Price growth edges lower despite reasonable economy

Insight

The Fed's stance has had a strong impact on markets in the immediate aftermath.

https://soundcloud.com/user-291029717/fed-more-dovish-uk-parliament-more-unicorn

US equities were having a good night ahead of the Fed announcement, the USD was steady and UST yields were drifting higher. As expected the Fed delivered its patient pledge and also confirmed a review of its balance sheet normalisation guidance. Risk assets loved the Fed message with US equities jumping across the board. Post the Fed, the UST curve is steeper with the move led by a rally in front end yields. The USD is also broadly lower with AUD and CAD the outperformers.

As expected the Fed stood pat and delivered a more dovish message relative to its December Statement. The Fed removed its reference to further gradual rate changes and consistent with official speeches post the December meeting, the Committee has pledged to be patient on further adjustments to the target range. Notably the Fed reasoning for its patience is largely attributed to “global economic and financial developments and muted inflation pressures” whilst its assessment of the US economy remains encouraging “The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes”. Speaking before the media, Fed Chair Powell said that the case for rate hikes has weakened somewhat and although the outlook remains “favourable” “we are now facing a somewhat contradictory picture,”. Powell then added that there’s growing evidence of cross-currents and patiently waiting for greater clarity has served policy makers well in the past.

In a separate statement the Fed said that the Committee is “prepared to adjust” the details of balance sheet normalisation if required and also hinted such an adjustment is likely by stating “the Committee is revising its earlier guidance regarding the conditions under which it could adjust the details of its balance sheet normalization program”.

Risk assets have reacted positively to the Fed Statement and Powell’s comments, it seems the Fed has listened to markets and is watching the global outlook closely with a “muted” inflation outlook allowing the Fed to be “patient” in determining future rate moves. As noted above, however, the Fed assessment of the US economy suggest its bias is still for funds rate to be higher in the future. Stabilisation in global growth and renewed signs of inflationary pressures are themes to watch.

US equities were already enjoying a good day buoyed by better than expected Apple results (after the bell yesterday) and news that Boeing’s earnings had beaten expectations by a significant margin. The Fed patient message was an additional boost and as we type the S&P 500 is 1.88% stronger while the NASDAQ is 2.44% higher.

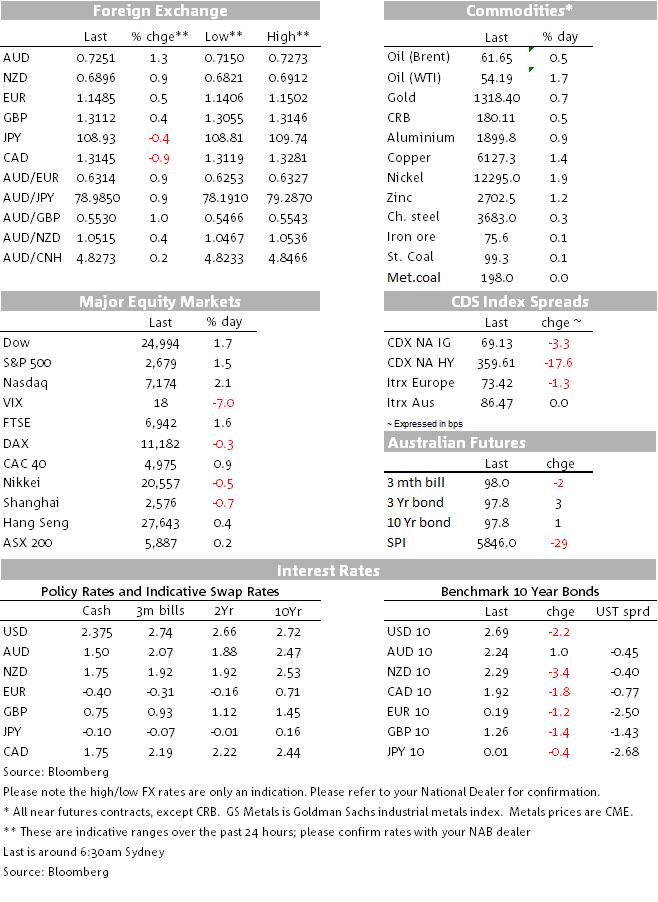

Ahead of the Fed the big dollar was marginally higher, but a mover lower in shorter dated yields along with a decline in safe haven demand triggered a broad USD sell-off. In G10 AUD (+1.41%) and CAD (0.94%) are the outperformers. Both pairs were outperforming prior to the Fed announcement. Counter to its safe haven attributes JPY is also stronger (USD/JPY is down almost one big figure to ¥108.95, following the move lower in UST 10y yield).

Yesterday a marginally better than expected Australian CPI boosted the AUD with price action suggesting the market was positioned for a soft outcome. Movements in iron ore prices have also helped the Aussie with the bulk metal trading above $80 in Asia. The CAD also benefited from a move higher in oil prices (WTI +2.02%) with the viscous lubricant benefiting from Venezuelan political crisis and glacial weather in some parts of the US. As we type the AUD trades at 0.7255, finally breaking higher from the tight 0.7076 and 0.7235 held since after the January 3rd crash. Technically the AUD is looking constructive with many looking at the 50WMA at 0.7378 as the next target a more dovish RBA is a risk next week from a fundamental basis a Fed led risk positive environment and higher commodity prices are all good news. Of course the caveat hear is the binary outcome from the US-China trade talks due to end tomorrow.

GBP has recovered somewhat after the Fed and now trades at 1.3110. Overnight the pound was under a little bit of pressure following news that the EU seems in little mood for compromise with EC President Juncker saying that the backstop was “part and parcel” of the deal and would not be renegotiated. He added that the risk of a disorderly no-deal scenario had increased. There is still time for UK MPs to vote to extend the leave date of March 29th if PM May is unsuccessful in securing concessions from the EU over the next few weeks, as seems likely. We retain the view that a no-deal scenario is unlikely.

The UST curve steepened led by a move lower in front end yields(2y down 3.5bps on the day to 2.526%), 10y UST yields fell 2bps to 2.69% and interestingly the 30y note is higher up 1.6bps to 3.057% relative to yesterday’s levels. For all the talk of recessionary risk implied by various yield curves, 5s30s is at its steepest in almost a year, at 55bps. A Fed on hold implies a rangy environment for UST yields and a favourable atmosphere for risk assets.

As for the latest on US-China trade talks, Bloomberg reported that the two sides remained far apart on some of the deep-seated issues like US demands that China revamp its industrial policies and take greater steps to protect intellectual property. Ahead of the talks, China’s National People’s Congress fast-tracked a law that would formally ban ‘forced’ technology transfers from foreign firms operating in China, although it’s uncertain whether that will be sufficient to assuage US concerns. The China CSI300 index was 0.4% lower yesterday, with more than 20 companies reporting lower than expected earnings results, a further sign of the slowdown in growth in the country. But the CNY strengthened further against the USD overnight (+0.3%) and the currency is now at its highest level since July last year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.