Price growth edges lower despite reasonable economy

Insight

Globally yields are on the rise again.

https://soundcloud.com/user-291029717/bond-yields-rising-no-bazooka-on-the-way?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

The Final Countdown – Europe

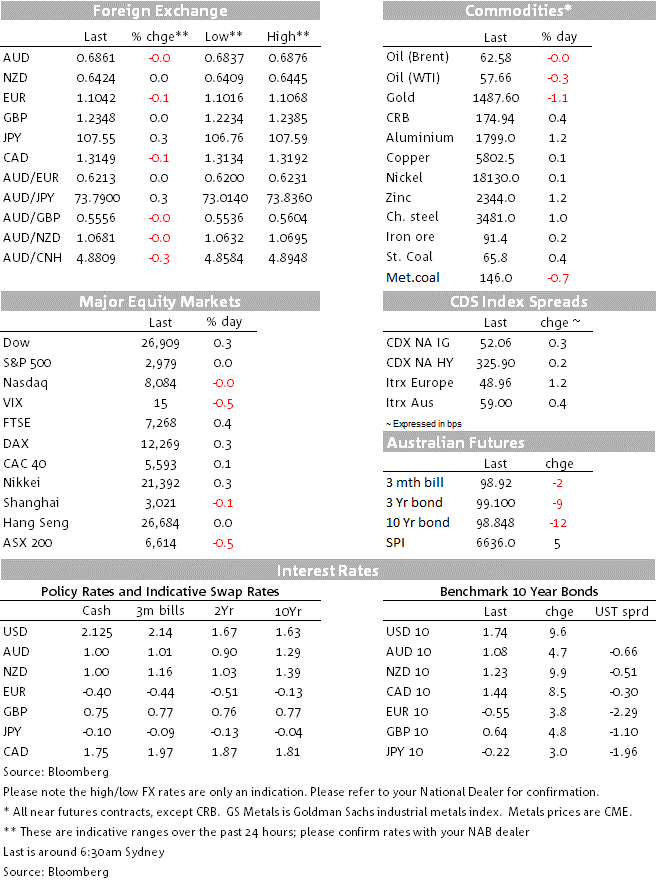

The move higher in core global bond yields has been the big news overnight as the market prepares for the ECB tomorrow. Meanwhile the hour of power has yet again come to the US equity market rescue, leaving main US equity indices unchanged for the day, after opening sharply lower. Moves in currencies have been relatively subdued with JPY weakness attributed to higher UST yields while NOK is the big underperformer, not helped by a sharp decline in oil prices following news that hawk US national security adviser, John Bolton, was not longer needed at the White House.

The repricing in core global bond yields has continued overnight with 10y Bunds and UST yields closing 3.6bps and 9.5bps (respectively) higher on the day. In August, 10y UST yields fell just over 50bps while Bunds declined around 26bps, but now in the past 4 trading days 10y UST yields have climbed 25bps to 1.742% while 10y Bunds are 12.7bps up to -0.547%.

The increased in US-China trade tensions over the past month alongside a downgrade to the global growth outlook and an increase in expectations of central bank easing all contributed the rally in bonds during August and early September. Now with the ECB meeting just around the corner it seem that the bond market investors are not willing to take chances, cashing in ahead of the ECB and Fed next week.

To some extent the repricing makes some sense given that after ECB Rehn hinted at the potential of a big bazooka around mid-August, ECB hawks including Weidmann, Knot, Nowotny, Lautenschlaeger, Villeroy, Muller and Holzman all came out housing down the need to for sizeable stimulus, arguing in particular against a return to QE. The idea of no QE was yet again reinforced overnight with a new sourced report from MNI saying that it was possible the ECB could announce a delayed start to QE, or that a resumption of the programme could be made conditional on further weakness in the economy. While the article said it was probably just a matter of time before the ECB restarted its QE programme, the market is clearly not taking any chance.

Another contributing factor has been the confirmation of no major German fiscal stimulus, after some suggestions of the potential for an increase in off-balance sheet expenditure measures, Finance minister Olaf Scholz maintained that Germany will have a balanced stimulatory budget next year ( oxymoron example?) that will help the nation cope with “great challenges” including trade disputes, without increasing the nation’s debt load. He said it would be an expansionary budget which would include a great deal of investment. Overall the comments are disappointing for markets hoping for some debt-financed or ring-fenced fiscal spending. For now, there is nothing to suggest Germany will go down this roads, unless and until it faces a real crisis.

So to conclude, we are now on the final countdown to the ECB meeting, the stakes are pretty high and while ECB President Draghi has form in delivering big surprises, this time it could be different given that the US led trade global growth slowdown is set to be a grind with no certainty as to when it might end. If the ECB tomorrow delivers with a dovish package of measures, including QE, the news should help contain the recent bond market sell-off, but if it disappoints, the bond market sell-off is at risk of extending.

US equities opened the session sharply lower, probably not helped by soft data releases. The JOLTS for July disappointed falling to 7.22m, from 7.25m in June and the NFIB index of activity and sentiment at small firms fell to 103.1 from 104.7, below the consensus of 103.5, and a five-month low. According to NFIB President Duggan, “In spite of the success we continue to see on Main Street, the manic predictions of recession are having a psychological effect and creating uncertainty for small business owners throughout the country” Even so, she said, “Small business owners continue to invest, grow, and hire at historically high levels, and we see no indication of a coming recession.”

In the end after falling close to 1% at the open, main US equity indices have closed the day little changed (S&P 500 0.03%m Dow +0.28% and NASDAQ -0.04%). Energy and industrial sectors gained over 1% while IT (-0.49%), Consumer Staples (-0.61%) and Real Estate (-1.37%) werethe underperformers.

Moving on to FX, the USD is a tad higher in index terms with DXY +0.1% to 98.39 and BBDXY +0.05% to 1208.76. A look at the G10 leader board shows the CAD +0.14% ( now at 1.3149 ) at the top with the Loonie not showing any ill effect from the close to 2% decline in oil prices following news that hawk US national security adviser, John Bolton, were not longer needed at the White House. Bolton’s departure has interpreted as a potential ease in US led geopolitical tensions.

USD/JPY is another big mover with the pair following the move higher in UST yields, courtesy of the BoJ yield curve control policy. Reuters overnight reported that according to some BoJ sources, “The pickup in global growth is taking longer than expected, which could affect Japan’s output gap and hurt domestic demand. If risks to Japan’s economy are deemed too high, there’s a chance the BOJ may act.”. So depending on how aggressive the EBC (12th) and FED (17/18th) are, then there is chance the BoJ (18/19th ) may follow, but we think this is a low risk. Last week Governor Kuroda gave an interview noting further stimulus was an option, but then added that circumstances have not worsened enough to merit such steps at this point.

The NZD and AUD are similarly little changed over the past 24 hours amid relatively tight trading ranges. The NZD is currently 0.6425 while the AUD is at 0.6862. There wasn’t much market reaction to either NZ or Australian data released yesterday. In NZ, electronic transactions (ECT) data revealed an bounce back in spending in August (1.3% in value terms) after several months of subdued results. In Australia, business conditions in the NAB survey deteriorated further in August, falling from 3pts (revised up from 2pts) to 1pt, the lowest level since September 2014.

On the NAB survey our economists noted the report suggests that momentum in the business sector continues to weaken, with both confidence and conditions well below the levels seen in 2018 – and is in line with the weak outcome for the private sector in the Q2 national accounts. NAB is now reviewing the outlook for interest rates which will be released alongside today’s updated set of forecasts.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.