Price growth edges lower despite reasonable economy

Insight

The Euro and European bond yields took a blow today as the European Central Bank failed to commit to a timetable for the ending of quantitative easing.

https://soundcloud.com/user-291029717/draghi-drags-it-out-again-gdp-friday

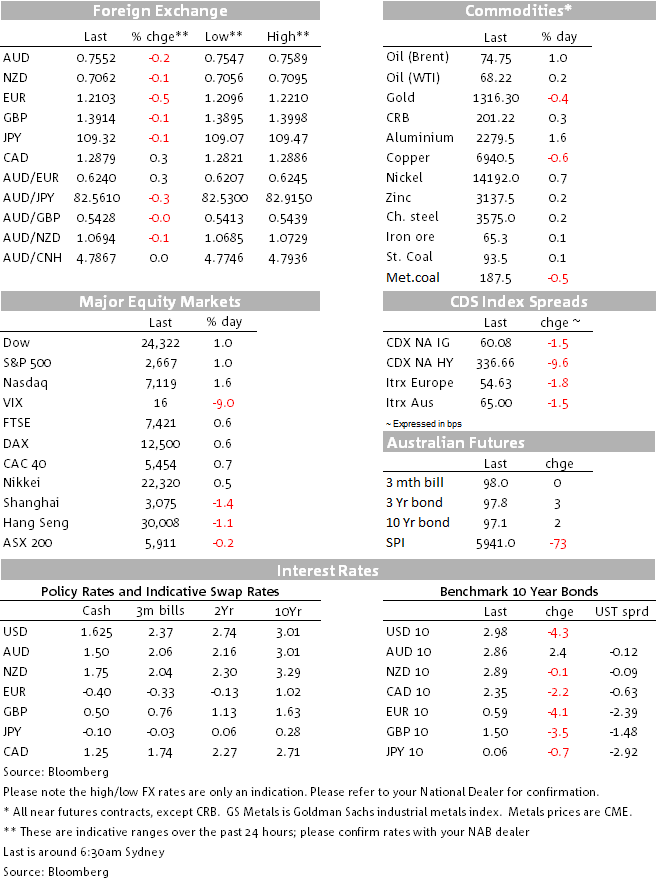

The week’s main event, ECB president Draghi post-meeting press conference, has come and gone leaving EUR/USD the best part of a cent lower, but it’s been a largely Euro-centric affair with limited contagion to other G10 currencies versus the US dollar, bar the Swiss Franc. AUD/USD orbits 0.7550. The Swedish krone is the standout loser of the past 24 hours after the Riksbank lowered its anticipated rates track. It’s been a good session for US stocks, largely earnings-driven but perhaps aided too by the slippage in 10 year Treasury yields to back below 3% (2.98% now).

As Gavin Friend in London notes in his post-ECB commentary, the ECB conveyed no sense of alarm or panic on the recent softening economic data and activity that is currently unfolding. In the post-meeting statement, Mr Draghi put on a brave face, insisting that the underlying strength of the economy continues to support its confidence that inflation will converge towards its mandated aim. He said, “The bottom line of this discussion is in my view, it’s basically caution in reading these developments, caution tempered by an unchanged confidence in the convergence of inflation to our inflation aim.”

EUR/USD initially rallied slightly at the start of the press conference, but then fell away as it progressed. As Gavin notes, this was as it became evident that what we were hearing from the President was not an all-clear and that further assessment is necessary before the ECB will decide if this has policy implications – such as delaying ending its bond purchases into early 2019. Indeed, later in the session a Bloomberg source story ran stating that Draghi faced down a request from the (perennially hawkish) Austrian central bank Governing Council member Ewald Nowotny that the future path of monetary policy be discussed. Lows of the session on EUR/USD just below 1.2100 (new 3-month lows) came soon after the story hit the wires.

EUR and CHF weakness has lifted the DXY dollar index further above 91.0 (91.58 now). Looking at the charts suggests that while DXY can move higher still, it will find resistance near 92.00 (the early January breakdown level) and which is also the 200 day moving average. If so, this might spare AUD/USD a test of the 0.75 level (and which is still out year-end target, albeit we need to acknowledge that some time is now likely to be spent sub-0.75 in the context of what we expect will eventually prove to be an unsustained USD rally).

Outside of FX, it’s been a very good night for US stocks, the S&P closing up just over 1% higher and the NASDAQ by 1.6%. Facebook jumped 10% after reporting its earnings and latest user-stats after the close yesterday. Advanced Micro Devices (AMD) jumped over 12% after reporting its earnings prior to the market open. Intel has just reported after the market close and exceeded its highest street estimate on earnings (87 cents versus a range of 70 to 76) with revenue more than $1 billion higher than expect at $16.1bn and improved forward guidance. This will support the market at Friday’s open.

In bonds, 10 year US treasuries have struggled to hold yesterday’s break above 3%, down 4.5bps to 2.98% now while 2 year yields are down just 0.4%. Thus the fledging curve re-steepening theme (and which looks to have been supportive of the USD) has suffered a set-back.

Commodities see oil adding back another 25 cents or so, after Brent crude added 50 cents yesterday following French President’s Macron’s prediction that US President Trump would pull the US out of the 2015 Iran nuclear deal which saw sanctions lifted and Iran pump one million barrels a day more oil than when the sanctions were in place. Exchange traded metals are mixed while iron ore is virtually unchanged on 24 hours ago at $65.29.

US data has been mixed, but looks to have left expectations for tonight’s first estimate of Q1 GDP little changed, centred on 2%. The advance report on good trade saw a much reduced deficit of $68.0bn down from $75.9bn in February, with imports slumping following the earlier post-Hurricane surge as inventories were rebuilt. This adds about 0.4% to Q1 GDP estimates according to the Atlanta Fed’s updated ‘GDPNow’ estimate, but fully offset by weakness in capital good shipments in the durable goods order report and a fall in retail inventories of 0.4%. They are still at 2%. Overall durable goods orders rose a better than expected 2.6% (1.6% est.) but ex the volatile defence and aircraft categories, they fell by 0.1% against an expected rise of 0.5%

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.