Price growth edges lower despite reasonable economy

Insight

As the President prepares to leave for the White House there’s still hope that a deal will be reached to pass version 2 of the Heroes Act, adding more stimulus to the US economy.

https://soundcloud.com/user-291029717/dont-be-afraid-of-covid?in=user-291029717/sets/the-morning-call

Going home, Without my burden, Going home, Behind the curtain, Going home, Without the costume, That I wore – Leonard Cohen

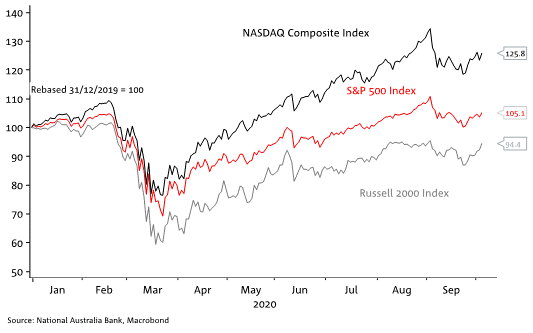

US stocks closing with gains of 1.8% for the S&P500, 2.3% for the NASDAQ and 2.8% for the smaller cap Russell 2000. The latter continues to tell a tale of improved confidence in a new fiscal support package that may be closer to The Democrats; $2.2bn bill passed last week, and of an undisputed Biden election victory on 3 November. Smaller firms are seen likely to benefit disproportionately from a new fiscal plan, and also potentially less affected than some of the big-cap sectors (including technology and health) from regulatory changes that will be more readily secured under a ‘blue wave’ scenario where the Democrats win back control of the Senate as well as holding the House. The Russell 2000 index is now less than 2% off its early September peaks, whereas the S&P500 is still more than 5% below. (see Chart of the Day below).

After the weekend NBC/WSJ polls, taken post last Tuesday’s TV debate but prior to Trump’s covid-19 diagnosis, showed Biden pulling 14 points clear of Trump on a national basis, overnight a Reuters/Ipsos poll gives Biden 10-point edge over Trump, 1 to 2 points higher than leads Biden posted over the past several weeks. The pollsters acknowledge though the increase in Biden’s lead is still within the poll’s precision limits of plus or minus 5 percentage points. The poll reveals that the majority of Americans think Trump could have avoided infection if he had taken the virus more seriously.

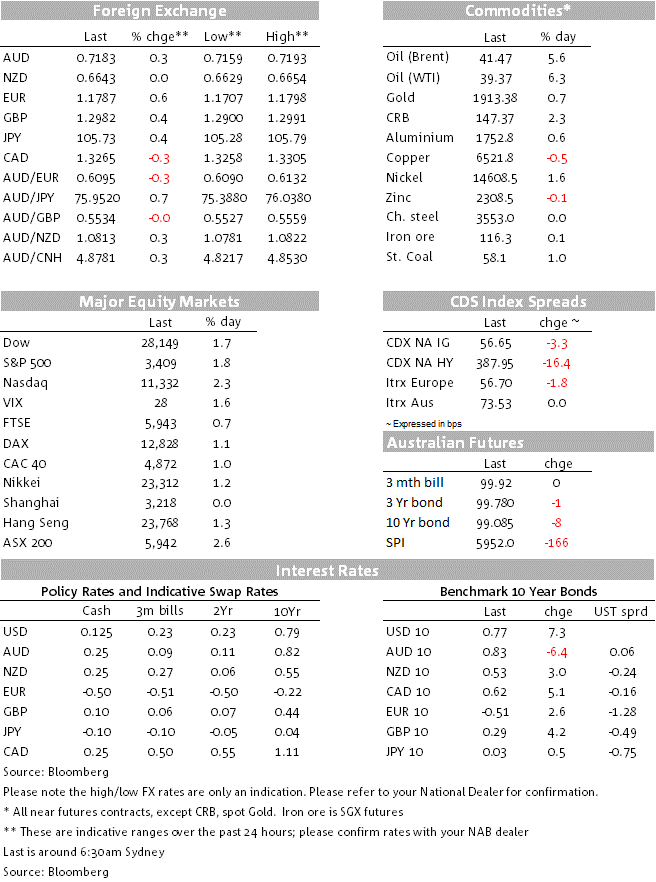

Something meaningful to say about bond markets for the first time in a while, with 10-year Treasuries rising by 6bps to 0.76% and up from a low of 0.65% soon after the news of Trump’s positive covid infection on Friday. Improved near term stimulus prospects and then potentially bigger deficits under a Biden Presidency that has the benefit of clean sweep, are behind the yield gains here, with spill-over to European markets where benchmark 10-year yields were up by 2-4bps on average. 10-year Australian bond futures show an implied yield rise of 4bps (to 91.5bps) since Friday.

USD/JPY has been one obvious beneficiary of the rise in US Treasury yields given its ultra-sensitivity to the spread over JGBs, up by 0.4% to Y105.75 and meaning the JPY is by far the weakest G10 currency so far this week. The USD is 0.4% lower on the DXY index and 0.45% in BBDXY terms, doubling the loss seen during the APAC time zone yesterday thanks to incremental gains for EUR and GBP. Optimism that a UK-EU trade deal can be struck in time has not been dented by the failure at the weekend to agree that talks are now at a stage where they can enter the so-called tunnel. This is despite UK PM Johnson at the weekend saying that the UK can “more than live with” a no-deal Brexit, and too comments from BoE MPC member Haskell that he stood ready to provide more stimulus, if needed, and his positive spin on negative rates, as a possible future policy tool. EUR gain were underway prior to the release of final Eurozone PMIs which showed some upward revisions to the flash services reading (e.g. Germany to 50.6 from 49.1) but news here certainly did the single currency any harm. AUD has held rather than extended the APAC session rally of about a quarter of a percent, currently 0.7185.

The US ISM services index (formerly the non-manufacturing index) unexpectedly rose to 57.8 in September from 56.9, with strong gains in new orders (+5.7pts to 61.5) and employment (+3.9pts to 51.8). There wasn’t much reaction to the data. In central bank talk, Chicago Fed President Evans told Bloomberg TV “I would be quite pleased if we could get core inflation up to 2.5% for a time”, adding that “2.5 is not even a large number.” The market is trying to work out how the Fed plans on operationalising its new ‘flexible average inflation targeting’ framework. Further clues may come from the minutes to the Fed’s September meeting, Powell’s speech tomorrow morning and New York Fed President William’s speech on the topic later in the week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.