Price growth edges lower despite reasonable economy

Insight

The markets continued to react to President Trump’s stance on steel tariffs, with his resolve seemingly increasing over the weekend.

Phil Dobbie asks NAB’s Rodrigo Catril how far the influence will reach this week.

https://soundcloud.com/user-291029717/my-tariffs-are-bigger-than-your-tariffs

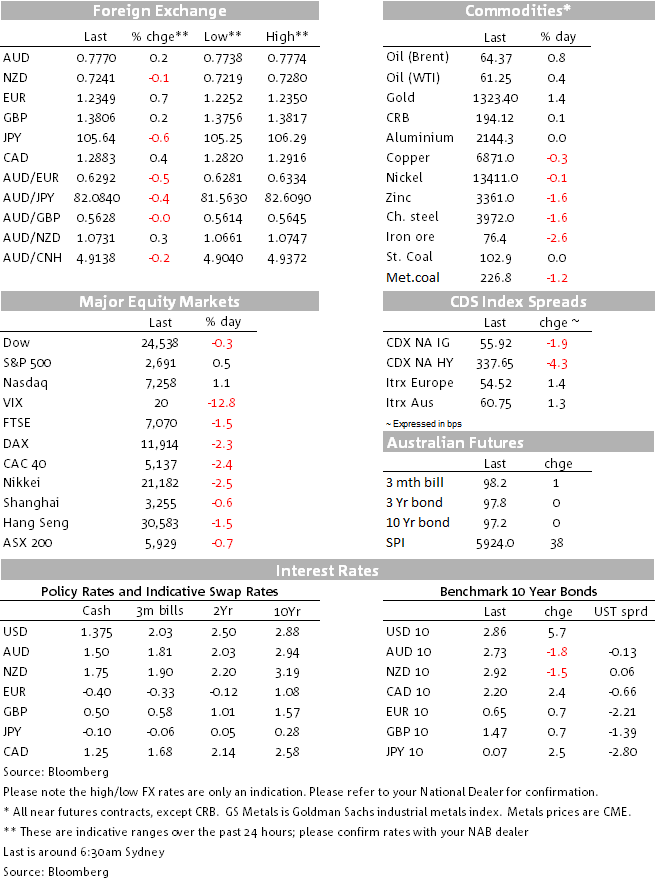

European equities closed Friday sharply lower, but US equities ended mostly higher amid an increase in trade tension rhetoric by president Trump. The USD continued to drift lower on Friday and the US Treasury curve bear steepened, likely reflecting inflationary concerns from trade tariff impositions.

In a Tweet on Friday morning President Trump said “trade wars are good, and easy to win”, increasing trade tensions and concern by the market. His tweet sparked further rebukes by trading partners and international bodies. Over the weekend Fed Kashkari also weighed in on the debate saying that “I am sympathetic to the desire for fair trade but I am nervous that there will be economic cost to the US economy in trying to show that the threat is credible”.

A full-scale trade war is not good for global growth and risk sentiment, the imposition of trade tariff is also likely to be inflationary for the US as domestic consumer will have to pay more for steel and aluminium and the risk of retaliations suggest that other sectors in the economy could end up getting hurt too. All that said we are not there yet and the response from China and other trading partners to an official US trade tariffs announcement will be important in this regard. China’s excess steel capacity is a known story and putting aside President Trump’s colourful language, the President does have a point; by many measures the US is less protectionists than China, Japan and Europe so a good outcome would be for everyone to yield a little bit.

For currencies the initial reaction to US led trade tensions is a negative for the USD, but we think that an escalation of these tensions will result in a differentiation between safe haven currencies and currencies from small open economies. AUD, CAD and NZ as well as EM currencies are unlikely to be winners under such scenario.

The US dollar closed Friday weaker in index term and softer against most G10 with the CAD (-0.35%) and NZD (-0.18%) the only G10 currencies weaker than the greenback. Canada is the US biggest steel importer, so CAD’s underperformance is not surprising. Canada’s Q4 GDP also disappointed on Friday (1.7% vs 2% exp.), meanwhile after a decent run in the previous day, NZD weakness/profit taking looked overdue. NOK was the big winner on Friday, up 0.72%, after the Finance Ministry announced its decision to lower the Central Bank’s inflation target to 2% from 2.5%. JPY also gained on Friday ( 0.46% at ¥105.64) aided by comments from Governor Kuroda acknowledging for the first time that a tightening in policy was likely in FY19 (Apr-19 to Mar-20) given the BoJ expectations for inflation to climb above 2% by then.

The AUD range traded on Friday, it reached an intraday low of 0.7738 and closed the week at 0.7756 (the pair now trades at 0.7769). GBP was also pretty stable on Friday, closing the week at 1.38 and showing little reaction to PM May Brexit ’s speech. The PM warned, “no-one will get everything they want” out of Brexit negotiations but she is confident a deal can be done.

Overnight, Members of Germany’s Social Democrats (SPD) voted in favour of a coalition with Merkel’s conservatives, eliminating a tail risk for EU markets and opening the way to a new government for Europe’s largest economy. The euro is little changed this morning at 1.2348. Meanwhile voting is underway in Italy for a new government and the first exit poll should be delivered around 1 pm Sydney time. The likely result is a hung Parliament, with the 5-star movement gaining the most seats but unable to form a majority government. This sort of political gridlock is par for the course for the country.

US Treasury yield moved higher on Friday with the move led by the back end of the curve. The 10y tenor ended Friday at 2.86%, essentially unchanged on the week and the 2y note closed at 2.243%, also little changed.

Commodities had a mixed Friday, risk aversion supported gold (1.39%), oil prices were marginally higher, but Met coal and iron ore were the big losers down 1.2% and 2.6% respectively. The story for the week, however, was for weakness across the board with met. coal and oil leading the way.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.