Price growth edges lower despite reasonable economy

Insight

US inflation has surprised again, up even higher than last month. But NAB’s Tapas Strickland says the indications are that it’s still transitory.

https://soundcloud.com/user-291029717/another-us-inflation-surprise-still-transitory?in=user-291029717/sets/the-morning-call

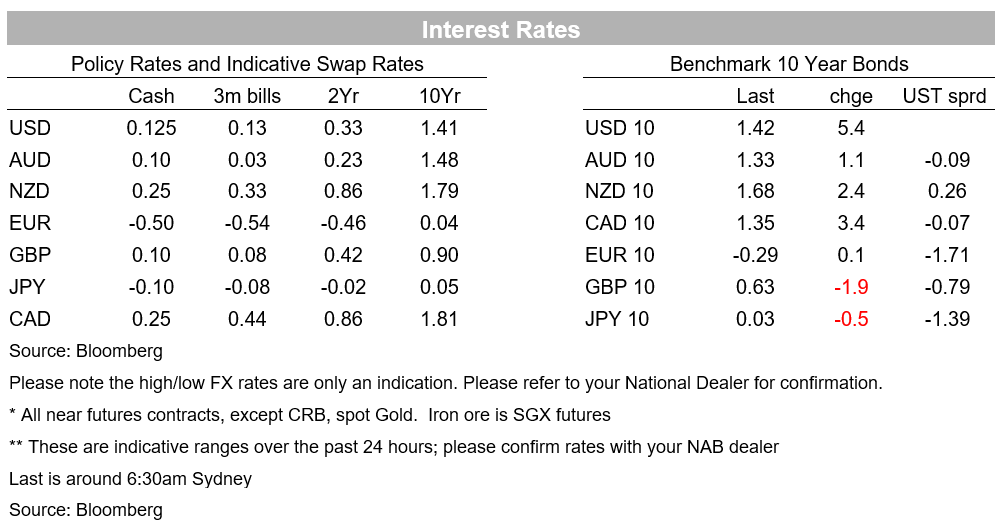

Another hotter than expected US CPI print has got the market wondering whether the lift in inflation will prove to be transitory or more enduring. The Fed’s Kaplan said he has raised his inflation forecast for the remainder of the year and into 2022, while the Fed’s Daly falls into the transitory camp where Chair Powell is also. Markets have sided on the hawkish interpretation, bringing forward rate hike expectations to late 2022, meaning markets also likely see tapering occurring in late 2021 assuming a 12m tapering profile. The curve meanwhile tells an interesting story of if the Fed were to hike earlier, then it may not need to tighten as much. The US 10yr yield initially fell slightly to 1.34% in the wake of the CPI, but then rose following a weak 30yr auction (auction yield was 2bps above the prevailing secondary market) with the US 10yr in the end +5.4bps to 1.42%. The 5s30s curve though still kept its flattening, down -1.8bps to 118.8bps. The USD (DXY) was unsurprisingly stronger, up 0.6% with broad-based gains. Equities fell, though weaker revenue numbers from the banks were also a factor.

As for the CPI print, both Headline and Core jumped 0.9% m/m in June, with Core more than double the market consensus of 0.4%. The annual rates which are being impacted by base effects were also much stronger than expected with Core at 4.5% y/y and Headline at 5.4% y/y. The key question for the Fed and markets in general is whether the sustained lift in inflation seen over the past couple of months is still likely to be transitory, or will it be more persistent, warranting an earlier normalisation in Fed policy. Within in the details there was enough to say the rise is mostly transitory. Used car prices accounted for almost half of the rise in core in the month with used cars up 10.5% m/m and adding 0.42% points to the month on its own. Used car prices are currently 45% higher than year ago levels and reflects the supply chain disruptions to the auto industry. More importantly, auction prices have dipped recently, and thus we could start to see used car prices reversing (potentially sharply) over the rest of the year. The other large rises in the month will also likely to prove transitory with hotel room rates up 7.0% y/y and airline fares up 2.9% (though airfares overall are still 9% below pre-COVID levels).

Fed speak in the wake of the CPI was mixed. San Francisco Fed President Daly in a CNBC interview played down the current spike in inflation as temporary, noting “several months of this doesn’t mean that it’s not transitory” and cited used cars as a prime example for why the lift in inflation will be transitory. Daly nevertheless still sees tapering occurring either in late 2021 or early 2022 (see CNBC interview for details ). Fellow FOMC colleague Kaplan sounded a little more hawkish in an MNI interview overnight, stating that he had revised up his inflation forecasts for the remainder of the year and into 2022. Kaplan continues to argue for a tapering of asset purchases and has also pencilled in a rate hike in 2022. As for Chair Powell, we have the opportunity to hear from him later tonight in his House testimony. Chair Powell is likely to keep to his transitory script, having previously noted lumber prices which have fallen 64.5% since their peak in early May after having skyrocketed during the pandemic – will used car prices tell the same story as the year progresses?

Inflation pricing/compensation lifted in the wake with the implied 10yr inflation breakeven widening to 2.37%, the highest since early June, but still nearly 20bp shy of the mid-May highs. The overall BEI curve though remains inverted, implying a market view that US CPI will moderate fairly quickly. Cleaner measures of inflation expectations such as the 5Y5Y forward is little changed at around 2.28%, a level broadly consistent with the Fed’s 2% target for PCE inflation.

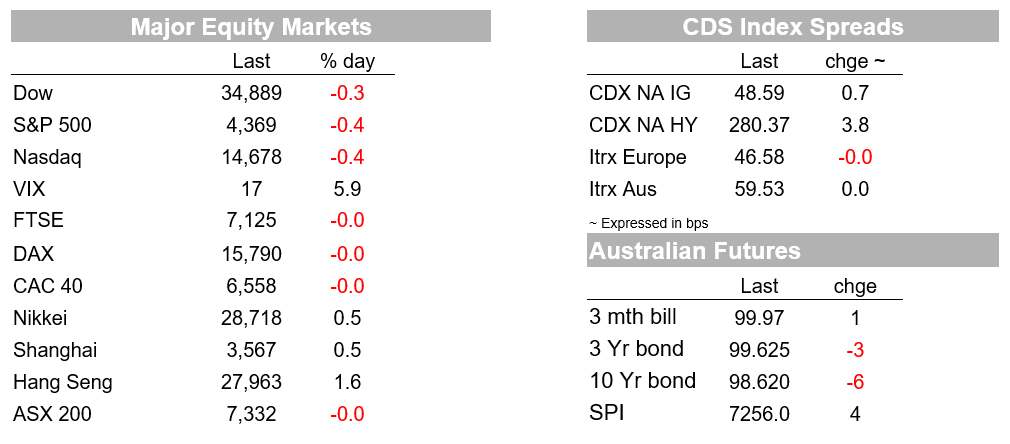

Equities also took the CPI mostly in its stride with the S&P500 closing down 0.4% with financials underperforming after weak revenue numbers from the banks. JPMorgan posted profit of $11.95 billion, on revenue of $30.48 billion, also beating expectations. While its profit more than doubled, its revenue fell 8%, a result of depressed lending margins and the lower trading activity.

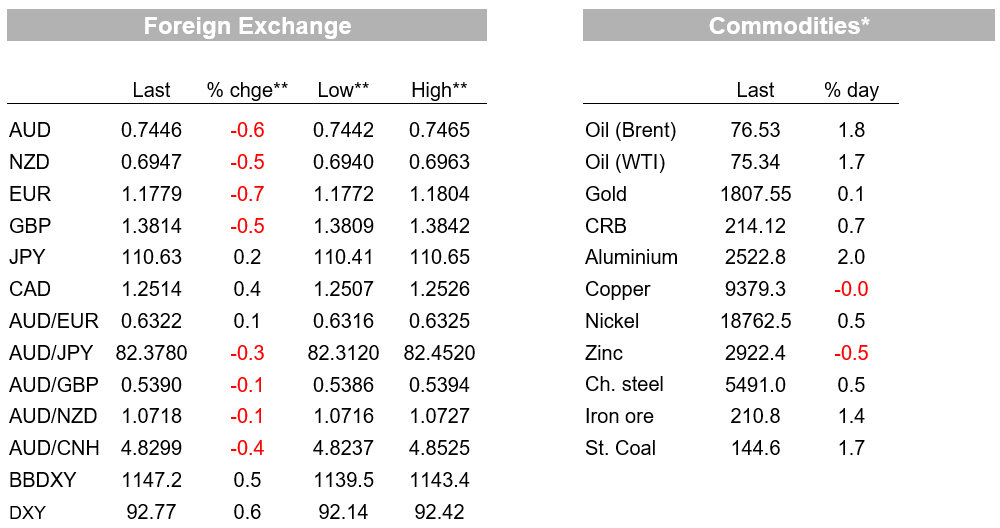

The USD has experienced a broad-based appreciation on the back of the upside surprise to CPI and the bringing forward of Fed rate hike expectations. The BBDXY index is up 0.5%, taking it back near the top of its recent range and close to a 3-month high. The EUR has fallen below 1.18 (-0.7%) and is trading at its lowest level since the start of April. The AUD and NZD are down 0.6% and 0.5% respectively.

Domestically we have the W-MI Consumer Confidence, though most focus in the Australian time zone will be on developments across the ditch with the RBNZ meeting. Internationally the focus remains on central banks with the Bank of Canada meeting and US Fed Chair Powell also gives the first of his Congressional Testimonies. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.