Price growth edges lower despite reasonable economy

Insight

The FOMC delivered a hawkish tilt for Christmas with the Fed dot plot showing three rate hikes in 2022 while also accelerating the taper profile.

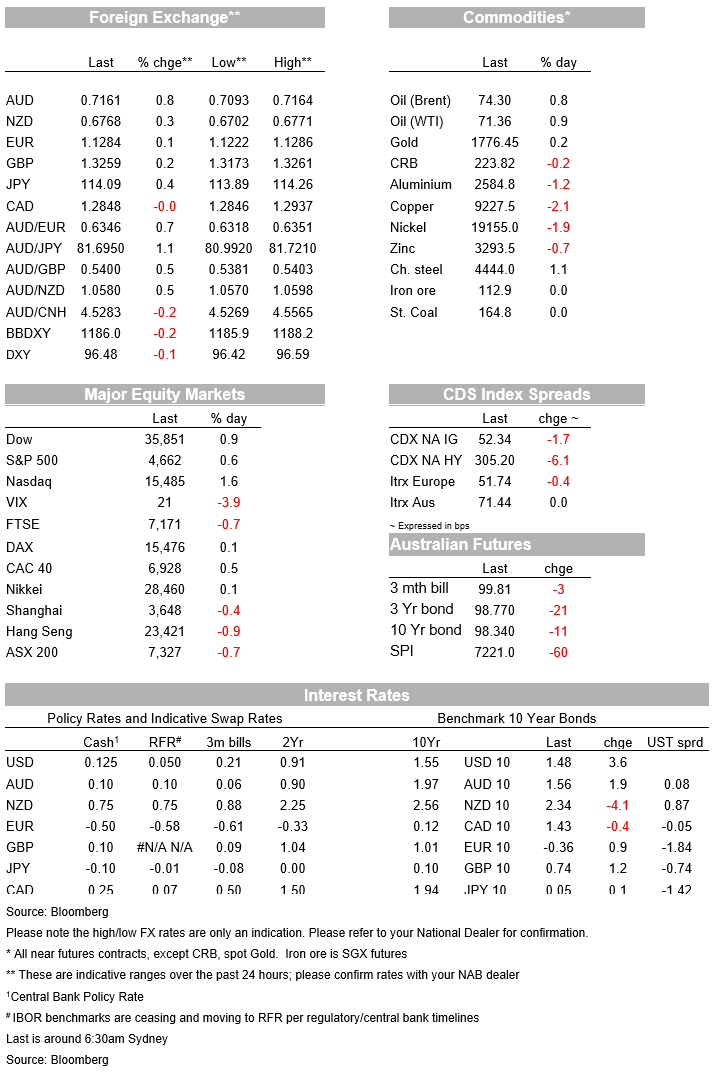

The FOMC delivered a hawkish tilt for Christmas with the Fed dot plot showing three rate hikes in 2022, while also accelerating the taper profile to $30bn from $15bn and which would see QE end by March. Markets seemingly have taken the tilt in their stride given three hikes were close to being priced into the meeting and expectations were high for an accelerated taper profile. Chair Powell also provided mixed tones in his press conference with the market seemingly paying more attention to his inflation comments with 10yr implied inflation breakevens initially dipping before reversing to be up 2bps to 2.42%. Nevertheless, Powell didn’t think the Fed was behind the curve and would take stops “in a thoughtful manner”. The US 10yr yield is now up 3.6bps to 1.48% with similar moves being seen in 2yr yields (0.68%) with the 2/10s curve broadly flat. Fed Funds Futures are broadly in line with the dot plot for 2022 with 73bps of hikes priced with a hike by May 2022 now 90% priced. Risk sentiment remains positive with the S&P500 well in the green at +0.6% at the time of writing, while the USD is down post Fed with BBDXY -0.2%.

For your scribe the key takeaway point was the Fed’s Core PCE forecasts which point to the need of a further hawkish tilt in 2022. The Core PCE inflation forecast is now well above the 2% target at 2.7% in 2022 (2.3% previously) and at 2.3% in 2023 (2.2% previously). One gets the impression on that profile that the Fed could move as early as March 2022, though of course the Omicron variant is one key uncertainty as is the taper profile which plays to the view of the first rate hike being in May 2022 and which is 90% priced. As for details of the Fed dot plot, every Fed member now sees the case for rate hikes in 2022, an important distinction given they were split 9 v. 9 at the September. Importantly 10/18 seethe case for three hikes and 2/18 see the case for four hikes. As for 2023, the consensus is for another three hikes, while the longer-term ‘neutral’ dot was unchanged at 2.50% (see FOMC SEP for details and the Fed Statement).

FX moves are still evolving as markets react to the FOMC statements. The US Dollar is now down -0.2% on the BBDXY after having risen into the FOMC, with most currency pairs higher post FOMC. The EUR is +0.1% and GBP +0.2%. The AUD outperformed over the past 24 hours up some 0.8% to 0.7161 ahead of three key risks events – jobs, RBA Governor Lowe and MYEFO (see coming up for details).

As for other data pieces overnight, UK inflation surprised to the upside again. Annual headline CPI inflation rate broke the 5% mark at 5.1% y/y (consensus 4.8%), while there was a similar three-tenth surprise on core inflation at 4.0% y/y against 3.7% expected. With core inflation now double the BoE’s target, there is clearly more pressure on the BoE to get along with it and start to normalise policy after having bottled it at the last meeting. Markets are now back to pricing in almost a 50% chance of a 15bps rate hike at today’s BoE’s meeting, though the consensus is the BoE will hold fire and wait until the fallout from the Omicron variant becomes clear. Overnight, the UK reported 78,610 new COVID19 cases, the highest since January with the Chief Medical Officer warning a big rise in hospitalisations is “a nailed-on prospect”, asking people to “de-prioritising” other social contact.

US retail sales were much weaker than expected in November, but the level of sales remains very elevated. Headline sales were 0.3% m/m vs. 0.8% expected and 1.8% previously. The core control group was even weaker at -0.1% m/m against 0.7% expected. There was though little reaction to the data coming before the Fed, and it is worth noting the miss comes after three very strong months in which core control sales rose by an average of 1.6% m/m. As for components, weakness was led by the electronic store sales which fell -4.6% m/m after lifting 3.1% in October, perhaps suggestive of people having brought forward their end of year shopping. Meanwhile north of the border Canadian inflation remained high, at 4.7% y/y for headline and 2.7% y/y for the average core figures in November, both in line with expectations.

A busy day both domestically and offshore. There is a trifecta of Aussie events with RBA Governor Lowe speaking, jobs data, as well as the last budget update. Offshore NZ has Q3 GDP, while the big risk events are the ECB and BoE, along with the global PMIs. See details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.