Price growth edges lower despite reasonable economy

Insight

On #TheMorningCall Phil Dobbie asks @NAB’s Ray Attrill if we could be a favoured state that avoids steel tariffs.

As Phil Dobbie discusses with NAB’s Ray Attrill, we know Canada and Mexico have been excluded from the new measures, but there’s a chance Australia might also be given preferential treatment.

https://soundcloud.com/user-291029717/will-australia-make-it-to-trumps-exclusion-list-ecb-unanimously-says-very-little

Just as after we hit the send button on today’s missive, President Trump is due to convene a meeting in the White House where he intends to finalise his tariff proposal on steel and aluminium imports, with the hope of getting it signed into law tonight (though it might not be until Friday or early next week due to legal/drafting considerations). What does now seem probable is that not just Canada and Mexico but also Australia will be exempted from the tariffs, based on the strong military ties between the US and the Australia and, as Mr.Trump has explicitly noted, the fact the US runs a trade surplus with Australia.

While the numbers involved aren’t huge (just over $200mn worth of Australian steel, and the same again of aluminium, are exported to the US each year) what such a move would confirm is that the US’s trade angst is really only directed at China (and Germany) not most of the rest of the world. While Australia would doubtless suffer significant collateral damage were the US and China – and/or the US and EU) to get into a tit-for-trade war that further slows down global trade – largely via reduced commodity demand from China – this is more tail risk than something we should have as a central scenario.

That said, Mr Trump’s maths has been corrected. The White House has says it now wants to see a $100bn reduction in the bilateral US-China trade deficit – that’s almost a third – not the $1bn he tweeted yesterday which as my colleague Jason Wong noted, amounts to no more than a rounding error. That’s a big challenge and keeps the threat of further US action against China very much on the table as we head toward the November mid-term US elections.

The other main news overnight is the ECB, who as expected tweaked their policy guidance to drop the so called easing bias, meaning a willingness to increase the size and duration of the QE asset buying programme if necessary. But there was no guidance as to when the purchase programme would end (not before September at least) or when rates might start to rise (not until well after asset purchases cease). All as expected, with any guidance on these latter two matters not expected until June at the earliest.

In itself this was not market moving, but Mr. Draghi succeeded in talking the Euro – and Eurozone bond yields – down in his ensuing press conference. Draghi down-played the removal of the easing bias, saying it was ‘backward looking’, noted that inflation remained subdued and that policy would be “reactive not proactive”, as well as warning that trade protectionism presents a new downside risk. Not really worth a big figure on EUR/USD in our view, but the market spoke otherwise.

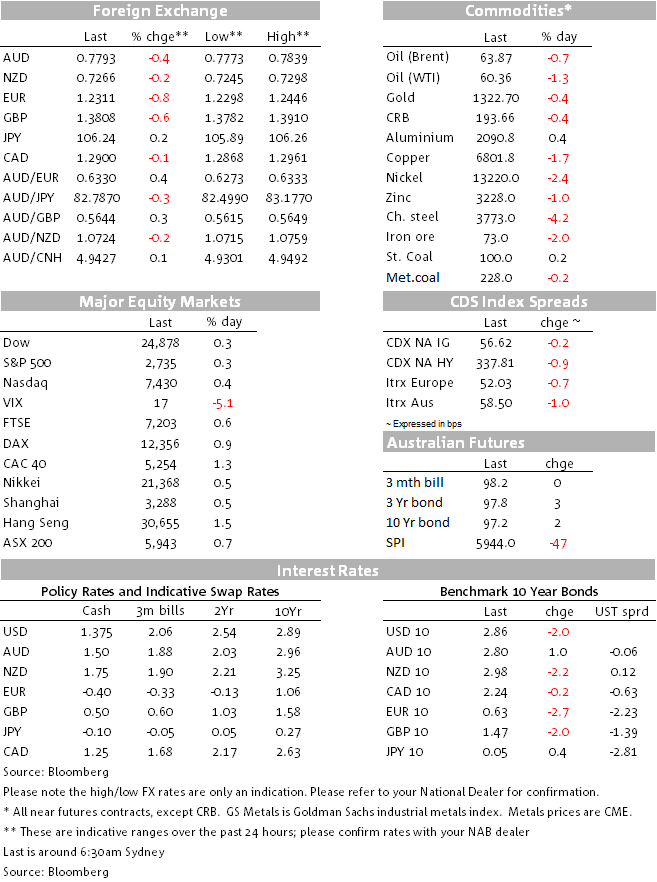

Post-ECB EUR/USD weakness has been the main driver of the 0.8% gain for the DXY dollar index but with gain now being checked by a big gains for CAD on incoming news headlines that Canada and Mexico will be exempted ‘indefinitely’ from steel and aluminium tariffs. USD strength is also evident elsewhere, pulling AUD/USD back down through 0.78 after spending much of yesterday above the figure (0.7790 now).

US equities are showing small gains an hour ahead of the close, US Treasury yields are fractionally lower while in commodities oil has had another bad night (WTI crude off nearly $1) while iron ore has lost another $1.50 and is now $5.50 a tonne lower than a week ago.

Tariff news out of the White House will be hogging the headlines during our morning. While rhetoric on trade has ruled the roost all week, tonight hard data is set to triumph with the all-important February US payrolls report (Canada employment data also due). US non-farm payroll growth is seen at 200k, the unemployment rate down 0.1% to 4.0% (new cycle low) and more important than either, average hourly earnings is seen +0.2% on the month and so easing to 2.8% y/y from 2.9% in January.

The latter implies that last month’s drop in annual growth to 2.9% from 2.7% was partly an aberration (i.e. a weather related boost, with those unable to work because of the weather likely to have been lower paid workers, biasing up the average of those in work). If this fails to prove the case and earnings rise by 0.3% or more on the month expectations for a lift to the Fed’s median ‘dots’ out of the March 20/21 FOMC meeting will rise.

In our time zone, we get the BoJ (policy will be unchanged, and there are no new forecasts this month). Also China CPI/PPI.

Europe has industrial production from Germany, France and the UK, and also UK trade.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.