Price growth edges lower despite reasonable economy

Insight

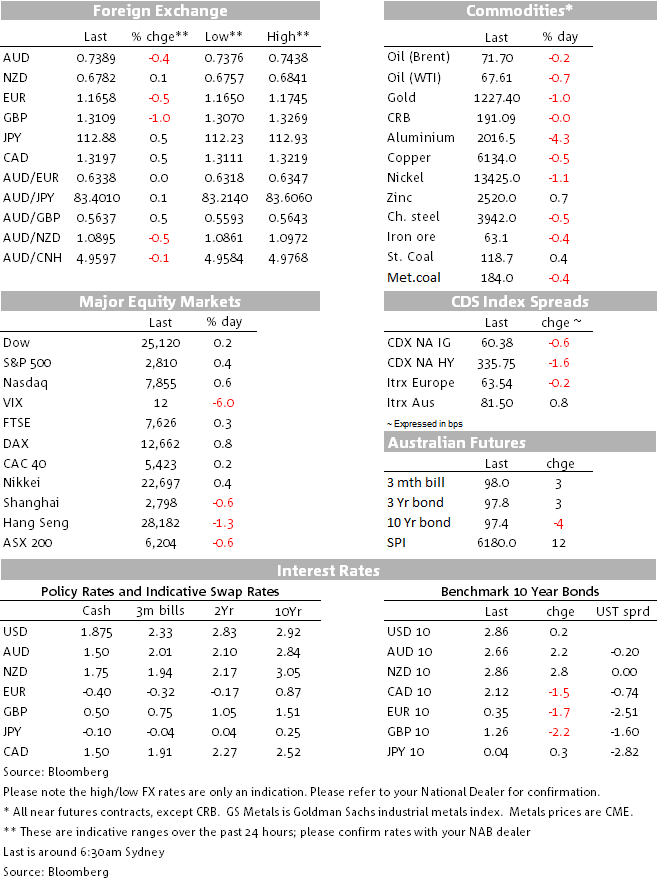

The move higher in front end yields boosted the USD, although the greenback was already on the ascendency early in the overnight sessions.

https://soundcloud.com/user-291029717/powell-strikes-a-cautious-note-carney-warns-europe

At his semi-annual testimony before the Senate, Fed Chair Powell reiterated the Fed’s upbeat assessment of the US economy, noting risks to the outlook remain roughly balanced and that for now the best way forward is to keep lifting rates gradually. On trade, a pragmatic Powell said that it was too soon to say how trade policy would influence the Fed’s thinking. So the key take away is that trade policy has not yet affected the Fed’s intentions for further gradual hikes. The Fed remains data dependent and the inclusion of the phrase “for now” provides the Bank with some flexibility if it needs to alter the interest rate path ahead.

US equities liked Powell’s upbeat US economic assessment and lack of imminent concerns over trade policy. Reaction in US rates triggered a flattening of the US Treasury curve led by a rise in front end yields and although the USD was already rising ahead of Powell’s testimony, the move higher in shorter dated UST yields was an additional boost for the greenback. NZD retains its gains from yesterday’s higher than expected core inflation, despite a mixed dairy auction overnight and GBP underperform amid ongoing Brexit political uncertainty.

The Nasdaq index has led the gains in equities overnight, climbing above its previous closing record high, closing the day 0.63% higher. So a rebound in technology shares and upbeat Fed Chair Powell testimony has helped risk sentiment overnight. Netflix shares retraced about two third of their opening drop ( -4.3%) as investors looked past disappointing quarterly earnings re-focusing on long-term growth. Meanwhile the Stoxx Europe 600 index added 0.2% and late yesterday the Japan’s Nikkei closed up 0.4%.

Although market expectations of Fed tightening didn’t change much after Powell’s comments with the market currently pricing just over a 90% chance of a September rate rise and about 3 hikes to the end of 2019 (versus 5 hikes denoted by the Fed dots), shorter dated US treasury yields continued their slow ascendency with the 2y tenor climbing another 1.5bps to 2.613%. Meanwhile 10y UTS yields were little changed at 2.86%, flattening the 2y10y curve to 24.8bps– its flattest level since 2007.

The move higher in front end yields boosted the USD, although the greenback was already on the ascendency early in the overnight sessions. The DXY index more than reverses the minor losses from the previous two days and now it is toying again with a move back above 95.

GBP has been the weakest currency overnight as politics continues to overshadow economic data (see below). The UK Government managed to narrowly avoid defeat on an amendment to the Trade bill that would have sought to keep the UK in the Customs Union if the Government couldn’t agree on frictionless trade with the EU by January 2019. If the amendment were accepted (and the Government defeated), there was speculation there would be a leadership challenge on Theresa May and possibly a vote of no confidence from Labour. GBP fell to as low as 1.3070 ahead of the vote, but has since recovered slightly to 1.315 after the amendment was defeated. So in spite of a positive outcome for the government, political uncertainty remains a massive headwind for the pound, overnight the FT reported that some EU diplomats are beginning to debate whether it is worth negotiating with PM May if she cannot hold her party together.

The NZD is slightly higher than this point yesterday at 0.6785 but it is the strongest performing currency in the G10. Headline CPI data released yesterday morning showed a 0.4% increase in Q2, slightly below the median expectation of 0.5%, but allaying some market fears of a very weak print. But the big surprise was an unexpected increase in the RBNZ’s Sectoral Factor Model of underlying inflation which was released later in the day. The Sectoral Factor Model showed an annual underlying inflation rate of 1.7% in Q2, higher than Q1’s 1.5% (subsequently revised to 1.6%). After revisions, the Sectoral Factor Model now shows an increase from 1.4% in Q3 last year to 1.7% currently – still below target, but now giving the impression that it is certainly moving in the right direction. A mixed dairy auction had little impact on the kiwi overnight The GDT Price Index fell 1.7%, within the expected range albeit toward the better end, but the details were extremely mixed with fat prices falling heavily while powder prices rose.

AUD is back below the 74c mark (-0.42%) and is currently trading at 0.7389. It has been a soft night for commodities (more below) and the divergence between emerging markets equities vs Developed market equities continues to be a thorn on the side for the AUD.

Oil prices had a calm and steady session overnight after a big decline on Monday (Brent -0.2%), but looking at the whole commodity complex the picture remains cloudy. Zinc had a good night up 1.54% , but the rest of the complex had a down day, copper lost another 0.72%, aluminium gave up 1.12% and iron ore closed -0.40%. Global growth concerns amid rising trade tension are seemingly the biggest drag on commodities at the moment.

UK: Unemployment rate, May: 4.2% vs 4.2% exp.

UK: Average weekly earnings ex bonuses (3m/3m), May: 2.7% vs 2.7% exp.

NZ: Global Dairy Trade – avg. winning price: $3,222 vs $3,232 prev.

NZ: Global Dairy Trade – whole-milk powder: $2,973 vs $2,905 prev

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.