Price growth edges lower despite reasonable economy

Insight

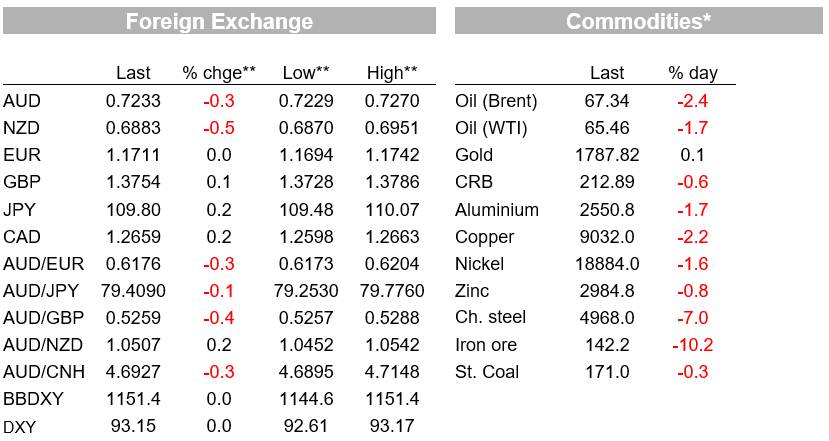

Following a fair amount of volatility in the immediate wake of the FOMC Minutes US equities are lower, bond yields and the USD are lower, the latter allowing the AUD some relief after posting a new year-to-date low of 0.7229 in the run up to the Minutes, but the gains are already proving hard to hold.

https://soundcloud.com/user-291029717/central-banks-holding-back?in=user-291029717/sets/the-morning-call

Following a fair amount of volatility in the immediate wake of the FOMC Minutes US equities are lower, bond yield are lower and so is the USD, the latter allowing the AUD some relief after posting a new year-to-date low of 0.7229 in the run up to the Minutes, but the gains are already proving hard to hold.

The key sentence in the Minutes of the Fed’s July 28 meeting is that “….it could be appropriate to start reducing the pace of asset purchases this year because they saw the Committee’s “substantial further progress” criterion as satisfied with respect to the price-stability goal and as close to being satisfied with respect to the maximum employment goal. “Various” FOMC members see grounds for tapering in coming months, versus “several” thinking it more likely early next year.

This leaves the market reasonably well set up for a decision on the start date of tapering being made as early as next month’s (September 21-22) meeting, to commence before the end of the year (possibly to be ratified and begun soon after the subsequent (Nov-2-3) meeting?). Obviously, contingent on a third successive good employment report being published on 3 September.

The Fed once again endeavours to draw a distinction between tapering and rates lift off, viz: ” …participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases and remarked that the timing of those actions would depend on the course of the economy.”

As for the initial pace of tapering as and when the Fed deems they are ready to start, one sentence of note is that “an earlier start to tapering could be accompanied by more gradual reductions in the purchase pace and that such a combination could mitigate the risk of an excessive tightening in financial conditions in response to a tapering announcement.” This reads like a sop to the ‘doves’ on the committee who favour a 2022 taper start date from ‘hawks’ who want to get a hurry-up (though evidently not Messrs Bullard or Kaplan, who earlier this week set their stalls out specifying a desire for an initial taper pace of $30bn per month (Bullard) or $15bn (Kaplan).

On the question of whether the Fed might reduce its MBS purchases more quickly than Treasuries, the Minutes note that “most” members want to reduce Treasury and MBS purchases “proportionally in order to end both sets of purchases at the same time”, with only “several” wanting to reduce MBS purchases more quickly. In this regard, the latest set of US housing market indicators overnight, showing a bigger than expected 7% drop in Housing Starts in July and a meagre 2.6% bounce in Building Permits after a 5.3% June drop, surely adds weight to the view that the notion of MBS purchases pouring petrol on an already inflamed housing market is last year’s story.

Other economic news overnight included stronger than expected Canadian inflation data where ethe average of the three core CPI measures lifted to 2.5% from 2.2% (2.2% expected) while in the UK headline and core CPI readings both fell 0.2% short of expectations at 2.0% and 1.8% respectively.

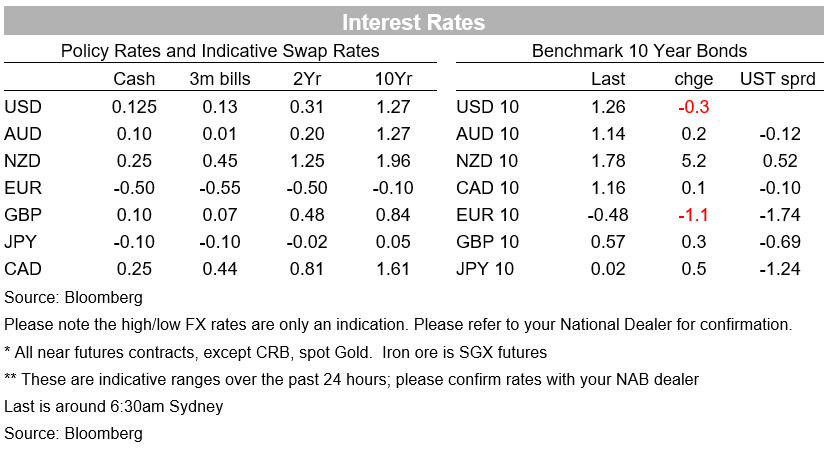

Market wise, US bond yields were rising into the FOMC Minutes, seemingly in anticipation of a potential ‘hawkish’ surprise (high of almost 1.30% at 10-years) only to fall back to 1.26% post Minutes. The 2-year note lifted to 0.225% from 0.21% but is currently back at 0.215%. Earlier, EU bond yields were mostly 1-2bps lower while gilts were little changed notwithstanding the downside CPI surprises.

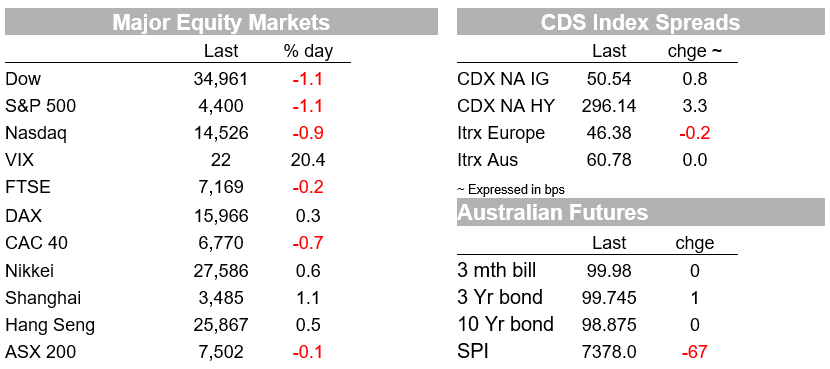

US equities meanwhile traded sideways into the Minutes at levels little changed from Tuesday’s close, only to dip out of the Minutes and then fall away quite sharply in the last ‘hour of power’ with the S&P 500 finishing the day 1.1% lower. Newswires seem happy to attribute this to the Fed’s signalling that tapering is near, though we would also note that the energy sector (-2.4%) is the weakest performing sub-sector of the S&P and that oil prices, already under pressure earlier in the afternoon, lost another dollar post Minutes to end the NY day down $3. The NASDAQ ends the NY day -0.9%, after what was a mixed day for European stocks (Eurostoxx 50 -0.17%).

In currencies, after the quite extreme volatility in the NZD out of the RBNZ’s ‘hawkish hold’ yesterday and which also impacted the AUD, both currencies are lower overnight, NZD a net half a percent own on Wednesday’s close and the AUD a quarter of a percent. The later has made a new year to date low of 0.7229 in from of the Fed Minutes, and though bouncing out of the Minutes as the USD fell back, has struggled to hold the gain and is currently back down to 0.7233.

Finally on all things NZ, RBNZ Governor Adrian Orr has been on local radio this morning saying the OCR would likely have been raised yesterday before the Covid-19 lockdown put a stop to that, but that with the RBNZ now meeting its targets on inflation and employment, it can’t hold back much longer.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.