Price growth edges lower despite reasonable economy

Insight

There’s been feverish activity in equity markets over the last 24 hours as investors respond to the US-China trade deal and the removal of Brexit uncertainty (for now).

https://soundcloud.com/user-291029717/are-shares-heading-for-a-melt-up?in=user-291029717/sets/the-morning-call

US equities making new record highs in the wake of Friday’s Phase 1 US-China deal confirmation, however limited it may be, with bond yields smartly higher while the US dollar is weaker across the board bar USD/JPY (higher). A lot of European and US data overnight, where various Eurozone PMI numbers have disappointed but in the US, more confirmation via the NAHB Homebuilders index that the housing market is far and away the strongest feature of the US economy at present, thanks to still ultra-low 30 year mortgage rates and ongoing strong gains in employment.

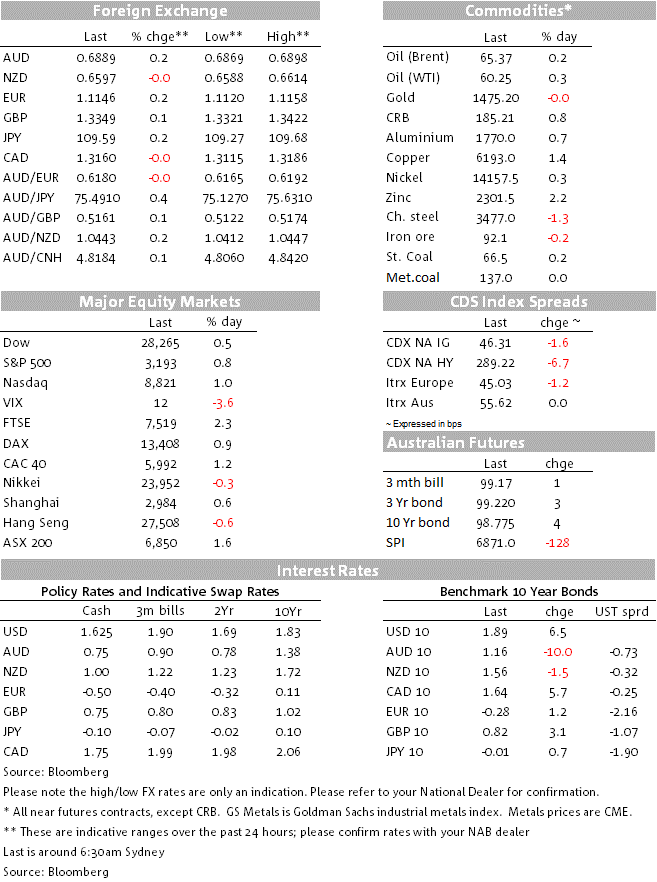

The reduction in uncertainty both with respect to the US-China trade landscape as we head into 2020 and in the UK post last Thursday’s election, has been enough to generate sizeable beginning-of-week gains for global equities, moves begun here in Australia yesterday where the ASX200 posted a 1.6% gain that was widespread across sectors. The S&P500 is into the last hour of trading showing a 0.8% gain (and the NASDAQ just over 1%). YTD gains are currently 27.5% for the S&P and 33% for the NASDAQ. Wow.

Bond yields in the US are currently up 6.5bps at 10 years and 3.5bps at 2-years, so reversing a good chunk of last Friday’s falls but still well shy of the intra-year highs of 1.97% for the 10-year back in early November, not long after the Fed had signalled it was now done cutting interest rates.

In fact besides a 2.8bps gain for the 10-year Bund and 5.1bps for gilts, they are lower. Here, disappointment that the various flash PMI data for Germany, France and pan-Eurozone didn’t come in better, is undoubtedly a factor. Germany’s manufacturing reading slipped back to 43.4 from 44.1 after two months of gains off the 41.7 September cycle low, a small (0.3) rise in services enough to ensure than the Composite reading was unchanged at 49.4 (so still in contraction territory). The pan-Eurozone Composite reading was also unchanged at 50.6. Evidence of green shoots turning into outright Eurozone economic recovery remain elusive and will at least now have to wait until 2020.

Now also produced in ‘flash’ first vintages, also disappointed, Manufacturing to 47.4 from 48.9 and Services to 49.0 from 49.3, putting the Composite reading at 48.5 – a new cycle low. Here, the approach of the UK election and uncertainty therein could have been a factor – we’ll only find out in a month’s time when flash January readings are published.

The US also had its Markit PMIs last night ahead of the more influential ISMs early in the New Year. These were fairly flat to slightly higher on November, Manufacturing at 52.5 (from 52.6), Services at 52.2 from 51.5 and the Composite 52.2 from 52.0. The Empire Manufacturing survey, the first of the regional (NY State) surveys dipped to 3.5 from 4. Finally and we say above, the more eye-popping US report last night was the jump in the NAHB survey reading, to 76.0 from 70. This is the highest reading since 1999. The report quoted NAHB Chair Greg Ugalde saying: ““Builders are continuing to see the housing rebound that began in the spring, supported by a low supply of existing homes, low mortgage rates and a strong labor market.” NAHB Chief Economist Robert Dietz added: “While we are seeing near-term positive market conditions with a 50-year low for the unemployment rate and increased wage growth, we are still underbuilding due to supply-side constraints like labor and land availability…. (but) higher development costs are hurting affordability and dampening more robust construction growth.”

FX markets have bene more subdued than equities or bonds, where outside of 0.3-0.5% gains for the SEK and NOK, the biggest mover has been the EUR (+0.2% – PMI data notwithstanding) and the AUD (0.2%) but still trading shy of the 0.69 level (high of -6898, 0.6891 now). Yesterday’s Mid-Year Economic and Fiscal Outlook (MYEFO) revealed downgrades to the economic outlook. Growth is slower in the near term and the government has reduced its expectation for wages growth. This has forced the government to lower its expected budget surpluses, where it now forecasts only small surpluses (ranging from 0.2 to 0.4% of GDP) in the next four years. Given the average forecast error for the MYEFO forecast of the current financial-year budget outcome is 0.6% of GDP, the lowered surplus outlook suggests there is a risk that the government does not deliver a surplus in 2019-20. The government did not announce any material fiscal stimulus, with additional spending – on drought, aged care and a slight bring-forward of infrastructure projects – only totalling $1.2b in 2019-20 and $1.1b in 2020-21. This suggests the RBA will have to continue to carry the burden of supporting growth. See our latest Australian Markets Weekly for more.

Also yesterday’s China’s slug of monthly activity data were all on the positive side of expectations, industrial production particularly (6.2% from 4.7%) though all the numbers have to be seen in the context of the October falls linked to the 70th Anniversary of the founding of the PRC. In YTD terms, growth rates were little changed.

NZ has Q4 Westpac Consumer Confidence and December ANX business confidence, the latter the main draw for NZ markets, at 13:00 AEDT.

The RBA December Board minutes are the main event here. The surprise in November was that the Minutes, unlike the earlier post-meeting statement, revealed that the Board “agreed that a case could be made to ease monetary policy”, but chose to stay on hold and wait for “another full assessment”. Whether or not they repeat this phrase, implying an active discussion of a potential rates cut, would be market moving, vis-a-vis expectations for a cut when the RBA returns in February, but the essential message is expected to be that a pause for assessment (of the impact of this year’s three cuts) is warranted.

Australia also has details of October Home Loans. There will be significant changes to home loan approval figures, such that we have not forecast housing finance this month given the ABS is updating its data methodology, which will result in substantial revisions to history.

The US has Housing Starts and Building approvals and the JOLTS job openings plus industrial production, the latter seen +0.8% do fully reversing the 0.8% October fall)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.