Labour market strong, housing supply falling behind

Insight

Markets seem to indicate a little optimism on the outcome of the Trump-Xi meeting at the G20 this weekend.

https://soundcloud.com/user-291029717/false-hope-on-g20-unicorn-dreams-from-boris?in=user-291029717/sets/the-morning-call

Well I was sitting, waiting, wishing..Must I always be waiting, waiting on you? Must I always be playing, playing your fool? – Jack Johnson

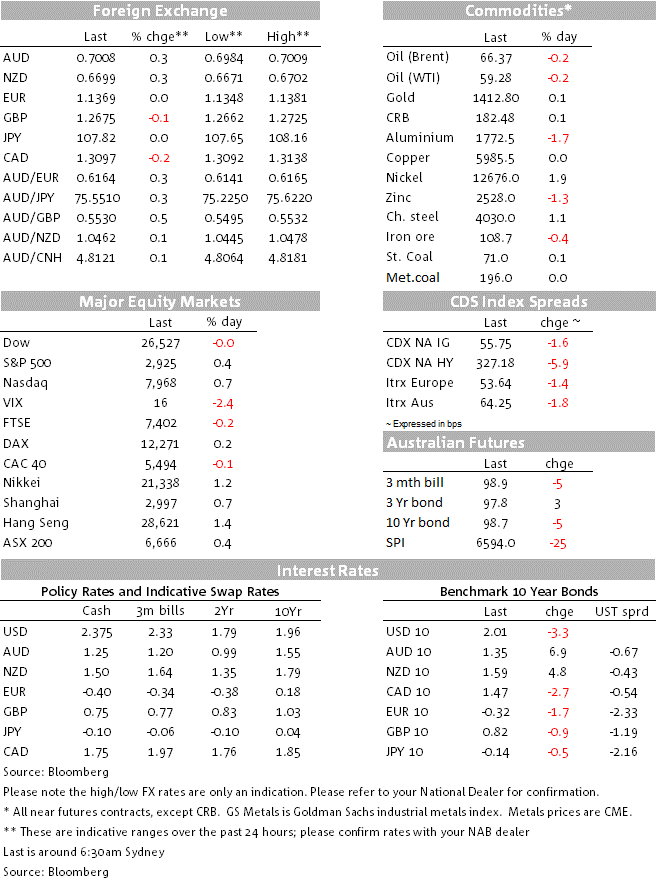

Well Friday has finally arrived and now we have to sit, wait and wish for a reasonable outcome out of Presidents Trump and Xi G20 meeting. Modest gains in US equities, halting a four day losing streak, suggest optimism is in the air, but the move lower in UST yields suggest otherwise. Meanwhile the USD is little changed, although commodity linked currencies have edged a little higher with the AUD back above 70c and NZD at 67c.

The mixed picture across markets reflects the mixed news flow over the past 24 hours. Yesterday a report from South China Morning Post suggesting US and China have tentatively agreed to another truce aimed at resolving their trade dispute was the catalyst for a lift in sentiment, boosting APAC equity markets with China’s CSI index and the Nikkei closing with gains above 1%. The report chimed with early comments from US Treasury Secretary Steven Mnuchin suggesting the two countries were closer to a deal and was followed by several similar reports pointing to a trade truce out the G20 meeting.

Early in the overnight session, however, the WSJ noted that China is seeking the removal of Huawei from the banned list before a deal could be made as well insisting on the removal of existing tariffs and an end to the demands for China to buy even more US exports. Adding to the confusion, a senior US administration official reported earlier this morning that nothing has been agreed ahead of time and that it is unlikely that the US would agree to lift restrictions on Huawei.

In spite of the positive lead from Asia, European equities ended the day in negative territory with the Eurostoxx 50 index recording its fifth negative day in a row. EU data releases didn’t help sentiment with euro-area economic confidence – a composite of business and consumer confidence – falling by slightly more than expected to its lowest level in three years. Ahead of the EU June CPI release tonight, Germany’s CPI inflation remained unchanged at 1.3%.

Core global yields have edged a little bit lower. A more cautious tone evident in EU equities alongside underwhelming data releases contributed to the move lower in 10y Bunds with the benchmark yield ending the day 1.7% bps lower at -0.32%. Meanwhile, longer dated bonds have led the decline in the UST curve with data releases contributing to the cautious market mood. The 30y rate is down 4bps to 2.53% while the 10y note is at 2.008% (-3bps). The Kansas City Fed manufacturing index slipped to zero, making it the fifth regional Fed survey to deteriorate this month, and setting the scene for a weaker ISM manufacturing index next week.

As it has been the case in recent times, compare to equities and bonds, currency moves have again been relative subdued with the USD little changed in index terms ( DXY @ 96.21 and BBDX at 1187.33) while commodity linked currencies are a tad stronger. After 17 days trading with a 6 handle, overnight the AUD has finally clawed its way back above 70c and now trades at 0.7008 (+0.24%). Based on CFTC data, AUD speculative short positioning is pretty extreme, so may be some of the AUD gains can be attributed to squaring of positions ahead of the G20 Trump-XI meeting, that said following the repricing of Fed rate cut expectations our AUD FV model has been suggesting a move back above 70c was in the offing while in a similar vein our EM AUD proxy model was also suggesting some upside.

NZD has been the other outperformer, rising for the ninth consecutive day, up 0.25%, breaking through some technical resistance at 0.6680 and is now hovering around the 0.67 mark. Yesterday on the NZ data front, the June ANZ Business Survey reflected still below-average levels of activity and business confidence, consistent with the RBNZ’s messaging this week of the risk of “ongoing subdued domestic growth”.

Yesterday we publish a note outlining what a new Fed easing cycle might mean for the USD and the AUD. The starting point is to assume the US and China agree an uncomfortable truce with no removal of tariffs, meaning the Fed is likely to embark on a new easing cycle at the end of July. (NAB’s call is two cuts this year, one at each of the next two meetings, July and September.) The USD has a bias to underperform in the first month after the Fed’s first rate cut. After an initial boost, AUD/USD performance is mixed, suggesting a range-trading environment around 70c over coming months. More telling, USD/JPY has downside risk before and after a new Fed easing cycle (read the full note).

Busy day for Japan, the unemployment rate is expected to print unchanged in May (2.4%) while the Tokyo core CPI reading for May, which tends to be a good leading indicator of the national reading, is expected to ease by on tenth to 0.7%. In contrast, consensus is looking for a small uptick in Industrial Production from 0.6% to 0.7% m/m.

Housing credit growth is forecast to slow a touch further to 0.2% m/m. We expect owner-occupied credit grew 0.3% in the month (was 0.4%), while investor credit was flat again. While business credit disappointed in April with a flat result, we look for a small 0.3% gain in May. Elsewhere, we expect another 0.2% decline in personal credit

Although consensus is looking for a small 0.2% uptick in core inflation to 1%, subdued energy and German package holiday prices suggest downside risk.

The April GDP report and the Business Outlook Survey are going be important for BoC guidance; the Bank doesn’t yet have a smoking gun in order to join other central banks easing mantra.

The May US Core PCE reading has some downside risks on the y/y due to rounding. Our core model suggests a 1.558% y/y print against a consensus of 1.6%, thus it is very easy to imagine core inflation might round down to 1.5%. The m/m print though should be on consensus at 0.2%. Going forward, core inflation is likely to remain subdued outside of possible tariff impacts.

The June Chicago PMI is also likely to be of market’s interest, in light of the softer prints by other regional PMIs, we would suggest there is downside risk to the 53.2 number expected by consensus vs the 54.2 print in May.

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.