Price growth edges lower despite reasonable economy

Insight

US June non-farm payroll employment 372k vs. 265k expected.

https://soundcloud.com/user-291029717/healthy-jobs-data-bad-news-for-the-economy?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Friday/weekend data highlights

US June non-farm payroll employment 372k vs. 265k expected (April/May revision -74k)

US June unemployment rate 3.6% from 3.6% as expected

US June average hourly earnings 0.3% m/m as expected

US June average hourly earnings 5.1% y/y from revised 5.3% (5.2%) and 5.0% expected

US June participation rate 62.2% from 62.3% and 62.4% expected

Canada June employment -43.2k vs. 22.5k expected

Canada June unemployment rate 4.9% from 5.1% and 5.15 expected

Canada labour participation rate 64.9% from 65.3% and 65.3% expected

China June CPI 2.5% from 2.1% and 2.4% expected

China June PPI 6.1% from 6.4% and 6.0% expected

If a softer US labour market is part of the solution to the United States’ inflation problem, there was precious little hard evidence of it in Friday’s June payrolls report. A 74k net downward revision to payrolls over April and May combined took a little gloss off the higher than expected 372k June headline print, but the unemployment rate printed at 3.6% (its post-pandemic low) for the fourth consecutive month, while average earnings growth is still running above 5% y/y, albeit the monthly run rate was only 0.3% after May was revised up to 0.4% from 0.3%, suggesting annual growth can fall back to nearer 4% in coming months.

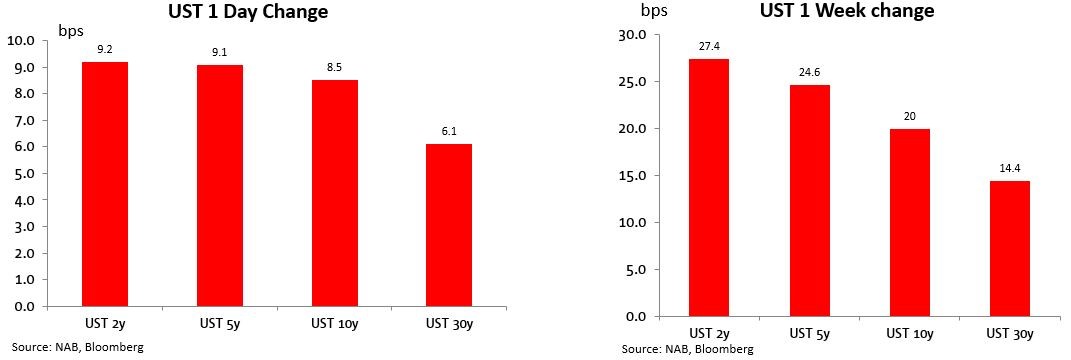

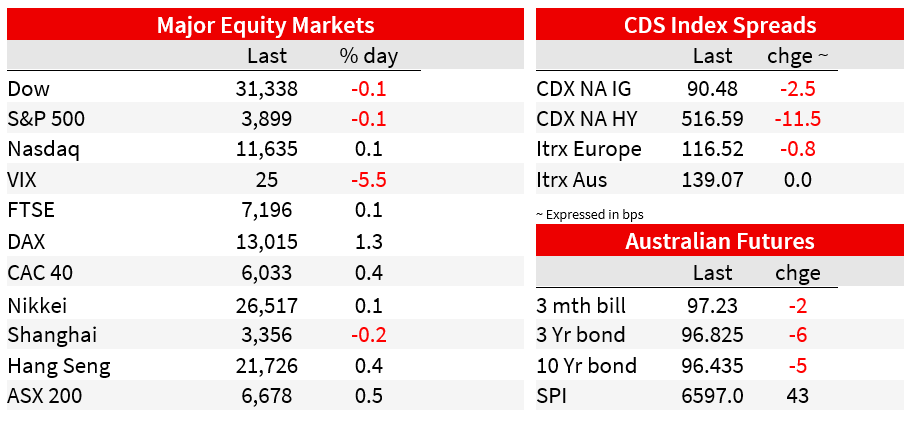

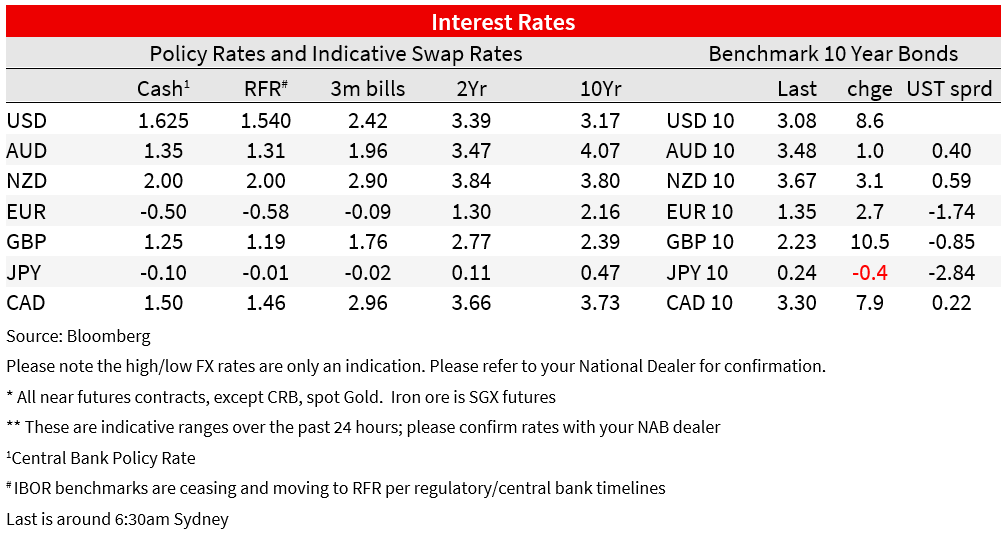

The absence of any downside surprises in the report saw an immediate sell off in bonds , both 2 and 10 year treasury yields up by 10bps or more, gains which held through the remainder of the New York session (2s finishing at 3.105%, 10s at 3.08%). Money markets lifted pricing for the July 27 FOMC rates decision to 74bps from 71bps the day before (and in Canada after its labour market report, from 72.5bps to 75.3bps, following the drop in its unemployment rate to 4.9% from 5.1%, albeit driven by a drop in the participation rate to 64.9% from 65.3%).

Atlanta Fed President Bostic , not a voter this year, spoke after the employment report and said he backed a second 75bps hike later this month because of the “tremendous momentum in the economy”.

NY Fed President John Williams in a speech on Friday didn’t directly reference the payrolls report or specify his preference for the size of the next rate rise but said that U.S. economic growth could fall below 1% this year and remain sluggish through 2023 as the Fed acts “resolutely” to curb inflation. He reiterated the increasingly strong language FOMC officials have been using to characterize their resolve to lower inflation to the Fed’s 2% target. “Inflation is sky-high, and it is the number one danger to the overall health and stability of a well-functioning economy,” Williams said. “I want to be clear: this is not an easy task. We must be resolute, and we cannot fall short.”

In other US news Friday, President Joe Biden said he hasn’t decided whether to roll back any of the tariffs on Chinese imports. “I haven’t made that decision yet,” Biden told reporters at the White House in response to a question about the tariffs. “They’re going through them one at a time,” he added in an apparent reference to administration officials.

Other CB speak of note since we left off on Friday included ECB Governing Council member and uber-hawk Robert Holtzmann, who said the ECB should increase rates by as much as 125 basis points by September if the inflation outlook doesn’t improve. An initial July hike should be 50 basis points and an even larger move should be considered at the Sept. 8 meeting to pro-actively steer the economy toward calmer waters, Holzmann told the Kronen Zeitung newspaper in an interview published Saturday. “When the situation doesn’t improve, a 0.75 percentage point increase may eventually become necessary,” he was cited as saying. “The time has now come for clear rate steps, otherwise inflation will solidify.”

Also deemed a hawk, fellow ECB GC member Klass Knot speaking on a Dutch talk show said, “It may well be that while the economy is slowing in the coming months and quarters, we will increase interest rates… It’s very likely….in an ideal world, you’d want to stimulate the economy but bring inflation down at the same time…unfortunately that’s not what we can do, we have to make a choice; in that case our mandate is very clear — we have to choose bringing inflation down.”

ECB President Christine Lagarde meanwhile said she doesn’t want to stop colleagues from speaking out on monetary policy as she acknowledged that communication is a challenge at present. “There is no intention to suppress certain views or question the independence of the individual members of the Governing Council,” she said in a letter to a European Parliament lawmaker. “The public expression of the different views held by policy makers in due course enhances the robustness of our decision-making process.”

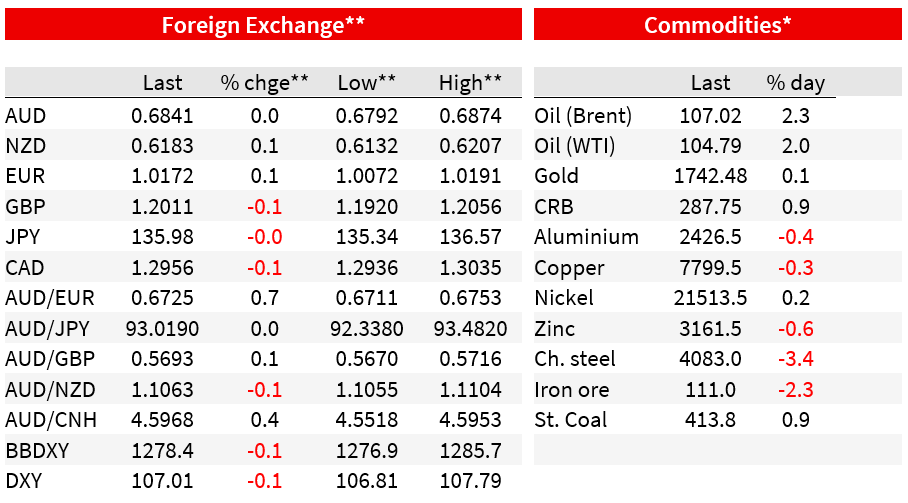

Also, over the weekend China June CPI came in 2.5% y/y from 2.1% and versus 2.4% expected, led by higher pork prices. Ex-food and energy measure 1.0% up from 0.9%. The Annual rise in PPI slipped to 6.1% from 6.4% and versus 6.0% expected. The monthly reading was flat.

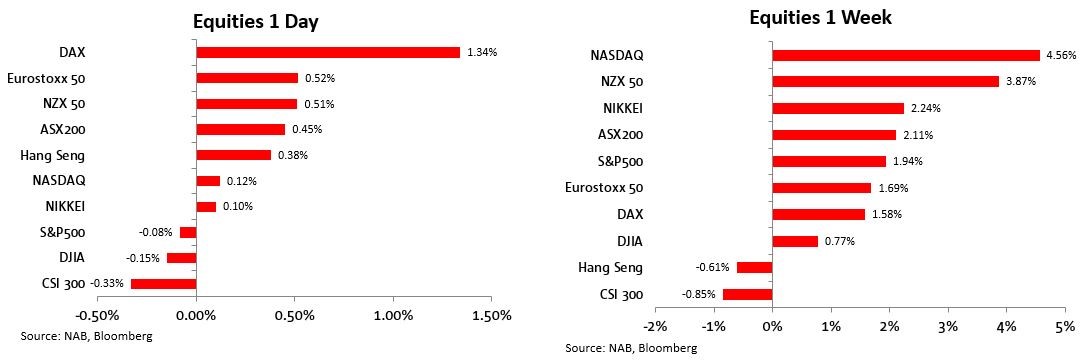

US equity markets initially sold off in conjunction with the spike higher in US bond yields on the payrolls release but recovered during the session to end the day little changed (S&P500 down less than 0.1%, NASDAQ up by just over 0.1%). With the exception of Shanghai and Hong Kong, it was a positive week for most stock markets, led by the NASDAQ. Let’s see if gains can survive the quarterly US earnings season kicking off on Thursday.

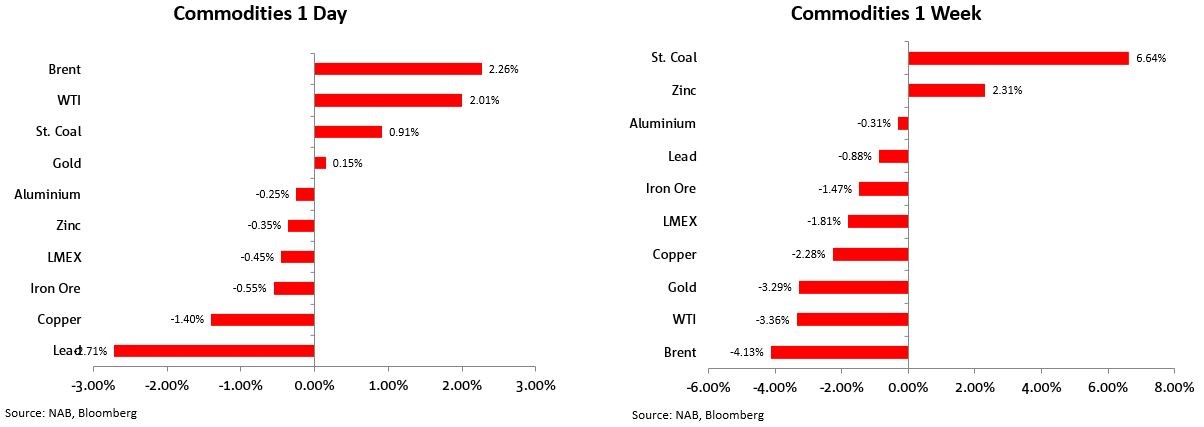

Nine of the eleven S&P500 sub-sectors finished down on Friday (Health Care +0.3% and IT +0.1% the exceptions) led by a 1.0% fall for materials in what was a down day (and week) for most commodities consistent with concerns about demand destruction implicit in a global economic slowdown (chart below). The exceptions on Friday were crude oil (up over 2%) and thermal coal (+0.9%). On the week, exceptional coal demand – the principal driver of May’s record Australian trade surplus – continue to shine through with another 6.6% price rise.

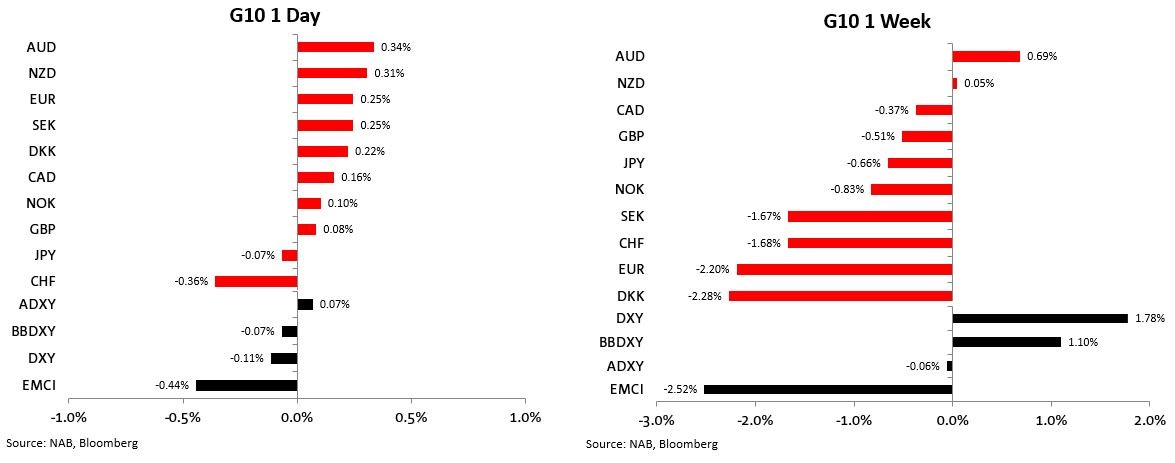

In FX, there were only limited net moves on Friday, but this was only after the mighty USD had hit new cycle highs in index terms, led by a further fall in EUR/USD to briefly below 1.01 (pre-US payrolls). The USD eased back alongside a recovery in US stocks, even though US bond yields held on to all of their knee jerk post-payroll gains.

On the week, it was another very good for the USD up a 1.8% in DXY terms (EUR/USD down over 2% on the week) with the broader Bloomberg BBDXY up by 1.1%. The surprise then is to note that the one major currency to outperform a rising USD was AUD, AUD/USD recovering from its mid-week fall to new post-pandemic low just above 0.6760 to 0.6858 for a 0.7% weekly rise. Indicative, perhaps, of better two-way price action emerging at what are, fundamentally, significantly undervalued levels.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.