Labour market strong, housing supply falling behind

Insight

Inflation. Watch out, it’s coming.

Tapas Strickland explains to Phil Dobbie, the rising oil and metal prices have had an impact on government bond yields in the US and Europe.

https://soundcloud.com/user-291029717/inflation-watch-out-its-coming

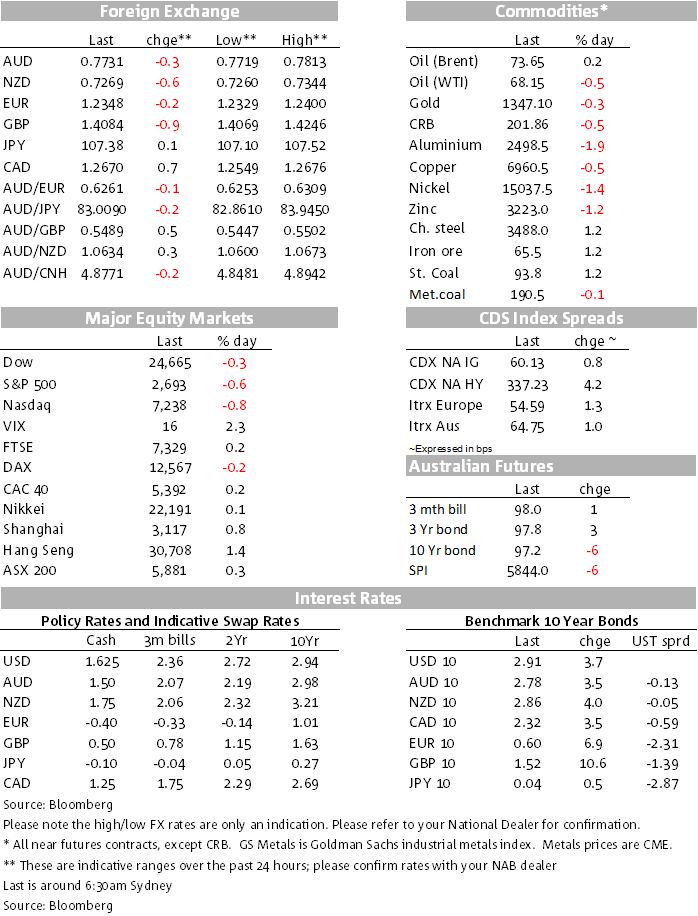

There’s been a further step up in Treasury yields overnight following on the heels of the previous session’s jump in oil and base metals prices, those prices having taken a breath and steadied overnight. 10 year Treasury yields have risen just under 4bps to be back over 2.90%, the highest close since late February. European bond yields also shifted higher, including in the UK, shrugging off a weaker than expected Retail Sales report for March. German 10 year bunds rose 5.9 bps to 0.60%, while UK 10 years increased 10.6bps to 1.52%. In the currency space, the USD has regathered its composure with the DXY up 0.3% and the Bloomberg spot dollar index up 0.5%.

Fed Governor Brainard, usually regarded as one of the ‘doves’ on the rate-setting committee, said overnight that the fiscal stimulus would “reinforce cyclical pressures”, adding to Fed rate hike expectations. The market now prices 54bps of rate hikes by the end of the year, slightly more than the 2 hike median set out in the latest set of Fed projections, and adding another 3bps of pricing to the 19 December expectations.

There was little in the way of economic data news overnight. UK retail sales in March missed the mark, put that was down to the bad weather and shrugged off by sterling. The five German institutes upgraded Germany’s growth forecasts by 0.2% for this year and next to 2.2% for 2018 and 2.0% for 2019.

Base metal prices have only partially retraced, WTI oil is only marginally off yesterday’s gains, while Brent has risen another 20 cents. In the metals space, there are stories that Russia is endeavouring to channel its supply into China as an alternative. Among equities, it’s been Apple and semiconductor stocks in Europe leading the way lower on reduced expectations for iPhone sales after Taiwan Semiconductor’s downbeat forecasts that cited a “very high end smartphone”.

The Nasdaq has under-performed, but all three major indices having closed lower by between 0.34% (Dow) and 0.78% (Nasdaq). Banking sector stocks outperformed for a change, helped by the rise in interest rates and a steeper yield curve. Earnings results were generally better than expected, including from Proctor and Gamble, Bank of New York Mellon and Blackstone. 79% of US corporates have beaten analyst earnings expectations and 83% sales expectations so far this earnings season.

The AUD/USD continued to make some net commodity price-led gains during yesterday’s APAC session, testing 0.78, but has retreated lower overnight, along with most majors that have lost some grip against the USD. Those AUD gains did not get the further shot in the arm from yesterday’s March employment report that we were anticipating, the report under-clubbing expectations and our own reading of a still strong jobs market.

Oil continues to be some centre of attention, WTI giving back only a little of yesterday’s rises and Brent marching on a little higher. As OPEC gathers to meet, unnamed sources from within OPEC have referenced that OPEC is within sight of reaching their producers’ target of reducing stocks to five year averages. That is consistent with the pattern in the US where inventories have changed little so far this year despite continued rises in US oil production with US inventories also back to their five year average. OPEC-inspired supply constraints seem to be part of the story, but stronger global demand is also part of the story. Brent for example is up 4.8% so far this month and year to date up a sizeable 23.9% on last year’s $67.81/bbl average.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.