Price growth edges lower despite reasonable economy

Insight

It was all about US CPI overnight with markets reacting sharply to a lower than expected print with Equity and FX markets taking the CPI miss as a positive signal, taking some pressure off the Fed and a sign that inflation has peaked.

https://soundcloud.com/user-291029717/false-hope-on-easing-inflation?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

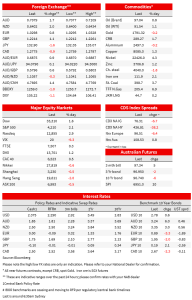

It was all about US CPI overnight with markets reacting sharply to a lower than expected print. Headline inflation was 0.0% m/m vs. 0.2% expected and core inflation was 0.3% m/m vs. 0.5% expected. Alternative core measures though were stronger with the Cleveland Fed’s trimmed mean at 0.4% m/m and median at 0.5% m/m, suggesting little change to the inflation impulse despite the headline miss. The Fed’s Kashkari and Evans noted the print didn’t change their path for rates. Equities surged with the S&P500 +2.1% and NASDAQ +2.9%. Yields initially fell sharply, but moves were quickly pared. The 2yr yield initially fell -21.9bps and then quickly pared moves to be -7.2bps to 3.22%. The 10yr was similar, initially down -14.8bps, but then paring to be -3.0bps to 2.78%, and exactly where it was this time yesterday. Fed Funds pricing moved a little (but not a lot) with a 75bp hike in September now sene at a 46% chance from 73% yesterday. The estimated peak in the fed funds is now 3.60% in March 2023, from 3.67% yesterday. Pricing for cuts in 2023 are little moved with 49bps worth of cuts priced from 54bps yesterday. The USD (DXY) in contrast moved sharply, down initially -1.3% to be -1.1% over the past 24 hours.

First to the CPI print. Both Headline (0.0% m/m and 8.5% y/y) and Core (0.3% m/m and 5.9% y/y) printed two tenths below the consensus. Much of the headline decline was driven by energy which fell -4.6% m/m in July after having surged 7.5% in June – falling gasoline prices the major driver at -7% m/m from +11.2% in June. As for the core measure, two large components weighed with lodging away from home ‑2.7% m/m and airline fares -7.8% m/m. Rent inflation remained high with primary rents at +0.7% m/m and owner-occupier rents 0.6% m/m. Alternative core measure which have provided a good guide to inflation when there has been large declines in certain categories was stronger with the Cleveland Fed’s trimmed mean at 0.4% m/m and median at 0.5% m/m. This suggests there has been little change to the overall pace of core inflation despite the headline miss and it is way too early to be confident inflation has turned or is on a path back to the Fed’s 2% inflation target.

Equity and FX markets nevertheless have taken the CPI miss as a positive signal as taking some pressure off the Fed and as a sign that inflation has peaked. The reaction in equity markets though also acts to loosen financial conditions, where the Fed has been attempting to tighten them. The S&P500 rose 2.1% on the data and is now 14.8% above the tough seen in June, though is still -12.2% away from the January 2022 peak. The NASDAQ rose a stronger 2.9% and is now 20.8% above its June low. Historically a 20% rise has been historically interpreted as a bull-market, though in reality it is still likely stocks are in a bear market given the NASDAQ is still -19.9% below its November 2021 high. In this light it is worth noting Fed speak remains hawkish with Kashkari, Evans out overnight (see below), as was the WSJ’s Fed whisperer Nick Timiraos (see WSJ: Fed Likely to Want Further Evidence of Inflation Slowdown). Timiraos noted in his piece “Wednesday’s inflation report keeps the Fed’s door open to a half-point rate increase in September if subsequent data confirm price pressures are easing. But a 0.75-point rise remains possible after recent reports of accelerating growth in jobs and wages point to significant income gains that could sustain stronger spending and higher prices”.

Fed speak was hawkish, and downplayed over-interpreting the CPI data. The Fed’s Kashkari who until recently was one of the most dovish on the CPI said the print “doesn’t change my path” laid out in June which called for a fed funds rate of 3.9% at the end of 2022 and 4.4% at the end of 2023. Importantly Kashkari also stated that path remains true even with a recession being possible in the near term. Kashkari also pushed back on the market pricing of cuts in 2023, noting “I think a much more likely scenario is we will raise rates to some point and then we will sit there until we get convinced that inflation is well on its way back down to 2% before I would think about easing back on interest rates ”. The Fed’s Evans was similar in that while stating the inflation numbers as “the first positive report”, inflation remains “unacceptably high” and still wants to get the fed funds rate to 3.5% by the end of 2023 and 4% by the end of 2023.

FX markets have seen an outsized reaction, with little reversal of initial moves. The USD (DXY) is broadly weaker, down -1.1% for the day. The NZD has been one of the key beneficiaries of higher risk appetite, seeing a gain of more than 2% as has been the AUD which is up 1.7%. EUR was +0.8% and GBP was 1.1%, while USD/JPY was -1.6%. One good CPI report doesn’t change our view of the global backdrop which still remains dire on the back of higher rates and energy prices. Speaking of energy, Russia’s pipeline operator Transneft PJSC said it resumed oil flows via the Druzhba line toward Ukraine, helping alleviate fears in Eastern EU countries. Oil prices though were volatile with EIA data showing a build in crude inventories.

Finally in China, yesterday’s CPI and PPI numbers were below expectations though were not overly market moving. In COVID news, China and the UK are said to be restarting direct passenger flights, though at this stage the flights are one-way from China to the UK (no tickets are being sold for the return flight back to China), so the implications for China’s zero-COVID policy is unclear. Scientists are also monitoring a new virus in China (the Langya henipavirus) which has been detected in 35 people. No deaths have been repeated, but symptoms include nausea, headache and vomiting.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.