Price growth edges lower despite reasonable economy

Insight

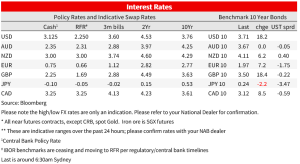

BoE, SNB and Norges Bank follow the Fed’s +75bps with 50bps, 75bps, 50bps respectively

UK: Bank of England Bank Rate (%), Sep: 2.25 (+0.5%) vs. 2.25 exp.

US: Initial jobless claims 213k vs. 217 exp. from revised 208k

EZ: Consumer confidence, Sep: -28.8 from -25.0 vs. -25.5 exp.

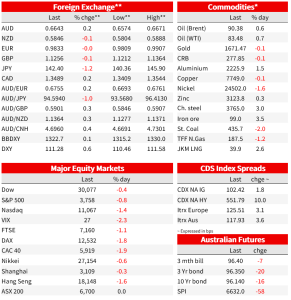

Another wild 24 hours with FX and bond market volatility firmly to the fore, no more so than in all things JPY after MoF ordered FX intervention for the first time since 1998, following USD/JPY making new highs above Y145 post a studiously unchanged BoJ, and 10-year Treasuries where yields are 17bps higher at 3.70% having fallen slightly in the immediate aftermath of Wednesday’s FOMC meeting conclusion.

Except for the Swedish Riksbank earlier in the week (+100bps) all this week’s central bank meetings have concluded with policy rate changes that conformed to pre-meeting consensus expectations, the Fed and SNB each by 75bps, the BoE and Norges Bank by 50bps apiece . This also included the Bank of Japan, but where their resolutely unchanged stance out of the meeting, including reference to rate being held at or below current levesl and a suggestion in the post-meeting press conference from Governor Kuroda that the stance could remain “even for as long as two or three years” in principle, was enough to see USD/JPY push on to a new post-August 1998 high of 145.90.

Then came BoJ intervention – that would have been a MoF not BoJ initiative – which drove the pair down to a low of Y140.36. An impressive intra-day move to be sure, but the fact is that USD/JPY is currently only 1.25% lower than where it was 24 hours earlier. Given the now even starker contrast between the BoJ’s policy stance and central banks everywhere else in the world and the fact intervention is working completely against the grain of Japan’s domestic monetary policy stance, MoF will need to be in this intervention game for the long haul and in size if it is to have much hope of arresting JPY weakness in an ongoing strong USD environment. And short of resurrecting some sort of SNB style currency peg as the latter did with EUR/CHF (and which ultimately failed, even though the SNB was selling not buying its own currency) the law of diminishing returns will surely set in on BoJ intervention before too long.

The back- up in longer-dated Treasury yields may well owe something to the BoJ’s actions, in so far as the world’s largest foreign holder of Treasuries will be condemned to sell some of them to furnish the US dollars required for intervention. There is also a hint in overnight US rates market price action that the market is starting to believe the Fed might not be cutting rates in the back end of 2023, or at least not by as much as had been the case into and immediately out of the FOMC meeting. US money markets now have the end -2023 fund rate priced some 35bps below an assumed Q2 2023 peak, in from 40bps the day before.

Such a (so far minor) reassessment could have further to run if evidence of US economic weakness and in particular a weakening labour market, remains notable by its absence. Certainly, the latest weekly US jobless claims data provided no such evidence, claims up slightly to a still very low 213k but off a downward revised 208k the week before.

The BoE hiked Bank Rate by 50bps to 2.25%, as expected by most economists, although the market was better priced for a larger 75bps move, hence a knee jerk negative GBP reaction to the news. It was a split vote on the MPC, with 5 voting for 50bps, 3 for 75bps and 1 for 25bps. While a full set of forecasts wasn’t produced, the Bank noted that the government’s new energy price guarantee meant that the peak in the CPI will now be just under 11%, down from the 13% rate projected in August. There was only a small tweak to the Bank’s forward policy guidance, with the committee leaving in the comment that it “will respond forcefully, as necessary”, should the outlook suggest more persistent inflationary pressures, including from stronger demand. On QT, the Bank confirmed that it would actively sell UK bonds over the next 12 months (about £10b per quarter) and this process will begin shortly.

Looking across currency markets , it is very unusual to see the two traditional haven currencies – JPY and CHF (of late usurped by the USD of course) sitting at opposite ends of the G10 spectrum (JPY more than 1% stronger, CHF more than 1% weaker). The latter was a move that came after the SNB’s +75bps rates decision an where it very much looked as though the SNB was intervening immediately out of the decision to check further, unwanted, EUR/CHF depreciation and after the pair had fallen quite sharply in the two days leading up to the SNB meeting. There had also been some thoughts the SNB might deliver a 100bps hike.

Prior to the BoJ intervention to drive down USD/JPY and which had a mechanically large impact on the DXY given its 13.6% weight, the USD had made a new cycle high of 111.80. It is currently around 0.5% back from that. EUR/USD remains the much bigger influence on the index of course, the pair making a new low of 0.9809 overnight. AUD and NZD found some relief for USD strength when the BoJ intervention came, but only after AUD/USD had hit a new 2+ year low of 0.6574 and NZD 0.5804.

Finally, US equity markets fell away in the last hour to reverse a fleeting early-afternoon rally, the S&P500 finishing in New York down 0.8% and the more interest rate sensitive NASDAQ down 1.4%. As was the case on Wednesday, Consumer Discretionary was the weakest performing S&P sub-sector, down 2.2%.

NAB Markets Research Disclaimer

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.