Price growth edges lower despite reasonable economy

Insight

The Euro’s rise is based on hopes that European leaders will reach a consensus on their rescue package this week.

https://soundcloud.com/user-291029717/european-plan-hopes-help-the-aussie-dollar?in=user-291029717/sets/the-morning-call

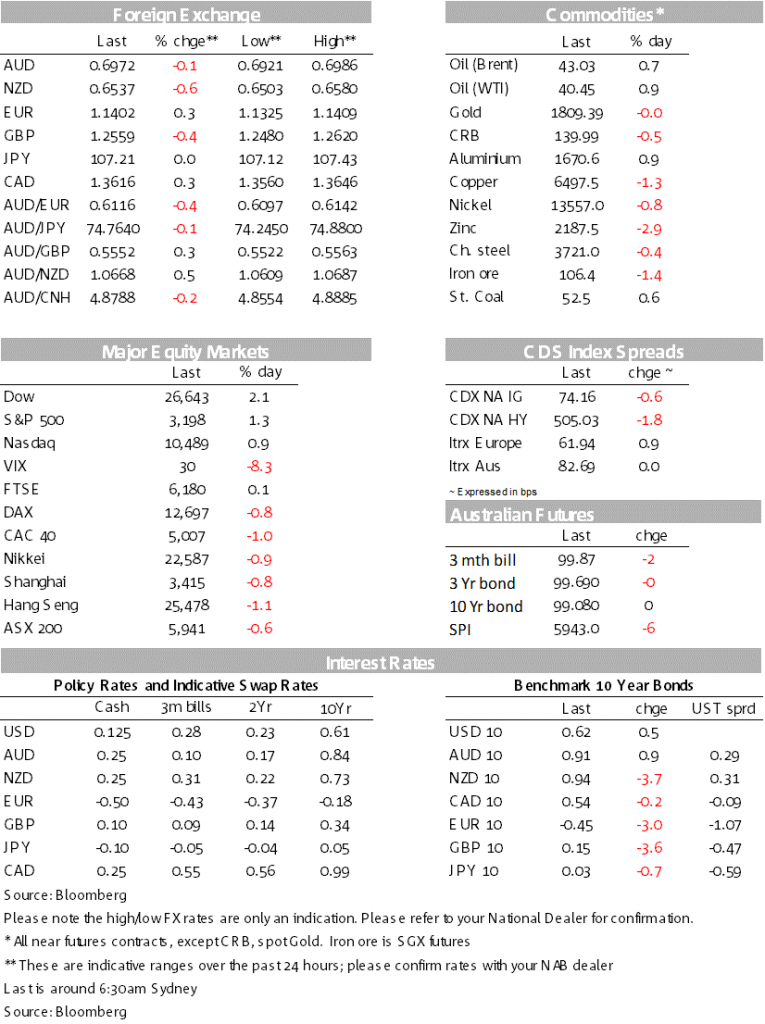

Risk sentiment was mixed with no clear direction from bank earnings and US equities surged into the close driven by underperforming cyclicals. The Euro rally continued with EUR +0.3%, helping drive a weaker USD (DXY-0.3%) with the AUD little changed at -0.1% on net and is currently sitting at 0.6973.

“All the people tonight, put your hands in the sky; Come on boy, come and get in the rhythm, music will take you high; What I’m feeling about you, I love you, don’t know why”, Inna 2010

“Sun is up” was the Euro rave pop song of 2010 and is still a regular feature at any spin class (if you can get a booking that is). So it was overnight with the Euro remaining in the ascendency with EUR +0.3% to 1.14 (a level not settled above since March), and putting the USD on the backfoot (DXY -0.3%). The move has been largely driven by speculation around the chances of the EU Recovery fund being approved by EU leaders when they meet later in the week. In G10 FX the NZD has been the worst performing currency over the past 24 hours, down -0.6% with the AUD little changed on net.

Equities also reflect the “sun is up” mood with the S&P500 rallying into the close to end +1.3%. Bank earnings were mixed and provided little direction for equities (JPMorgan +0.6%, Wells -4.6% and Citigroup -3.9%). Instead the rally was driven by underperforming cyclicals with industrials +2.2% and materials +2.5%. Also supportive of risk was reports of Moderna going ahead with a firm date for phase three trials – set for July 27. Yields were little moved in the US with US 10yr’s +0.5bps to 0.62%

JPMorgan’s trading revenues offsett a weak main street (earnings were $1.38 a share v 1.04 expected; trading revenue rose 79%). In contrast Wells Fargo more a main street name reported a net loss (-0.66 a share v -0.20 expected) and cut its dividend by 80%. All three major banks that reported today had larger-than-expected loan-loss provisions ($28bn across all three and highest since 2008). Worryingly for retail operations net interest margins were also squeezed at Wells (falling 33bps to 2.25% and below the 2.33% consensus). On the outlook, the banks sounded a cautious note, with Citi’s CEO Corbat saying “We don’t want people leaving the call simply thinking the world is a great place and it’s a V-shaped recovery.”

The Fed’s Brainard was also supportive of the late rally in risk with Brainard implying she was willing to run the economy and was supportive of using yield curve control as a Fed policy tool. Brainard cited research that would imply the Fed refraining from raising rates until inflation reaches 2% allowing a modest temporary overshoot. Yield curve control was also highlighted as a potential policy tool given the uncertainty over the recovery: “Given the downside risks to the outlook, there may come a time when it is helpful to reinforce the credibility of forward guidance and lessen the burden on the balance sheet with the addition of targets on the short-to-medium end of the yield curve” (see WSJ for details).

In the US Core CPI rose 0.2% m/m against 0.1% expected and taking the annual rate to 1.2%. Despite the headline beat the more interesting aspect was rents which make up a combined 40% of the CPI basket. Rents rose a mere 0.09% compared to the pre-COVID average of 0.3% a month with recent media pointing to falls in rents and suggestive of core CPI being weak for some time. UK May GDP was worse than expected, bouncing back only +1.8% m/m against the +5.5% expected. The consensus though did look a little optimistic given the UK only really starting easing up on restrictions from mid-May and a bounce in June is likely. A similar result was also seen in Singapore where Q2 GDP fell by 41.2%, missing expectations of a -37.4% fall. On a y/y basis GDP fell 12.6% versus expectations for a 10.5% contraction. Again lockdowns in Singapore only really started being eased in a meaningful way from early June.

The more interesting data print was the Chinese trade data yesterday which continued the string of upbeat June activity readings. June trade saw exports +0.5% y/y in USD terms (estimate -2.0%); imports +2.7% (-9.0% estimate and up smartly from -12.7% In May) with the rise in imports suggesting the industrial recovery is being sustained.

Australian data flow also continues to take a back seat with little reaction to yesterday’s payrolls, NAB Business Survey or virus news domestically. As for Weekly Payrolls, they showed around 35% of lost jobs have been recovered, though gains have slowed over recent weeks. The NAB Business Survey bounced sharply, reflecting the bounce seen in the PMIs globally.

Melbourne’s lockdown is yet to see a meaningful fall in new cases (270 new cases reported on Monday), if we don’t see that in the next couple of days than a harder lockdown could be implemented. The AFR today is running a piece along these lines with Victorian Premier Daniel Andrews stating they may need to “go harder” on restrictions if the numbers do not improve and high-level discussions were under way on Tuesday afternoon. A key reason why Victorian developments have not weighed on Australian markets to a great extent is that there has been little spillover from the Melbourne lockdown to the rest of Australia (weekly consumer confidence fell just -0.5% in the past week) and high frequency data continues to show a pick-up outside of Victoria.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.