Price growth edges lower despite reasonable economy

Insight

COVID19 cases continue to rise in Europe, with numbers in the UK and France now well above the first wave.

https://soundcloud.com/user-291029717/courting-support-ahead-of-election-debates?in=user-291029717/sets/the-morning-call

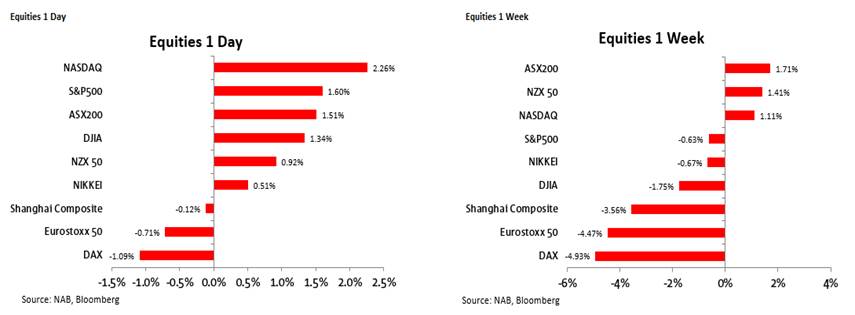

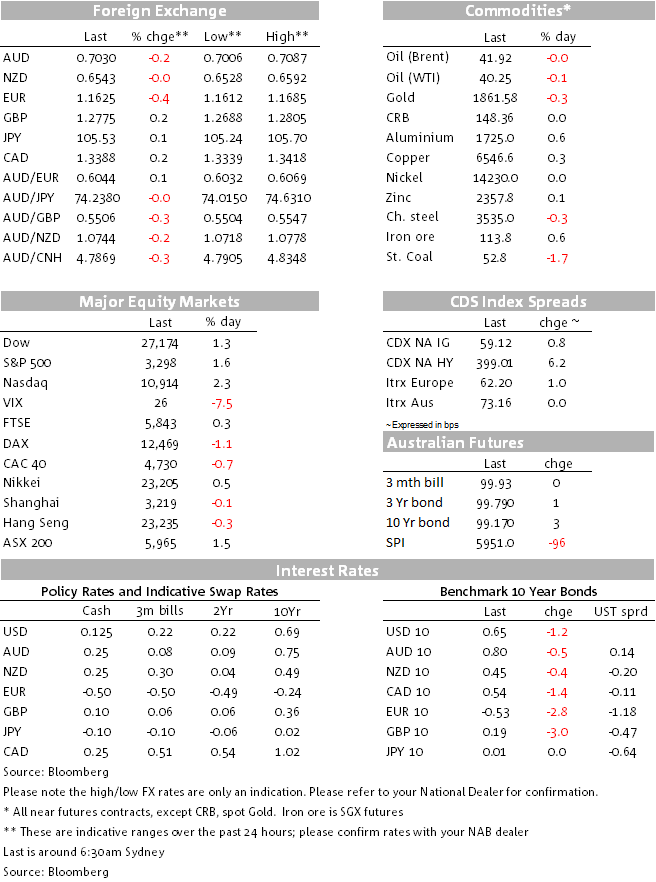

It was a relativity quiet end to last week, but a good day for the NASDAQ Friday, +2.3% – big-tech now somewhat laughingly referred to as ‘defensive’ given the relative immunity of the sector (or benefits) to adverse covid-19 developments – pushing the index into positive territory for the week (+1.1%). A 1.6% gain for the S&P still made for a fourth consecutive down week (-0.6%) and leaves the index -5.8% month to date with three trading days to go until month/quarter end. The latter could be an interesting one for currencies from a rebalancing perspective depending on how stocks go between now and Wednesday.

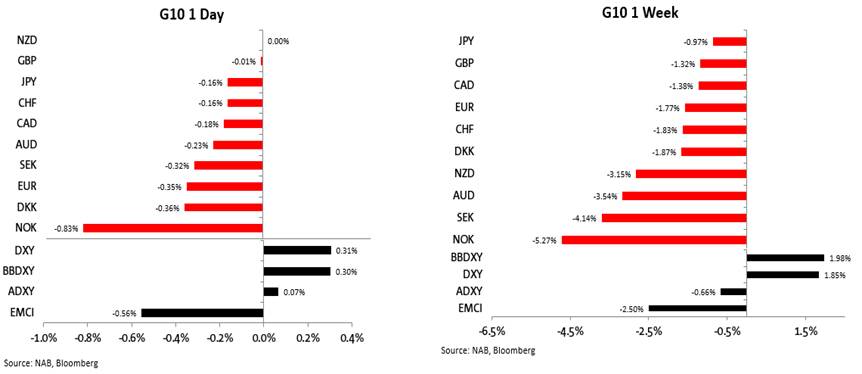

Despite being a positive US session for risk assets, in FX the USD still eked out additional gains (+0.3% in DXY and BBDXY terms) with AUD/USD down another 0.23% to a low of 0.7006 before lifting to 0.7030 by the NY close. AUD is down 3.5% on the week, losses within the G10 spectrum only surpassed by the Swedish and Norwegian Crowns. As well as the impact of broad based USD strength, of special relevance to AUD (and to only slightly lesser extent the NZD) is the across-the board weakness in EM currencies, not so much in Asia but led by the likes of MXN, BRL and other Latam currencies, the South African Rand, Russian Rouble and Turkish Lire. Here, we often find that the AUD correlates better with a global EM FX index than with one linked just to Asian EM, despite the strength of trade ties with the latter. As per the chart below, the global EMCI was off 2.5% last week versus just -0.66% for the (Asian) ADXY:

Partly due to USD strength but perhaps too the demand-side implications of virus trends in the US, Europe and elsewhere (e.g. New York reported more than 1,000 cases on Saturday for the first time June 5) it was a poor week for commodities, ranging from -2% for WTI crude oil to -4% for the LMEX base metals index to -4.9% for gold.

Global government bonds markets remain extremely well supported, US 10-year Treasuries off 1bps Friday to 0.65% and the German Bund -3bps to -0.53%.

In economic news, US Durable Goods Orders disappointed expectations in headline terms (+0.4% vs. +1.5% expected) but the less volatile capital goods ex-defence, ex-aircraft reading was better than expected at +1.8% (1.0%) and July was revised higher to 2.5% from 1.9%.

China August industrial profits were reported Saturday up a healthy 19.1% versus 19.6% in July (back in March close to the peak of China’s covid-19 lockdowns, they were -35% y/y).

on Saturday evening in Washington Amy Coney Barrett was confirmed as President Trump’s new Supreme Court pick, the third of his Presidency. Confirmation in coming weeks (highly likely) will install a 6-3 conservative bent to the Court. Barrett’s nomination has immediately has taken on 3 November election significance. Both President Trump and Senate minority leader Chuck Schumer are claiming that her elevation to the Supreme Court could sound the death knell for the Affordable Care Act (Obamacare) in its current guise (in particular with respect to the current provisioning that compels insurers to take on people with pre-existing medical conditions). There is also the question of how the nomination of a mid-western Catholic conservatives will play with voters in some of the so called Rust Belt and Sun Belt ‘battleground’ states where Joe Biden currently has his nose in front of Trump.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.