Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Another day, another direction for US equities. Today they’re back up (for now) on easing tensions over Syria (for now). Join @NAB’s Gavin Friend and Phil Dobbie on #TheMorningCall.

https://soundcloud.com/user-291029717/equities-bounce-back-again-as-war-talk-eases

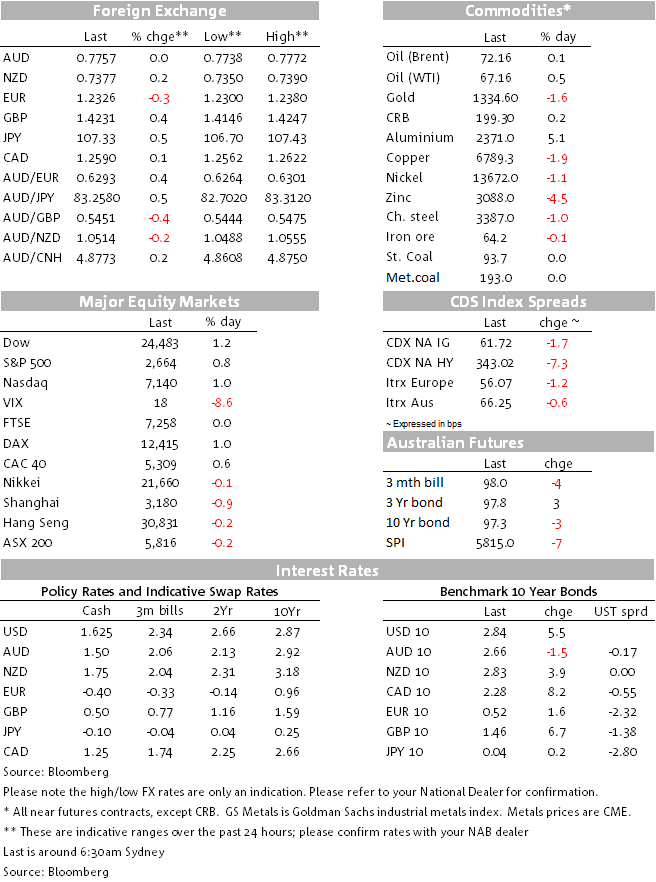

Ease in trade and geopolitical tensions have helped risk sentiment overnight.US and EU equities have closed in positive territory, UST yields are also higher and the USD is stronger, mainly driven by softness in European currencies and yen weakness with the latter declining amid a decrease in safe haven demand. NZD is a mild outperformer while AUD is a bystander.

Market sentiment remains at the mercy of political rhetoric and just like Bjork’s Possibly Maybe 1995 hit, the theme from the overnight session is that there are encouraging signs of an ease in tensions in Syria along with improved prospects for resolutions in trade tensions. Not only in terms of US-China trade negotiations, but also in terms of a positive outcome for NAFTA and…surprise, surprise, even TPP gets a mention!

President Donald Trump said that he will be meeting national security advisers later today to discuss the US response to the alleged chemical weapons attack on civilians by the regime in Syria. But in the tweets that followed, the President appeared to play down an imminent military response, noting that “Never said when an attack on Syria would take place. Could be very soon or not soon at all!”. US defence secretary Mattis said that there were non-military options available to the international community, while Russian leaders urged calm and reined in their own war rhetoric. That said the thread of a military response still remains a possibility. French President Emmanuel Macron said that there’s proof that Assad’s regime again used chemical weapons and that allies are working to decide what response would be “useful and efficient,”. Meanwhile, just to complicate matters a little bit more, Russia claims to have discovered chemical weapons stockpile in rebel territory.

The ease in geopolitical tensions helped sentiment, but President Trump also helped the cause following a meeting with lawmakers. On China the President said that the two countries ultimately may end up levying no new tariffs on each other. On NAFTA, he indicated that talks are progressing toward a successful renegotiation and on TPP, the President reportedly told lawmakers that he is considering re-joining the trade deal he pulled out shortly after taking office.

So with the world in a better place, US and EU equities have closed in positive territory and the VIX index has drifted below the 20 mark closing the day at 18.49. Worth noting too that there is a prospect for a re-focus back into to fundamentals as the earnings reporting season kicks-off in the US. Blackrock reported decent results overnight and we have a few banks reporting their results tonight (see more below).

In index terms, the USD has edged a little bit higher overnight mainly driven by softness in European currencies and yen weakness. SEK is at the bottom of the G10 board, down almost 1% after underlying CPI inflation in Sweden came in below market expectations, with the ex-energy measure coming in 0.3% below the Riksbank’s forecast. The softer inflation number has essentially erase any prospect of an eminent a removal of easy policy by the Riksbank. ECB minutes (or accounts) from the 8 March policy meeting were also out overnights and the overriding message is cautiousness. Policy makers noted concern over risks of a trade war with the US and its impact on confidence, while FX remained a source of uncertainty.The ECB repeated that the path on inflation was close to a sustained adjustment but not yet sufficient. Tighter financial conditions also got a mention, while the minutes said the removal of the easing bias should not be misunderstood. The ECB remains reactive rather than proactive. EUR ended the day 0.32% lower, the pair traded to an overnight low of 1.23 and now trades at 1.2337.

The improvement in risk sentiment has also helped the USD outperformance against JPY with USD/JPY now trading a ¥107.33. Yesterday the pair traded to an intraday low of 106.70, but true to form, the decrease in safe haven demand has played into yen weakness overnight.

Meanwhile the Kiwi and GBP are the two pairs that managed to marginally outperform the USD. NZD outperformance has been broadly based with the AUD/NZD cross briefly dipping below the 105 mark. For now NZD appears to be benefiting the most from the improvement in risk sentiment. Jason Wong, our BNZ strategist notes that it seems that the government’s new policy to restrict NZ’s oil exploration industry and threaten thousands of high-paying jobs hasn’t had a negative impact on sentiment.

AUD for now remains a bystander. The pair traded in a narrow range overnight and sit essentially unchanged at 0.7758. AUD has been one of the G10 underperformers since the drop in US equities late in January/early February, the rise in equity volatility has been one factor weighing on the AUD while the rise in US-China trade tensions has also weighed on the currency. It seems that further concrete improvement in trade tension are needed for the AUD to begin a proper recovery, that said the recent rejections for moves sub 0.7650 suggest the AUD is on a stronger footing now. A good start to the US earnings reporting season and further positive sound bites on US-China trade negotiations are probably needed for an AUD rebound.

As for UTS yields, the 10y note is at 2.83% – the highest level in a week and the curve is a touch steeper. A quick look at commodities reveals a mixed picture. Copper is down almost 2%, gold is -1.3% and oil is essentially unchanged.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Labour market strong, housing supply falling behind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.