Price growth edges lower despite reasonable economy

Insight

US shares are racing ahead again on earnings results and further evidence of a strong US economy.

https://soundcloud.com/user-291029717/us-equities-back-on-the-boil

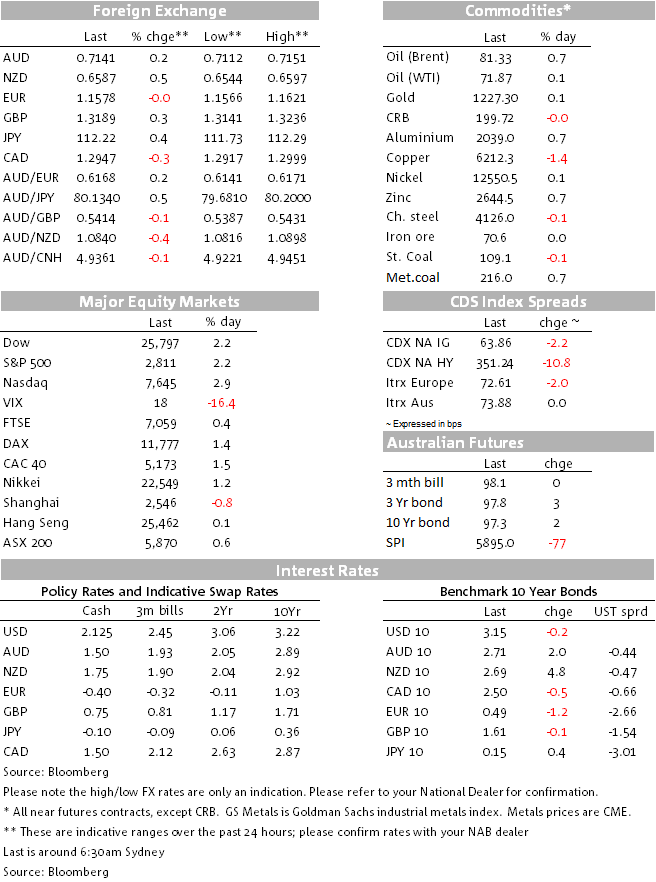

US stocks are back on the up, a 2.2% gain for the S&P 500 (led by the IT sector) which reduces the month-to date loss to 3.5% from 6.7% as of last Thursday and has pushed the VIX index back firmly below 20. This has done nothing for either US bond yields or the big dollar however, both effectively flat to Monday’s New York closing levels. The New Zealand dollar is the best performing G10 currency of the past 24 hours, holding the gains scored in the immediate aftermath of yesterday’s stronger than expected Q3 CPI data.

The inimitable Martin Wolf writing in today’s Financial Times (subscription required) has an excellent perspective on recent market events and which very much chimes with what we have been saying of late, both in terms of the battle between the old (US) and new (China) superpowers that implies the current Sino-US trade war is really the start of new cold war, and his take on the rise and recent fall in US stock market in the context of so-called ‘Cyclically Adjusted Price Earnings Ratio (CAPE) as developed by Yale University Professor and Nobel laureate Robert Schiller.

As per the thematic note published by my colleague Tapas Strickland last Friday noted, US equities measured in these terms are anywhere between 13% and 27% overvalued depending on what risk-free rate is used to discount corporate earnings.

Wolf writes: “Bull markets, it is said, climb a wall of worry. When the last worrier turns into a fully invested optimist, the market has nowhere to go but down. That might be what has just happened: so much optimism was already in the prices of financial assets — in the US, above all — that once worry returned they had nowhere to go but down. How far might unfolding events exacerbate the worries? A long way, is the answer”. He notes that the CAPE is, with the exception of the pre-1929 and dotcom crash levels, higher than it has been at any time in the last 137 years:

Anyway back to last night, and a ‘buy the dip’ mentality has evidently prevailed serving to push the S&P back above its 200-day moving average. Stronger earnings reports have supported the move (Goldman’s among those already reported, Netflix due after the close where analysts have been busy slashing earnings estimates ahead of their release). The data flow has been positive. The US JOLTS report showed US job openings rise in August to a fresh all-time high, exceeding the number of unemployed people by over 900k, the most on record. Both US homebuilder sentiment and industrial production figures were slightly ahead of consensus, the latter +0.3% versus the 0.2% consensus. With the IT sector leading the rally, the NASDAQ is up 2.9% as is the smaller cap Russell 2000.

Heading into the New York close, the 10-year Treasury yield is -0.4bp and the more Fed policy sensitive 2yr yield +0.6bps, so rally nothing to see here. Money markets still ascribe a more than 80% probability to the Fed lifting rates by another quarter percent in December.

Earlier in Europe, Italian 10-year BTP yields were off 9 bps, which as our London analysts’ note, is a little bewildering. This is as Italy submits its 2019 budget to the EU, saying it is ‘extremely happy’ that it is keeping with its election promises of not raising taxes of any kind. The budget essentially increases social spending and lowers the retirement age. Italy still foresees a deficit of 2.4% of GDP and it is not clear the EU will accept it. EU Commission President Juncker was reported today as saying the EU executive arm would face a revolt if it were to give its approval to the budget plan.

The New Zealand dollar followed by the Swedish Krone (the latter of late one of the more risk-sensitive G10 currencies) are both up 0.6% to top the leader board, with the safe-haven JPY and CHF both down, by 0.4% and 0.3% respectively. NZD gains are largely of the back of yesterday Q3 CPI report showing inflation coming in stronger than consensus at 1.9% yr/yr. Core measures of inflation were relatively steady, averaging around 1.7-1.8% although annual non-tradeable inflation was 0.2% higher than the RBNZ projected, alongside the 0.5% miss in headline inflation. Post-CPI, the kiwi rates market priced out some of the RBNZ easing risks in the OIS curve, with the implied probability of a rate cut by August 2019 falling from 24% to 18%.

The AUD meanwhile sits mid-pack at 0.7142 as I write, 0.15% up on this time yesterday. Worth noting that globally, emerging market currencies are generally stronger over the last 24 hours, with gains of over 2% for the Argentine Peso and Turkish Lire and of more than 1% for the Rand and Colombian and Chilean Peso. Yesterday’s RBA October meeting Minutes came and went without fanfare as far as the currency or rates markets were concerned. The next move is likely up, but not for good while yet, was the now familiar take-away.

On the big dollar, President Trump has been out on Fox News just now again railing against the Fed, saying he respects its independence but that ‘the Fed is raising rates too fast’ and that the Fed is his ‘biggest threat’. While such name calling shouldn’t mean anything in terms of what the Fed actually does, it is a factor which somewhat undermines sentiment towards the dollar and so, we’d argue, is a contributory factor, albeit minor, to recent poor performance of the US dollar in the face of first higher US yields then last week’s sharp turn for the worse in US equity market and with that the spike in the VIX. But of course, a weaker dollar is exactly what Trump wants. A method to his madness?!

A mixed night, with oil slightly firmer, precious metals slightly lower and base metals mixed (copper down but zinc and aluminium up, while iron ore is virtually unchanged and coking coal back up by $1.50.

RBA Deputy Governor Guy Debelle speaks on the State of the Labour Market is Sydney at 08:20 AEST this morning. His perspective on wages formation and the prospects for this picking up to levels more consistent with the mid-point of RBA 2-3% inflation target will be fascinating.

Tonight (or rather 5am tomorrow morning) we’ll get the September FOMC meeting Minutes, where particular interest in the Fed’s view of the neutral rate has been sparkled by chairman Powell’s comments on 5th October that “we are a long way from neutral”.

UK CPI and Final Eurozone CPI figures are due in Europe. More important, EU Leaders are having dinner, including with UK PM Theresa May ahead of their Summit tomorrow, with as yet no sign of a breakthrough in their discussions on dealing with the Irish border questions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.