Price growth edges lower despite reasonable economy

Insight

The US economy is travelling with some momentum along side a tight labour market and still elevated inflationary pressures

https://soundcloud.com/user-291029717/markets-still-at-odds-with-rba-and-ecb-whos-right?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

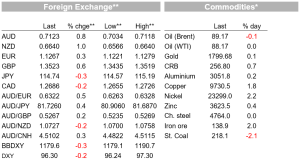

US equities have traded in and out of positive territory, consolidating the decent gains over the past two days, meanwhile EU equities have played catch up with the Stoxx 600 closing with gains over 1%. 10 UST yields are little changed with core European yields the focus, rising amid an increase in the Union’s inflationary impulse. The risk positive backdrop has kept the USD on the back foot with the NZD and AUD soaking up the sun, regaining ground from oversold positions. AUD is back above 71c while NZD is back above 66c.

After two days of solid gains which saw the NASDAQ climb 6.54% and the S&P 500 4.32%, US equities are taking a breather consolidating the gains from previous days. US stocks have traded in and out of positive territory, but the last hour of power is proving to be yet another positive one with the NASDAQ now up 0.30% and S&P 500 now trading +0.32%. European markets have played catch-up to the late-day rally in US equities yesterday, with the Euro Stoxx 600 closing the day 1.3% higher.

Overnight US data releases helped reaffirmed the notion that the US economy is travelling with some momentum along side a tight labour market and still elevated inflationary pressures, a recipe that justifies the need for the Fed to starts a new tightening cycle next month. The ISM manufacturing index slipped for a third successive month to a still-high 57.6, as expected. Commentary from the survey noted that the US manufacturing sector remains in a demand-driven, supply chain-constrained environment, but January was the third straight month with indications of improvements in labor resources and supplier delivery performance. Still, there were shortages of critical intermediate materials, difficulties in transporting products and lack of direct labour on factory floors due to the COVID-19 omicron variant. Looking at some of the subindices, the key measures of supply chain disruptions eased again, notably the order backlogs index falling over 6pts to a 15-month low. Prices paid jumped nearly 8pts, but this can be put down to the rise in oil prices.

The JOLTS report was also out last night and after Fed Chair explicit reference to the report last week as evidence of a tight labour market, the overnight update has done little to dissuade this view. The survey was surprisingly strong in the face of the Omicron hit to the economy – job openings rose to 10.9m, to near record highs, while the quits rate barely fell at 2.9%, still near its record high. The market is looking for a soft Omicron impacted non-farm (150k exp.) and ADP (184 exp.) reports this week, the JOLTS survey supports the view that this is likely to only be a temporary blip.

Meanwhile US earnings reports were mostly positive, supporting the consolidation theme in the overnight price action. Exxon Mobil recorded its highest earnings in eight years on aggressive spending cuts. UPS projected annual sales above expectations and in Europe UBS boosted its buyback program after an earnings beat.

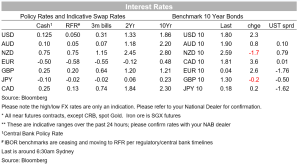

10y UST yields have traded a widish range of 1.74-1.82% and currently sits just 2bp higher for the day at 1.80% with the curve displaying a steeping bias as the 2y rate has eased 2bps to 1.162%. After some talk of the potential for a 50bps hike in March, the upward pressure in front end US yields has been easing somewhat with Fed Harker overnight joining the chorus for a 25bps hike next month and four 25bps hikes this year while also pushing back on a 50bps hike unless inflation spikes. On the topic Harker said “Could we do 50? Yeah. Should we? Well, I’m a little less convinced of that right now,”.

European core yields are also showing sign of life with the move up in the 2y German yield above the -0.5% ECB deposit rate for the first time since 2015 stealing a few headlines . Over the past week the 2y Bund yield has gained nearly 20bps from a low of 0.66% on Jan 24 to -0.489%, a change in Fed rhetoric is lifting all boats, but the EU inflation narrative has also played a part. The market has been increasingly seeing the chance of the ECB hiking rates this year, as the inflationary impulse grows. Overnight, French CPI inflation positively surprised, following the stonking German and Spanish CPI reports yesterday, adding further upside risk to the prevailing consensus for euro area CPI data tonight, ahead of the ECB meeting later this week. On market pricing, the ECB is expected to increase the deposit rate by 10bps to minus 0.4% in September, with a full 25bps priced by year-end. Both don’t expect the ECB to sanction this view later this week.

Moving on to the FX market, the risk positive backdrop has kept the USD on the back foot with the greenback softer across the board . In index terms DXY now trades at 96.37, a decent move lower from last week’s high of 97.41. Antipodean currencies have led the charge against the USD over the past 24 hours with NZD at the top of the leader board, up 0.9% to 0.6641 while AUD has edged up by 0.7% to 0.7124 currently. As noted early in the week, after last week underperformance, both currencies looked oversold to us with month end rebalancing also likely playing a dampening role, specially for AUD. Yesterday the RBA statement proved to be only a temporary disruption in the AUD recent ascendency, while playing the patient card we judged the RBA’s revised forecasts as consistent with a late 2022 rate rise, AUD price action would suggest a similar conclusion reached by the market. RBA Governor Lowe speaks today and hopefully we will get more clarity on the RBA’s thinking (see more below),

Of the other majors, GBP is one of the better performers, up 0.5% to 1.35. Despite the focus on German yields and where the ECB might take rates this year, the euro has remained on the softer side of the ledger, barely higher at 1.1260. CAD is also little changed, notwithstanding a solid Q4 GDP print. Canadian GDP was stronger than expected, with November beating estimates and the stats department estimating growth of 1.6% q/q in Q4, or an annualised rate of 6½%, ahead of the Bank of Canada’s projection of 5.8%, reinforcing the likelihood of a first rate hike for the cycle at its next meeting

Finally, on Ukraine news Russian President was again critical of the US and its allies for “deceiving” Russia over NATO’s expansion but suggested further talks may yield a resolution. Let’s hope so!

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.