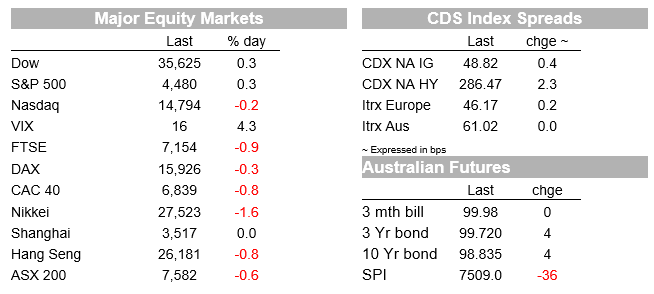

The much weaker than expected China data, lack of encouraging covid news over the weekend – no more so than in Australia – and the news out of Afghanistan which adds another dimension to ever-present geopolitical concerns (in this case, international terrorism) perennially cited as a risk to positive market sentiment – haven’t prevented the S&P 500 closing at a new record high.

https://soundcloud.com/user-291029717/chinas-slowdown-gives-confidence-another-blow?in=user-291029717/sets/the-morning-call

In truth the weakness evident in the Empire State Manufacturing survey overnight – down to 18.3 from a (record) 43.0 in July and the first of the August regional Purchasing Managers surveys – hasn’t been the main driving force behind the mostly risk-negative market price action since the start of the new week, but in the spirit of never letting the facts get in the way of a good story, it seems a shame to let such a great song go to waste this morning.

That said, the New Orders sub-series of the Empire (New York State) survey fell to a five month low, playing to the ‘peak US growth’ concerns, already amplified by last Friday’s plunge in US consumer confidence. We should also note that China’s manufacturing PMIs, where the Caixin vintage has fallen from a post-pandemic peak of 54.9 last November to a low of 50.3 in July – have historically been a reliable lead-indicator for PMIs in much of the developed world , the US especially. So while the July jump in the Empire survey was an outlier and the pull back in August therefore not wholly surprising, the numbers do serve to sharpen focus on what other regional, and then the nationwide, PMIs will reveal as we go through August and into early September.

The bigger influence on markets on Monday has been the extent of the slowing in China growth evident in the July activity readings . These showed headline year-on-year retail sales down to 8.5% from 12.1% and versus 10.9% expected, industrial production 6.4% from 8.3% and 7.9% expected and Fixed Asset Investment 10.3% YTD year-on-year down from 12.6% and 11.3% expected. In seasonally adjusted, month-on-month terms, industrial production growth slowed and retail sales fell in July. Similarly, real investment contracted steeply year-on-year, trends at least in part related to COVID-19 outbreaks in the second half of July, starting in Nanjing but rapidly spreading to other localities, including Beijing, prompting the Chinese authorities to introduce mass testing and travel restrictions, along with localised closures of events and businesses. Flooding in parts of China also impacted activity. Reflecting the impact of these measures, NAB has revised down its China growth forecast for 2021 to 8.7% (previously 9.5%), while our forecasts for 2022 (5.9%) and 2023 (5.7%) are marginally stronger.

The much weaker than expected China data, lack of encouraging covid news over the weekend – no more so than in Australia – and, we might add, the news out of Afghanistan and which adds another dimension to ever-present geopolitical concerns (in this case, international terrorism) perennially cited as a risk to positive market sentiment – haven’t prevented the S&P 500 closing at a new record high . It finished the day up 0.26% having been close to flat an hour before the close, though the best performing sectors, health care, utilities and consumer staples, are hardly a ringing endorsements of faith in ongoing bumper post-pandemic US economic growth. Energy (-1.8%) has dragged the chain, with oil prices off about a dollar. Earlier, European bourses had a bad day everywhere, the Eurostoxx 50 finishing -0.64% and the UK FTSE 100 -0.9%.

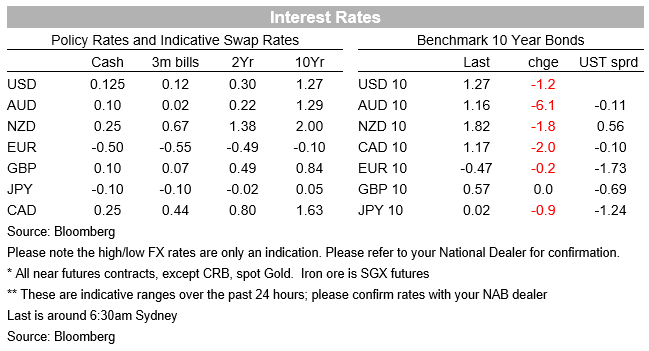

In bond markets, more hawkish Fed speak from known Fed hawks hasn’t prevented the 10 year Treasury yield ending the New York day one basis point lower at 1.27%, though the 2-year yield is up marginally (0.2bps) and 10s are well back from their intra-day low of 1.22%. Catching attention has been a WSJ report titled ‘Fed Officials Weigh Ending Asset Purchases by Mid-2022’ and saying Federal Reserve officials are nearing agreement to begin scaling back their easy money policies in about three months if the economic recovery continues, with some pushing to end their asset-purchase program by the middle of next year.

Inspection reveals this is not a new ‘source story’, largely referencing recent commentary from various Fed officials. Overnight, we have heard from who we consider to be the two biggest hawks on the FOMC, Bob Kaplan and James Bullard, neither of whom are current FOMC voting members – albeit Bullard is in 2022 – as well as Eric Rosengren, also on the hawkish side of late. Kaplan says he wants to taper at the rate of $15bn per month, Bullard at $30bn and Rosengren wants tapering to be done by the middle of 2022. On the more neutral/dovish side, San Francisco Fed president Mary Daly says she’s open to tapering starting later this year or not until next.

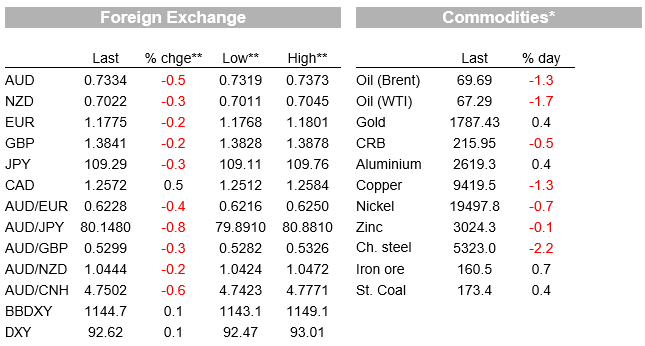

In FX, it’s a familiar story of USD support on safe haven considerations (indices up 0.1%) but outpaced by the CHF and JPY (both +0.3%) while commodity linked currencies are back languishing once more, AUD, NOK and CAD all off by 0.5% and the NZD a lesser 0.3% in front of tomorrow’s RBNZ decision.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.