An early-day bounce in US stocks following NY Fed’s John Williams CNBC interview (see below) proves to be of the (very) dead cat variety.

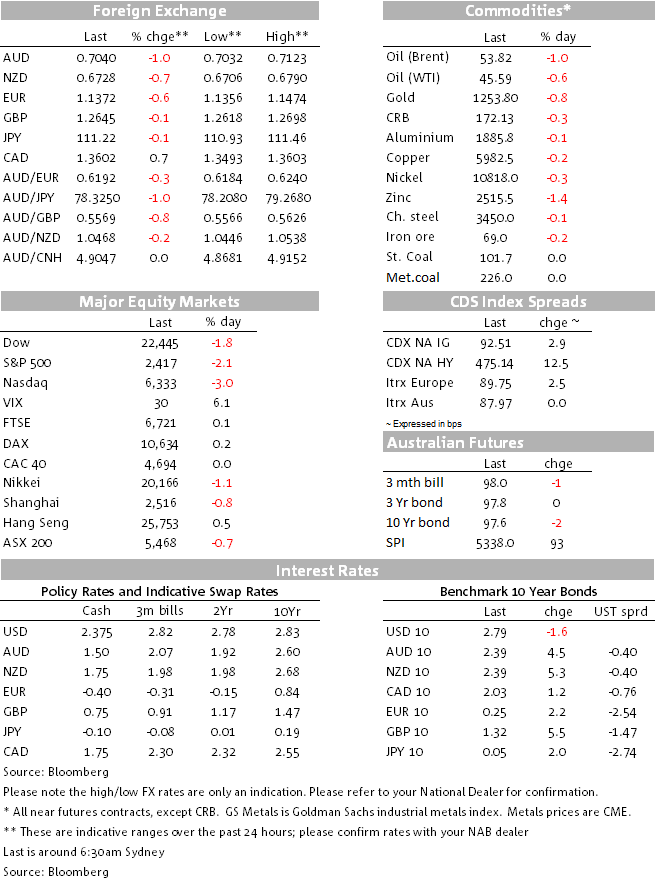

S&P ends -2.06% (-7% on the week, -9.6% YTD). DJIA -1.81% (-9.2% YTD). NASDAQ -2.99% and -8.3% YTD but -21.7% versus 30th August 2018 highs and so in bear market terrain (>20% down from prior high).

The VIX adds 1.73 to 30.1, to its highest (and first time above 30) since 9th February.

A partial government shutdown commence on Friday after the Senate failed to give Trump his $5bn worth of wall funding. 420,000 government employees to work without pay, 380,000 furloughed (forced to take unpaid leave). Thursday is the absolute earliest that the shutdown could be resolved, but realistically it looks unlikely before the New Year.

Thursday’s resignation of the highly respected Defence Secretary Jim Mattis on fundamental differences with Trump, and who will now leave two months earlier than planned on Dec 31st, at Trump’s behest, follows the earlier resignation of John Kelly as Trump’s chief of staff. It provides more than enough fodder for perceptions of chaos and instability in the White House. At the same time, the government shutdown offers a true foretaste of what lies ahead once the new Congress in sworn in on January 3 The US debt ceiling is set to be re-imposed on March 1st 2019 and will almost certainly provide another flashpoint regarding Trump’s wall-funding (and other demands) assuming it has not been put to bed earlier.

To this we now add Friday’s Bloomberg reports that Trump had been sounding out Fed officials on whether he could fire Fed chair Jay Powell (to which Treasury secretary Steve Mnuchin has taken to twitter to say Trump is not considering firing him even if he could and where the advice is reportedly that he cannot). .

John Williams – doubtless one of the three FOMC members we should listen to besides chair Powell and vice-chair Rich Clarida, arranged himself onto CNBC Friday morning to say the Fed was going into 2019 with ‘its ‘eyes wide open’.

Williams was at pains to point out how good the economic data looked to the Fed this week, but also stressed the significance of the tweaks to the language in the Fed statement. In particular, he wanted his audience to know that saying the Fed ‘judges’ (that some further gradual increases in rates, etc…..) is not the same as saying the Fed ‘expects’. He also stressed the insertion of ‘some’ in front of ‘further’ and the addition to the statement of the sentence about monitoring global economic and financial developments.

As an exercise in damage limitation, Williams’ interview was an abject failure, the S&P falling by more than 3.5% after initially rallying by some 1.5% immediately following the interview.

Economic data that played to the market’s slowdown fears came in the form of durable goods orders, +0.8% against 1.6% expected and -4.3% previously. Ex-transport orders fell by 0.3% (+0.3%E) and capital goods order ex defence ex-aircraft – the better underlying measure – by a bigger 0.6% (+0.2%E).

Q3 US GDP was revised to 3.4% from 3.5% (3.5%E)

The November core PCE deflator printed 0.1% (0.148% unrounded) against 0.2% expected but yr/yr rose to 1.9% from 1.8% as expected.

Personal Income 0.2 (0.3%E) and Personal Consumption 0.4% (0.3%E)

On the bright side…..

The final University of Michigan consumer sentiment index came in at 98.3 versus a preliminary 97.5 (and 97.5 expected). No sign here of stock markets negatively impacting sentiment. It might come January though.

And more importantly for Australia, China’s Central Economic Working Conference (CEWR) ended Friday with a commitment to “stabilising aggregate demand” through “countercyclical policy adjustments”, pledging “pro-active fiscal policy” and “prudent monetary policy” (not “prudent neutral” policy as previously)

In FX the DXY USD index added 0.7% to 96.96; EUR/USD was the biggest contributor to the gain (-0.65% to 1.1372) but AUD was the biggest G10 loser -0.95% to 0.7040 (and closing in NY pretty much on the lows). AUD/JPY finished 1% down at Y78.33. NZD lost 0.0.71% to 0.6728.

Coming up

Given developments in Washington since Friday’s New York close, whether or not this aggravates the sell-off in US stocks tonight and over the Xmas-New year period is the major point of interest before Christmas Day.

The main data points worth noting between now and year-end are the China official PMIs on New Year’s Eve. Locally, RBA private credit data is the same day. There is a smattering of housing related releases in the United States through the week.

Expect to hear plenty of chatter about month and quarter end rebalancing demand for USD (and supply of AUD) though recall this failed to show up at the end of October when stocks were sharply lower on the month. Regardless, AUD looks to be at some risk of testing the 0.70 level one side or other of year-end.

Market prices

Markets Today will return to Business Research and Insights on Monday 7 January 2019.

We wish all our readers and listeners to the Podcast all the best for the festive season and the New Year.