Price growth edges lower despite reasonable economy

Insight

The markets have retreated somewhat from yesterday’s tumultuous response to uncertainty over who will govern Italy, and their stance on the Euro and EU membership.

https://soundcloud.com/user-291029717/did-parmageddon-go-too-far-inflation-next-to-watch-for

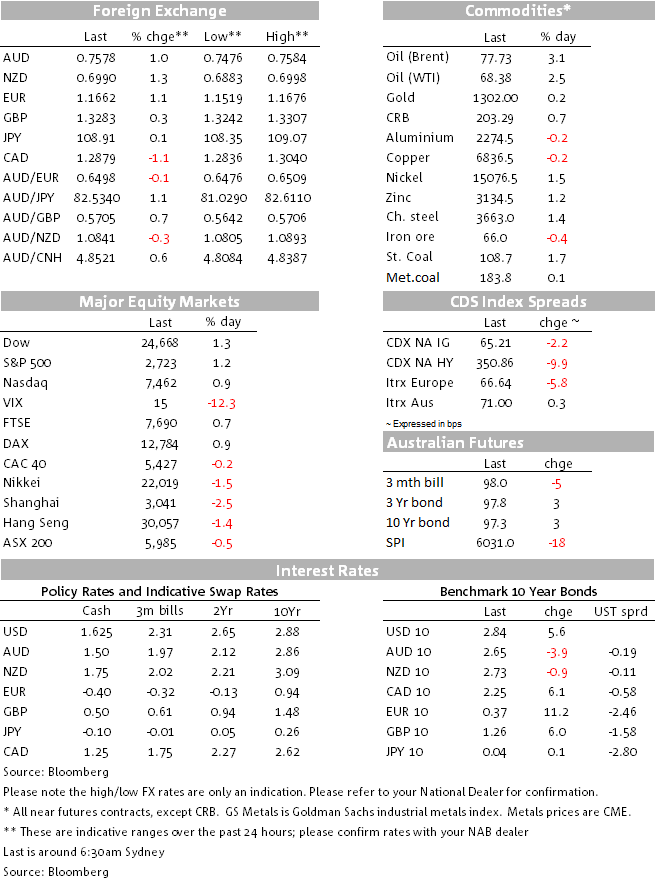

Global markets moves on Wednesday aren’t quite the mirror image of Tuesday, but many of them are doing a passable impression. In FX for example, the Swedish Krone lost over 1.5% on Tuesday in the midst of the Italian bond market carnage, and today it is up 1.8%. Italian bond yields have retraced almost half of Tuesday’s spike at the short end (and more than half at ten years, aided by a respectable – in the circumstances – sale of €5.6bn worth of bonds). US Treasury and German 10-year bond yields are smartly higher (~6bps and 10bps respectively) while the S&P has just closed up by 1.3% for its biggest one day gain since May 4th. AUD/USD, having spent time back below 0.75 yesterday morning, has made an overnight high just above 0.7580.

Relieving Wednesday’s acute tension in Italy and which had some immediate global contagion effects via various financial linkages (or fears thereof) have been reports that the Italian President will allow Five Star and the League to have another attempt to form a government, with Five Star leader Di Maio saying he was willing to propose a choice of new finance minister. The League, which has seen large gains in opinion polls since the election, seems more intent on going back to new elections, but the current indications are that this is going to be the case, it won’t be as early July and which, for now, is being viewed as a positive not a negative. Also helpful has been comment from Five Star leader Di Maio saying that the two anti-establishment parties never sought an exit from the euro and that Five Star was willing to cooperate with the President (having earlier been calling for his impeachment following the rejection of the proposed candidate for finance minister).

EUR/USD has risen from 1.1525 to as high as 1.1676, partly on the less fraught Italian situation but also as inflation in Spain and Germany comes in above forecasts. Spain posted May preliminary HICP of +0.9% m/m for 2.1% y/y (vs 1.7% consensus). Germany printed 2.2% in both headline and HICP terms against the consensus of 1.8% prior to the staggered release of the various state numbers. This then poses clear upside risks for today’s pan-Eurozone HICP estimate where the earlier consensus was at 1.6% from 1.2%. EZ confidence data were also generally stronger than expected and while off their late 2017 peaks, are holding up better than the recent PMI activity data.

If the incoming inflation data does embolden the ECB to give some signalling with regards to the fate of the QE bond buying programme as early as June 14th (the next Governing Council meeting) then the Bank of Canada has already moved a step in front of it, shifting its language following the conclusion of last night’s policy meeting to put market back firmly on the scent of a next rate rise on July 11th. The market implied probability of July meeting has jumped from below 50% to above 75% after the BoC dropped the ‘cautious’ adjective previously in front of ‘gradual’ in terms of its approach to future rate rises. It also dropped reference to higher rates being needed ‘over time’. Markets had previously been given to belief that the BoC was parked on hold pending a successful resolution of NAFTA negotiations and evidence that business confidence was subsequently improving. Now, they seem confident that business confidence and conditions are sufficiently robust not to need to wait much longer. At the same time, Canadian PM Trudeau has been out saying he would rather no deal than a bad deal with respect to NAFTA.

Canada’s evident intent to proceed with policy tightening puts a spotlight on who else might be getting close to initiating a tightening cycle of their own Here, the OECD was out last night suggesting the RBA would be moving before the end of the year, citing the likelihood of wage rises and inflation both quickening by then. We were with them on this until a few weeks ago, but are no longer of the view that, in particular, unemployment will have fallen enough by late 2018 to bring about a rise in wages pressures sufficient to given the RBA confidence inflation is now set to come back toward the middle of the 2-3% target band as quickly as they would like. Latest polls of private economists’ expectations currently pencil in the first RBA move at mid-2019, as does NAB.

Other things to note overnight includes the resurrection of Sino-US trade tension following Trump’s latest backflip that saw him announce tariffs on $50bn worth of China imports after saying just a week ago tariffs were off the table for now. Wilbur Ross is still planning to be in China June 2-4th for the latest round of trade talks. Oil is back higher again (+$1.50-2.0) amid speculation that whatever agreement OPEC and Russia strikes on increased output next month, it will only be aimed at stabilising the market near here rather than driving prices appreciably lower.

US data out overnight has included the ADP employment report which at 178k verses the 190k consensus has some analyst knocking a bit off their picks for Friday’s non-farm payrolls; revised Q1 GDP at 2.2% versus the 2.3% prior estimate (with core PCE price index down to 2.3% from 2.5%); the advance US goods trade balance at -$68.2bn against the -$71bn consensus; and retail and wholesale inventories which came in flat versus +0.5% expected. The Atlanta Fed will be updating its ‘GDPNow’ estimate tonight (last at 4%)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.