Price growth edges lower despite reasonable economy

Insight

The US Fed has revised its growth forecasts for this year and next, and removed all dot points for rate moves this year.

https://soundcloud.com/user-291029717/fed-loses-its-dots-eu-issues-a-ransom-note

Markets were geared up for a relatively dovish Fed and in the event got something even more dovish than they expecting. It has been enough to significantly move the dial on the currency and interest rates, as well as supporting stocks where the S&P has rallied about 0.5% from its pre-Fed level. The exception here has been the banking sector (S&P financials -1.2%) where still-flatter curves are among banks’ worse enemies. We’re almost at the point where US banks will need to be borrowing long and lending short to make money.

US indices have just closed with the S&P up 0.3%, the Dow 0.5% and NADAQ flat.

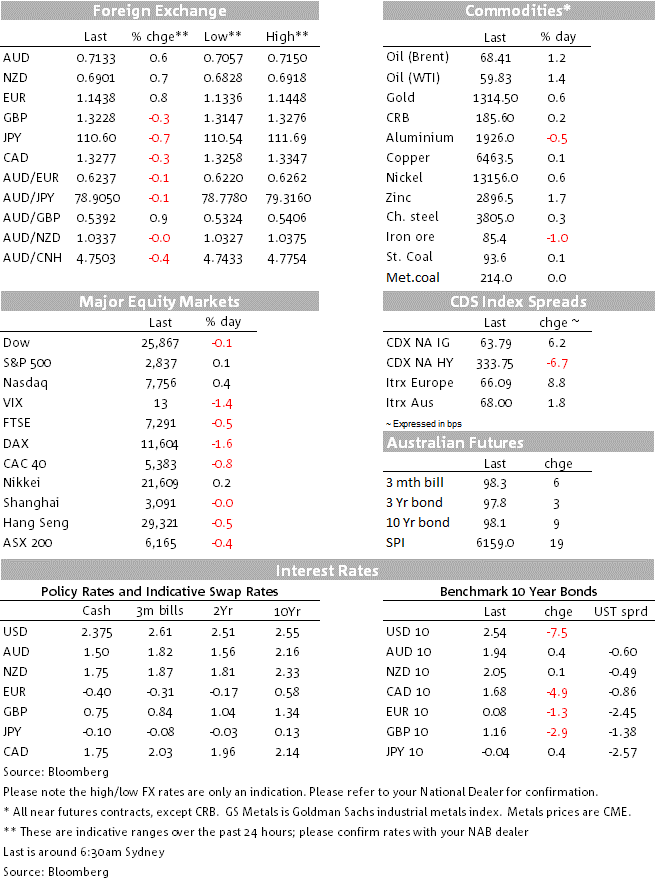

In terms of reaction, the OIS market now ascribes a 45% change to a quarter point cut from the Fed by year-end, up from 30% this time yesterday. 10 year US Treasury yields have dropped by 5.5bps from their pre-Fed level to 2.53% (and 8.5bps down on Tuesday’s NY closing level). The DXY dollar index is 0.65% down to 95.88 to its lowest level since 4th February.

All G10 currencies bar GBP are up, led by SEK (+0.9%), CHF (+0.8%) JPY and EUR (both 0.7%) respectively, while AUD and NZD are both about 0.5% higher.

GBP came under fresh pressure on news that UK PM Theresa May was requesting only a short Article 50 extension, to June 30th, from the EU. In response, EC President Donald Tusk said that a short delay was possible, but contingent on the UK parliament passing Theresa May’s Brexit bill in parliament, where a third meaningful vote (MV3) will more likely than not take place next week.

Regarding the chances of this getting up, it’s worth noting comments from Labour MP Lisa Nandy a few hours ago, who suggests she could table a motion that could win the support of other labour MPs whereby they would support Mrs May’s withdrawal agreement proving parliament, rather than the government, then had control of the trade negotiations to take place during the transition period (to run through end 2020).

Elsewhere the latest on Sino-US trade are reports that the US administration was not planning to remove the existing tariffs on Chinees imports for some time after a trade deal is struck (if it is), pending sufficient evidence of Chinese compliance with the agreement. This could be a major sticking point from the Chinse side. We can put hope it’s all part of the ‘Art of the Deal’, but in the meantime means we can’t as yet fully price in a trade deal next month, or later, with supreme confidence.

The only economic news of note was UK CPI where the headline was slightly higher than expected (1.9%) but core CPI marginally lower (1.8%); so both measures are just below the BoE’s 2% target.

First up this morning is NZ Q4 GDP. Our BNZ colleagues are looking for a 0.5% increase, slightly below the Bloomberg consensus of 0.6% and well below the 0.8% implied in the RBNZ’s last MPS).

Then it’s eyes down for February Australia Labour Force Survey. We forecast flat employment growth in February (market: +15k) and an unchanged unemployment rate of 5%, though with risks skewed to an upside (5.1%) surprise (5.1% or higher) rather than downside (4.9% or less). The latter is because of our below-consensus forecast for employment and also – though we don’t play this up – given the possibility that ‘sample rotation’ biases the rate up in so far as the 1/8th cohort falling out of the survey have a lower unemployment rate that the 7/8th staying in.

As for potential market reaction, note that in the surveys, there are more economist saying 5.1% (8/24 on Bloomberg) than 4.9% (only 1/24) and therefore you could argue that 4.9% will be a bigger surprise than 5.1% and therefore worthy of a bigger market reaction. We’d agree, all the more so given where the market already is with regards to RBA rate cut pricing. If unemployment prints at 5.0% (or lower) this would mean no ‘smoking gun’ as yet for the RBA to shift its current thinking, which is that the justification for rate cut(s) is rising unemployment.

Up later tonight is the ECB’s Economic Bulletin, UK Retail Sales and Public Borrowing and the Bank of England. Latter should be a non-event. Then in the US we have the Philly Fed survey and weekly jobless claims.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.