Price growth edges lower despite reasonable economy

Insight

Technology out of favour, markets a little confused.

In today’s podcast Phil Dobbie talks to NABs Tapas Strickland about how the Trump administration is strengthening its aim at China’s high-tech industries and the impact it’s having on the NASDAQ.

https://soundcloud.com/user-291029717/technology-out-of-favour-markets-a-little-confused

I’ve just seen that Judith Simpson has died aged 93. Described as a rare female pioneer of pop journalism in the UK, she was the inspiration for ‘Hey Jude’ written by Paul McCartney in 1968.

I’m struggling to make use of this as a market-appropriate song title in homage to Mrs Simpson, unlike Turning Japanese by the Vapors which anyone not familiar with the early 1980s UK punk scene – I have to admit I am – is probably much less familiar with than anything by the Beatles.

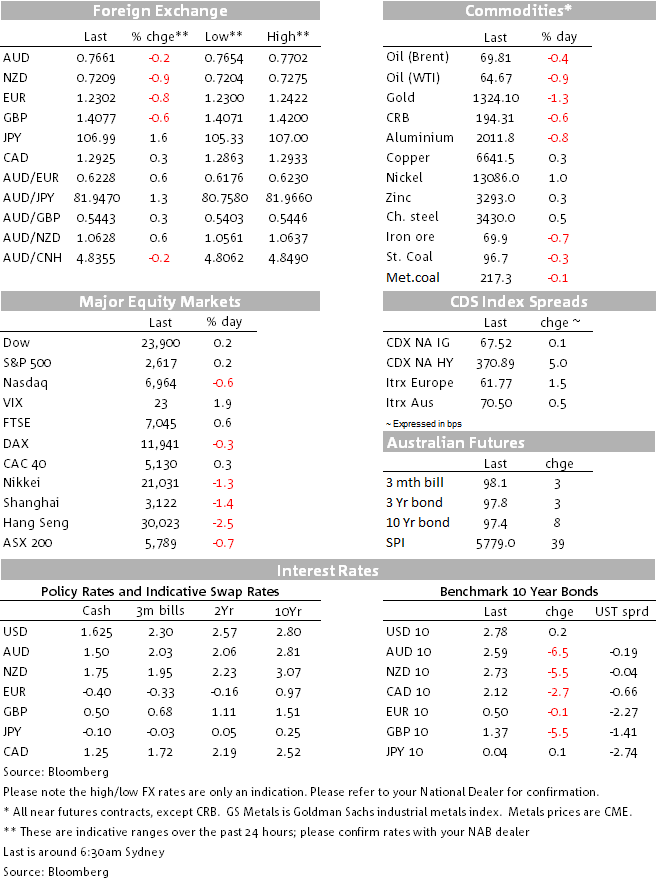

Scandinavian currencies aside (NOK hurt by weak retail sales, SEK by a dovish Riksbank comments) The Japanese yen is the weakest of the G10 currencies in the past 24 hours. This is despite what still looks and feels like a more ‘risk-off’ than ‘risk’-on market backdrop when looking across other asset classes.

US stocks have failed to recover any of Tuesday’s FANG-led weakness, in part due to a ~5% hit to Amazon after President Trump’s latest verbal attack on the on-line retail behemoth demanding more regulation (and which will probably be followed in short order by European demands to tax them more, such is the contrast between the current US and EU attitude towards the US tech-sector giants).

In bond markets, 10 year Treasury yields, having broken below the 2.80% level in late New York trade on Tuesday (the bottom of a six week range), have traded sub-2.75% overnight (2.77% now) with the 2-10s curve extending the recent flattening theme to now be at its flattest since about October.

Still weighing on risk markets are US-China trade concerns, with White House trade adviser Peter Navarro reminding us on Bloomberg television that the focus of latest planned tariff actions – utilising Section 301 of the 1974 US Trade Act – are the so called China 2025 industries.

“China in my view brazenly has released this China 2025 plan that basically told the rest of the world, ‘We’re going to dominate every single emerging industry of the future, and therefore your economies aren’t going to have any future.’ It’s artificial intelligence, robotics, quantum computing — all those things,” Navarro says. The Section 301, which is on intellectual property theft and forced transfer, is specifically designed to address those kinds of things. And I think the world should welcome that. Europe is getting hammered by the same thing. Japan is getting hammered.”

As for JPY weakness in FX markets, the safe haven status we would normally associate it with given the broader market theme, has for now been usurped by two things. One is M&A news, where the WSJ reports that Takeda Pharmaceuticals Co. is weighing a bid for UK rival Shire, the latter closing Wednesday with market value of £32bn following the news. The other is more encouraging sound bites related to North Korea, where Kim Jong Un has reportedly offered talks with Japan, while China has said that following the talks between President Xi and Kim Jong Un earlier this week, de-nuclearisation is on the table for talks with US and others. President Trump’s latest tweets seem to imply this is almost a done deal. What could possibly go wrong?

Our hesitancy in fitting facts to figures this morning (what some folks unkindly refer to as making up stories) is because month and quarter-end (and Japanese year-end) flows do appear to be figuring in current FX (and possibly bond market) moves and will continue to do so in what is the last working day of the month for most financial centres. The train of logic here is that with US stocks +/-4% down on the month, non-US fund managers will need to be buying US dollar to bring their hedge ratios back in to line with current benchmarks. It seemed to work this way in February when the S&P finished the month down a similar amount and the DXY dollar index added over 0.8% in the last two trading days of the period.

If month-end is relevant, it can provide some additional weight on AUD today. Although it one of the better (or least worst) performers on the night, it has made a near year to-date low of 0.7654 (0.7762 now). Note too that commodity prices are in a sea of red, including iron ore back below $70 for the first time this year – a month ago it was looking like it was about to knock on the door of $80.

Data wise, US 4th quarter GDP was revised up slightly (2.9% from 2.7%) and US home sales data was a bit better than expected (+3.1%) . The former at least looks to have provided a bit of post-release support for the USD.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.