Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Airline stocks have taken a heavy hit after Warren Buffet’s decision to bail out at the weekend.

https://soundcloud.com/user-291029717/airlines-take-a-beating-german-judges-to-rule-on-qe?in=user-291029717/sets/the-morning-call

The undercurrents never cease, Ambition’s such a tease,

The undercurrent’s always there, Our hopes are hard to bear – Maximo Park

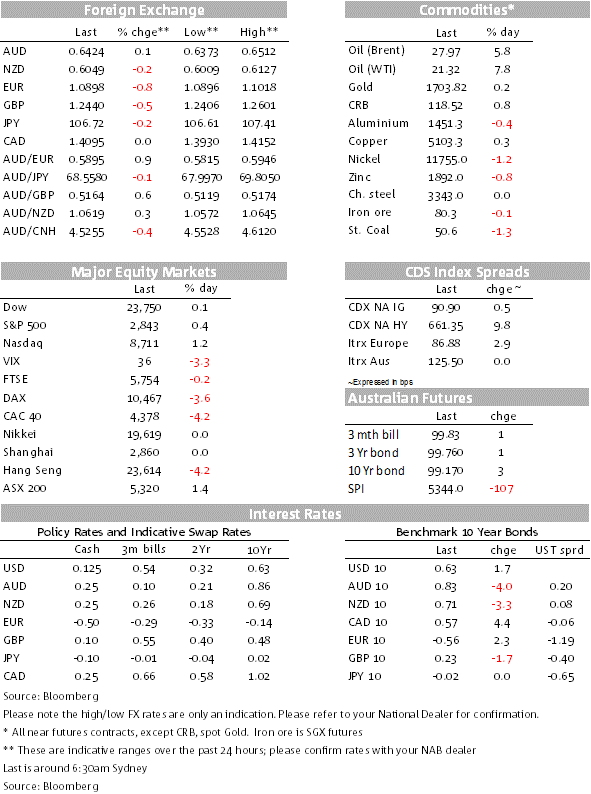

It’s been a subdued start to the new week with many European equities playing catch up after a day off on Friday. US equities have recovered after a negative start with airlines stock feeling the pain from Warren Buffet’s weekend rejection. Meanwhile oil prices are up helping energy stock and some commodity linked currencies along the way. Undercurrents, however, still give a sense of risk aversion with US-China tensions on the rise and no official response from Beijing as the country is still on holidays. The Euro the G10 underperformer ahead of German constitutional court decision tonight.

Warren Buffet’s confessions over the weekend reverberated on US equities on Monday with airlines stocks taking a heavy hit after the oracle of Omaha admitted to no longer being in love with them. Buffet increase in cash reserves and lack of optimism on the outlook didn’t help sentiment either. The S&P 500 airlines subsector ended the day down 5.93%. On the other hand the move up in oil prices helped energy stocks perform (Top S&P 500 sector +3.71%) with IT also up at 1.47%. So after a poor start, US equities have managed to crawl back into positive territory with the S&P 500 ending the day at 0.42% and the NASDAQ up 1.23%.

All major European equity indices ended the day in the red with the CAC-40 the big underperformer down 4.24% while the STX Europe 600 closed at -2.65% . Most of Europe enjoyed labour day on Friday, so the market played catch up overnight.

That said, there’s still a sense of risk aversion in the air. US-China tension have moved up a notched over recent days with the US administration publicly blaming China for the spread of COVID-19 and covering up the issue. Overnight, Treasury Secretary Mnuchin said that Trump was reviewing options he has to penalise China. So far there has been little evidence of China ramping up imports from the US as agreed in the Phase 1 trade deal signed earlier this year. Meanwhile with China still celebrating an extended Labour day holiday, there has been no official response to the US accusations over the past couple of days. But the official news agency Xinhua on Monday accused Mr. Pompeo of speaking “nonsense” and telling “lies,” while a news reader on China Central Television called the secretary “evil” and said he was “spitting poison.

Market sentiment has also been held back as investors wait for Germany’s constitutional court final ruling tonight on the legality of the ECB’s asset-purchase programme, a case that has dragged on for nearly five years. The case, filed by a group of conservative businessmen and academics argues that the ECB is overstepping its authority with the QE program and removing the incentive for EU countries to pursue sound fiscal policy. Expectations for a ruling against the ECB are low, but a negative ruling would be a shock to the market and prevent the ECB from going full steam ahead with its €750b Pandemic Emergency Purchase Programme, which removes many limits that constrained its previous asset purchase programmes.

Some nerves ahead of that judgement see the European currencies at the bottom of the leader board. EUR is down 0.72%, and has slipped below 1.09 this morning. GBP is down 0.5% and found some support just above 1.24 overnight.

The AUD and CAD have joined the JPY as the only currencies recording (modest) gains against the USD. The move up in JPY can be justified by the cautious sentiment in the air, favouring JPY safe haven attributes ( USD/JPY now trades at Y106.75) while gains in AUD (now at 0.6427 +0.14% and CAD @1.3087 +0.03%) can probably be attributed to gains in oil prices. WTI is up just over 7% over the past 24 hours while Brent is up 5.79%. Oil prices are up for a fourth consecutive day with gains overnight assisted by a Genscape report noting a 1.8m /b build in inventories in Cushing, Oklahoma, the delivery point for West Texas Intermediate crude. If the US government reports a similar number Wednesday, it would mark the smallest increase at the hub since mid-March.

The NZD is the weakest of the commodity currencies, down 0.3% to 0.6048, after finding some support around the 0.6010 mark over the past 24 hours. The RBNZ’s aggressive QE stance is NZD-negative as the Bank’s actions continue to drag NZ rates down, with falls to record low levels across much of the curve – NZ’s benchmark 10-year government rate (2031) closing down 4bps to 0.73% and the 3-year bond trading down to just 0.07%. The 5 and 10 year swap rates fell 2-3bps to record lows of 0.31% and 0.69% respectively. Many are beginning to question the RBNZ’s strategy here, given the overwhelming distortions it is generating in the market.

The overnight steepening on the UST curve has been led by the back end of the curve with the 30y bond up 3bps to 1.277% while the 10y rate is up 2bps to 0.6340%. Investment Grade Corporate issuance was a factor at play with longer dated tranches from Apple and Altria amongst others.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.