Price growth edges lower despite reasonable economy

Insight

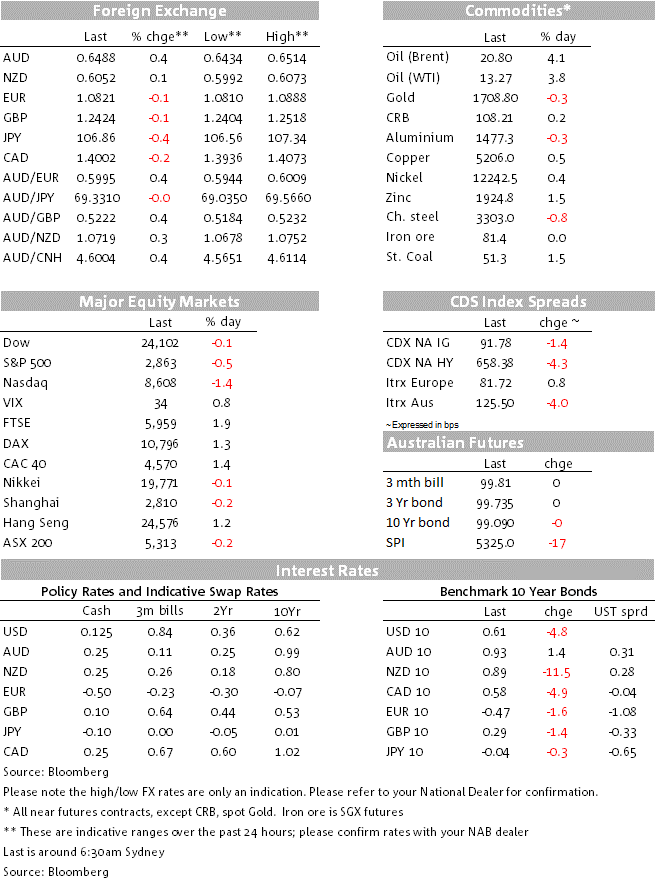

The Aussie dollar has been steadily rising, now around 65 US cents.

In what remains an essentially risk positive backdrop, the IT technology sector came under a bit of pressure during Tuesday’s session in front of Alphabet’s Q1 earnings report (as did Healthcare). Bond yields are lower again in front of the FOMC tonight while in FX the USD is weaker and AUD had pushed back above 0.65 for the first time since March 10. NZD has fully recovered from yesterday’s negative RBNZ rates scare.

Alphabet, nee Google, has just reported its Q1 result showing revenue up 13% on the same period last year and earnings per share of $33.71 against the $32.60 street consensus. The stock immediately jumped by just shy of 5% before stepping back a bit as I write. So as far as the ‘FAANGS’ reporting season goes, it’s now two down (after Netflix last week) and three to go (Apple, Facebook and Amazon) with no damage done to this sub-segment of the overall IT sector which remember makes up about a fifth of the entire market cap of the S&P500.

The NASDAQ ended the NY session -1.4%, underperforming versus the S&P (-0.5%) and Dow (-0.1%) but S&P futures during our session will likely be indicating a reversal during tonight’s US session given the Alphabet news. At the ‘old economy’ end of the spectrum, Ford posted a $2bn loss for the quarter and just missed its street EPS estimate, with its stock down over 4%.

Risk sentiment in general is seemingly still being supported by the backstop provide by the various central bank and other government policy pronouncements of recent weeks, but also COVID-19 related news flow vis-à-vis likely partial relaxations of social distancing strictures in various parts of the world in coming weeks (e.g. France re-opening shops on May 11, gradual relaxations of measures in Spain over the coming 8 weeks). And of course, Macdonald’s, KFC and (members only) golf is now available to our friends across the Tasman as of yesterday morning. Some small social ‘nearing’ steps are also afoot in Queensland and, later this week apparently, NSW.

FX markets may be seeing volatility well back from its last March peak, but this hasn’t stopped the AUD in particular continue to push ahead – or rather, in part because of declining volatility in other asset markets – albeit the run up in AUD this month has extended far beyond what the (quite limited) improvements in risk metric most pertinent to the AUD would justify. The overnight high of 0.6515 is the best level since March 10 while month-to-date, AUD is up by 5.8% against the USD which is over 4% more than any other G10 currency. This is quite extraordinary (it didn’t underperform the G10 pack by nearly as much in March) and does leave us a little cautious about the near term outlook, especially as the calendar clicks over the May. Yesterday NAB and BNZ’s FX strategy team revised up its forecast for AUD/USD to 0.6750 for end 2020 and 0.72 for end 2021 and while our end-Q2 forecast was also lifted, we have it lower than now (0.62).

The NZD had a volatile day Tuesday, falling quite heavily intra-day after Westpac, following at least one independent research firm before them, forecast the RBNZ going negative on the OCR (to -0.5%) later this year. NZD/USD loses have since been fully recovered in line with the improvements in other risk/growth sensitive currencies to be slightly up over the last 24 hours, albeit the AUD/NZD cross is marginally higher. The BBDXY USD index is 0.3% lower.

Bond markets have generally posted small price gains, with the UST 10y yield 4bp lower to 0.61%, effectively reversing the sell-off seen the day before. Our rates strategist notes that month-end index extensions are above average in the US and which looks to be supporting the long end of the curve. They also note demand for the US 7y auction overnight was average, after a solid showing in the 2y and 5y offerings this week.

The US Conference Board’s April Consumer Confidence reading plummet to 86.9 from 118, albeit close to expectations, led by a fall in the present situation reading from 167.7 in March to 76.4. Of note though, the expectations index actually improved, to 93.8 from 86.8, seemingly symptomatic of expectations that social distancing measures will start to be relaxed sooner rather than later. The Richmond Fed manufacturing survey plunged to -53 from 2, while the US Advance March trade deficit widened out to $64.2bn from 59.9b led by a 17.8% drop in auto exports.

The oil market remains jittery with the WTI June contract trading a 35% range between around $10.10-13.70. S&P, which runs the popular GSCI Commodity Index, changed its investment policy, doing an unscheduled roll out of the June contract to avoid the same issues that happened with the May contract – oil prices going negative – as storage for physical delivery remains limited. There has been some spill-over into Brent crude, which has also traded a wide range, albeit much less than that of WTI, between $18.70-21.30. Elsewhere in commodities base metal are mixed, iron ore futures are down 1% and gold +1%.

AU Q1 CPI this morning should show moderate inflation as higher grocery prices offset the fall in petrol. We expect a small 0.3% rise in the Q1 CPI, lifting annual inflation from 1.8% in Q4 to 2.2%, which would be the largest annual increase since 2014. The trimmed mean CPI – which is the Reserve Bank’s preferred measure of underlying inflation – is expected to rise by a further 0.4% in Q1, with annual inflation ticking up from 1.6% to 1.7%. the bigger CPI story will be for Q1 not Q1 though, where largely as a result of petrol prices and temporary free childcare, our economists have currently pencilled in a 1.9% quarterly fall, to take inflation into negative YoY terrain. territory

NAB’s forecast of a slight rise in the Q1 CPI may seem surprising given the pandemic and containment measures has seen consumer spending fall sharply around the world, with other advanced economies showing deflation in the month of March. However, falling prices in March overseas had little impact on inflation in Q1 as a whole. In Australia, the impact of the coronavirus pandemic and related containment measures escalated in the second half of March. As such, we expect a limited impact on the Q1 figures.

Instead, the key factors for our Q1 CPI forecast are the strong rise in food prices offsetting a fall in petrol prices and weakness in travel costs.

The Advance estimate of US Q1 GDP will show the early impacts of the pandemic (recall that initial jobless claims fell by over 10 million in the latter half of March) but which will be very much larger in Q2. Consensus is for a 3.8% fall in seasonally adjusted annual terms (so just under 1% QoQ) led by a 3.5% decline in personal consumption spending.

The FOMC will hand down its latest decision at 4:00 AET Thursday, and while there is am minority view that the Fed will offer some firmer guidance of the future pattern of QE bond purchases, the consensus view is that there will be no new policy initiatives out of this meeting, leaving the subsequent Pres conference from Fed chair Powell the main focus of attention.

New Zealand has March trade data this morning, and Germany its preliminary April CPI (expected to fall to 0.7% YoY from 1.4% in March.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.