Price growth edges lower despite reasonable economy

Insight

Will the results of the US mid-terms impact the focus of the Fed?

https://soundcloud.com/user-291029717/divided-they-stand-divided-the-dollar-falls

For once the polls were right! The Republicans kept control of the Senate, actually increasing their majority by three, but the Democrats rested control of the House back from the GOP. At his press conference, as well as claiming credit for the economy’s performance, President Trump struck something of a conciliatory political tone, saying that he is willing to work with the Dems to get policy through, though not if there is a blizzard of subpoenas threatening the President.

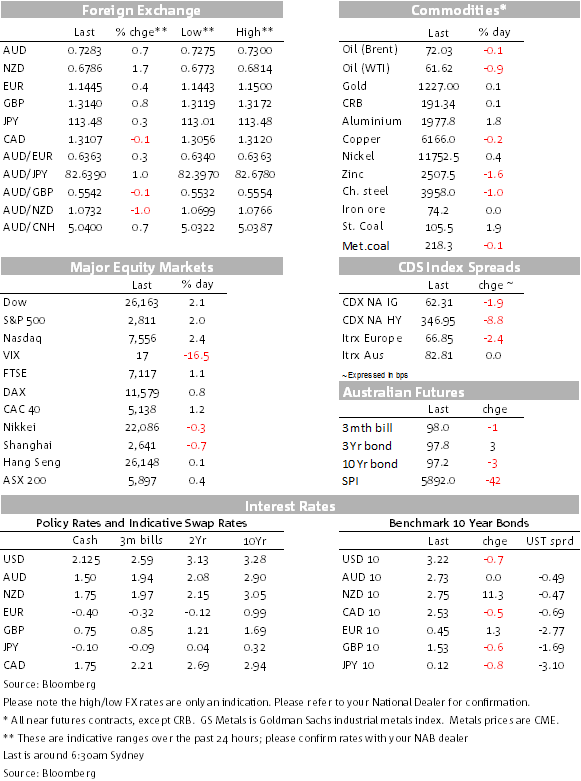

In Asia yesterday, the USD drifted lower, with risk currencies such as the AUD and the NZD doing better, Kiwi also having had the benefit from a large drop in the unemployment rate to below 4% and a large rise in employment, the best such figures since before the GFC. Overnight, European and US equity markets have rallied, the Eurostoxx 600 index up 1.06% and the main board US indexes up 2-2¼% in the last hour of trade, the Nasdaq doing the better. US bond yields are mixed, US 2s up but 10s down a basis point as we go to press.

With trade tensions to the fore over recent months and risk currencies in the spotlight, the US Mid-Terms were being seen through the prism of whether the outcome might embolden the President to go harder on trade or in effect if the elections would clip his wings. With the Democrats gaining control over the House, the latter scenario now might be a little more likely, including from his press conference, though both sides are unsurprisingly claiming victory as they might.

The USD drifted lower during the APAC session yesterday as the election results came in, but the moves were not large. At the end of the day, the President can still prosecute further changes on trade and a step up in the tariff rate to 25% is still on the cards to take effect from January 1 (together with the threat of potentially wider coverage of higher tariffs) unless some “deal” can be nutted out at the G20 in Argentina later this month.

The star performer though yesterday was the Kiwi on the back of the much stronger labour market report for the September quarter. While the surprise half a percent quarterly drop in the unemployment rate from 4.4% to 3.9% possibly overstated the improvement in the labour market on a full read through, including the accompanying more muted wages data, the NZD jumped higher, dragging the AUD along for the ride early in the APAC session yesterday. Both the NZD and the AUD are 0.3-0.4% higher than where they sat when we went home yesterday.

As expected, the RBNZ left rates on hold this morning at 1.75%. The NZD has been whippy since with the various pieces of the RBNZ’s statement offering something for everyone. As my colleague Stephen Toplis from BNZ has noted in his quick reaction piece, “The RBNZ has done its very best to keep market pricing unchanged and so far exceeded. There is no change in the cash rate and no meaningful change in the interest rate track. The Bank acknowledges upside and downside risks to growth and inflation projections but has dropped the up or down risk for the OCR. At the very margin this means the statement is slightly more hawkish than previously. The emphasis is on slightly”. There is a press conference to come at 10am AEDT.

Sterling also makes some net gains – including against the Euro – as markets prepare further for the probability/likelihood of a Brexit deal to be put before British Parliament as early as November 27. Markets are giving PM May wiggle room knowing she is pulling out all stops with that the clock ticking to get a deal ratified not only by the UK Parliament but the European Parliaments. The Irish border issue still needs to be sorted out, but rather than what has mostly this year been one disappointment after another, markets are now positioning for a deal. We think that Sterling could rise another 3-4% as news develops further in the days and weeks ahead, EUR/GBP at its lowest levels since mid-year, down 3.8% from late August highs.

There’s been little movement in bond yields, US short term yields a little higher as the FOMC approaches tomorrow morning, but long term yields drifting lower, perhaps with the knowledge of less likelihood of another round of US tax cuts, though additional infrastructure spending has bipartisan support, in principle. Remember too that there are budget continuing resolutions and debt ceilings yet to negotiate.

With the USD drifting lower, it wouldn’t have been surprising to see commodities push a little higher. In the event, oil is flat to lower, WTI leading with Brent little changed, gold up smalls, with base metals also mostly higher, copper unchanged while aluminium had a good session. Dalian iron ore and steel rebar futures ended a little higher yesterday, while steaming coal rose 1.88%.

It’s been an uneventful night for data reports. A little from left field and something worth keeping an eye on has been some further softness in the US mortgage demand as a consequence of rising mortgage rates. The 30 year mortgage rate is the highest since 2010 with the latest weekly US MBA mortgage (flow) index down another 4% for the week to November 2 to the lowest reading since December 14. While the US economy has been well and truly firing, the drag on the economy from dwelling investment evident over the past year or so seems likely to persist and likely build.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.