Price growth edges lower despite reasonable economy

Insight

Italy looks set to go back to the polls. NAB’s Rodrigo Catril looks at the market reaction on today’s Morning Call podcast.

https://soundcloud.com/user-291029717/italian-elections-looking-more-likely-oil-falls-further

Fears of a euro existential crisis are gathering momentum amid simmering political turmoil in Italy. President Mattarella proposition to form a technocratic government has been met with fierce opposition, suggesting new elections late in the Italian summer now look likely. Stevie Nicks’ song about love during a summer holiday in Italy, couldn’t be further from investor’s love for Italy at the moment. Italian equities and bonds have been sold sharply overnight, dragging the Euro to its lowest level since November last year. Core bond yields also traded lower, but given public holiday in the UK and US, it is hard to tell whether contagion risk has been contained.

After vetoing the appointment of a Eurosceptic economy minister, which triggered the collapse of the coalition government on Sunday, Italy’s president sought to calm political and market concerns by appointing Mr Cottarelli, a former IMF official, to run a technocratic government for at least until the end of this year.

News of the collapse of the Italian antiestablishment coalition boosted the Euro during our APAC session yesterday, pushing the currency to an intraday high of 1.1728. But when markets opened in Europe, it became evident that an Italian technocratic government led by Mr Cottarelli, known as “Mr Scissors” for his cuts to public spending in Italy in the past, was unlikely to win a vote of confidence by parliament with both Five Star and League fiercely opposing his appointment. As a result, Italy now looks more likely than not to head back to the polls late in the European summer with the election campaign likely to be run on Italy’s relationship with Europe.

The League, more so than Five Star, has enjoyed a rise in popularity in recent weeks, suggesting that in a new election they could be the party that outperforms. So the prospects of an anti-European Italian government has triggered a sell-off in both Italian bonds and equity markets. The FTSE MIB closed 2.01% and the Stoxx 600 Europe ended 0.32% down with Italian banks among the biggest losers. BTPs (Italian sovereign bonds) endured a brutal sell-off with the move lead by the front end of the curve. The 2y yield ended the day 40bps higher at 0.83%, taking the 2 year Italian-German spread to 160bps,50bps wider on the day and its widest level since late 2013, towards the end of the Eurozone sovereign crisis. Meanwhile after briefly rallying at the open 10y BTPs closed 22bps higher at 2.66% with the spread to 10y Bunds ending the day at 232.7bps. The market has pushed the first (10bp) ECB rate rise out to October next year and safe haven demand for German bunds spilled over into other major bond markets, with the US 10 year Treasury futures yield down 7bps (implying the 10y rate at 2.86%, its lowest level in over a month).

The EUR quickly gave up its gains from the Asian trading session dropping around 1% to an overnight low of 1.1608 before settling at 1.1624 where it currently trades. Worth reiterating here that given both the US and UK markets were closed for public holidays, thin trading conditions could have played a role on the price action overnight, so tonight’s session will be closely watched for any evidence of contagion risk.

Looking at price action in other currencies, overnight moves have been reasonably contained. European currencies have followed the euro lower with a higher beta fashion, both NOK and SEK have underperformed the euro, falling 0.33% and 0.66% over the past 24hrs. Notably CHF didn’t enjoy a safe haven bid with the pair down 0.26% against the USD. JPY is little changed after initially losing ground during our APAC session (USDJPY now at ¥109.41).

After trading to a monthly low of 0.7412 on May 9th, the AUD has remained contained in 0.7488-0.7605 range over the past 10 trading days and now the pair trades at 0.7544, sharply unchanged over the past 24hrs. The AUD has managed to hold its ground thanks to mixed to stable commodity prices and overall resilient risk appetite. So far Emerging Market concerns, geopolitics and now Italy have not triggered a wider risk off environment, so as along as contagion risk remains contained, the AUD is likely to remain supported.

Last but not least, the NZD followed the EUR higher during the local session yesterday as the market initially reacted positively to Italian political developments. The NZD reached a high of 0.6960 before Sydney’s close, but then it faded to 0.6940 over the remainder of the trading day as Italian fears mounted and the EUR resumed its decline. The net result was that the NZD is around 0.3% higher on the day, the best performing G10 currency (as it continues to recover from its sharp decline between mid-April to mid-May).

Coming Up

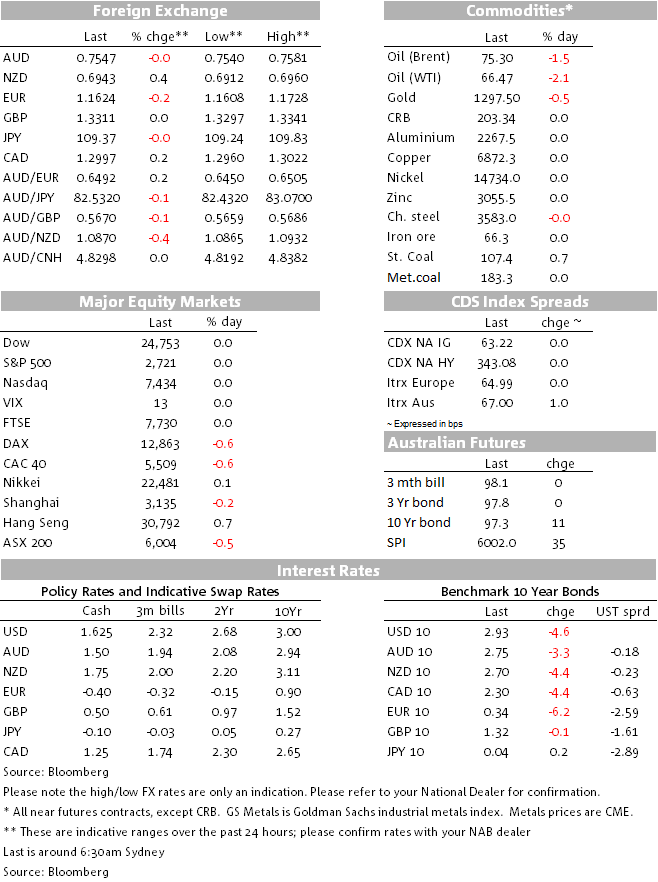

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.