Price growth edges lower despite reasonable economy

Insight

Hawkish hold by the FOMC/Powell sees yields rip higher and equities reverse earlier gains

https://soundcloud.com/user-291029717/fed-confirms-move-to-post-pandemic-policy?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

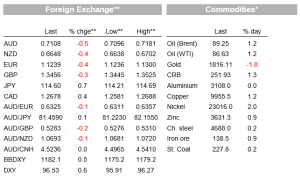

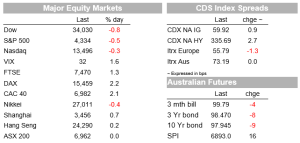

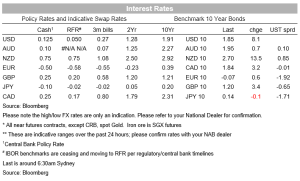

Risk assets fell sharply in the wake of the FOMC meeting overnight with Fed Chair Powell sounding hawkish, even if he tried to be measured. The headline of course was the Fed tipping their hat to a March rate hike and for QE to end in March. In the press conference though Chair Powell sounded hawkish as well as hinting the Fed put is a lot lower than the current -10.2% fall in the S&P from its peak. Yields sky rocketed with the 2yr yield up 11bps to 1.12% and the 10yr also up 7.7 bps to 1.85%. Markets have increased their pricing for Fed rate hikes to 4.8 being priced in 2022 from 4.2 yesterday. Pricing for a March rate hike also increased with a 40% chance of a 50bps hike. Equities tanked with the S&P500 -0.5% after having been up some 2.2% prior to the FOMC meeting. The USD also leapt higher, up 0.5% across the board with most currency pairs similar including the AUD which is down -0.6% to 0.7103.

Key for the markets were three comments that point to the risk of an aggressive Fed hike cycle. (1) Chair Powell noted: “I think there’s quite a bit of room to raise interest rates without threatening the labor market. ” That comment was taken in the same light as his 2018 words of being a long a way from neutral and suggests the Fed thinks it can raise rates substantially and above the terminal rate that is currently priced by markets which was 1.7% according to 5Y1Y FWD OIS. (2) Chair Powell noted “asset prices are somewhat elevated ”, perhaps hinting that the Fed put is a lot lower than it was in prior cycles and the Fed is not overly concerned about the fall in stocks as yet (note the S&P500 has fallen some 10% from its peak; and (3) some hint the Fed could move in increments of more than 25bps and could hike at consecutive meetings. Asked about a 50bps hike and a departure from the prior gradual pace of moves, Powell said the Fed really hasn’t addressed or a made a decision on that (he purposefully didn’t rule it out). Moreover, he then added “I can tell you that the situation now is very different from before” going on to list persistently higher than 2% inflation, econ growth that is still above potential late in 2022 and a very tight labour market.

Guidance on quantitative tightening (QT) was fairly vague with only a reference to starting the process after rate hikes have started, reduction will occur in a predictable manner, and at the end of it the Fed wants its holdings primarily in Treasuries and so hinting at a faster run off perhaps in agency mortgage backed securities (see FOMC – Principles for Reducing the Size of the Federal Reserve’s Balance Sheet for details). In the press conference Chair Powell said the Fed is “willing to move sooner” and “perhaps faster” than last time in shrinking the balance sheet. More guidance will be given at upcoming meetings.

The Bank of Canada also met overnight and delivered a hawkish hold, citing the Omicron variant as one reason not to hike in January as was 70% priced by markets, but signalled a hike at the next meeting in March. Governor Macklem noted: “we were mindful that the rapid spread of Omicron will dampen spending in the first quarter. So we decided to keep our policy rate unchanged today, remove our commitment to hold it at its floor, and signal that rates can be expected to increase going forward ”. Importantly the Bank “removed its exceptional forward guidance on its policy interest rate” given overall economic slack is now absorbed, which must mean every meeting should be considered live for hiking. The market now prices a 90% chance of a hike in March and more than six rate hikes are priced for 2022.

If realised, six hikes would see the Bank of Canada hiking at almost every meeting in 2022. Such a trajectory was hinted at in the press conference: “a path is not one move, a path is a number of steps. Secondly, a path doesn’t mean we’re on autopilot, it’s not automatic, and we will be assessing at each meeting,” “and a path doesn’t rule out that you would take a few steps and then we might pause and assess progress. ” The BoC also mentioned they could consider quantitative tightening by allowing maturities to roll off. There was a knee jerk weakening in CAD, as the market was 70% priced for a hike today, but that soon faded with USD/CAD little change over 24 hours at 1.2594 (see BoC: Monetary Policy Report Press Conference Opening Statement for details).

Also in central bank news, media with known links to the RBA suggest the Bank will move to considering 2022 for potential rate hikes given the better than expected progress on inflation and unemployment. However, the RBA will still argue that for inflation to be sustained at target wages need to rise to closer to 3% plus (see WSJ’s Glynn, AFR’s Kehoe’s, and The Australian’s McCrann). Inertia in the wage setting process probably suggests the RBA sees early 2023 as their central scenario, but their upside scenario now firmly sits in H2 2022. The risk for the RBA of course is that with a historically tight labour market and headline inflation running at 3.5% y/y, employee/union wage demands are realised earlier. Markets of course are well priced for the RBA moving in 2022 with four hikes fully priced.

As for data overnight it was mostly quiet and not market moving . The US goods trade deficit unexpectedly widened to a record high of $101b in December vs. $96bn expected. While this would normally put downside risk to tonight’s Q4 GDP estimate, there was a large jump in wholesale and retail inventories (retail 4.4% m/m vs. 1.5%) which has more than offset the impact on Q4 GDP. The Atlanta Fed’s GDP Now estimate now sits at 6.5% annualised, signalling upside risks to the consensus of 5.3%. New home sales were also strong at 11.9% m/m against 2.2% expected.

Finally, oil prices are up some 2.5% with Brent at over $90 per barrel for the first time since 2014. The weekly EIA report showed inventories at Cushing fell 1.8m barrels for the third week in a row, though total inventories rose 2.4m vs. expectations of a fall of 0.7m. The risk of sanctions against Russia is also weighing on the minds of traders. This could take some supply out of the market at a time when supply/demand conditions remain tight.

Domestically there is no top tier data with only Import/Export Prices scheduled. Offshore NZ has Q4 CPI figures with the consensus looking for another high print of 1.3% q/q. Focus then turns to China for Industrial Profits and then to the US for Q4 GDP figures. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.