Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Despite trade talks, shares continue to rise, but for how long? And what’s happening to Australian inflation – a temporary falter or the start of a softening trend?

https://soundcloud.com/user-291029717/friends-again-or-playing-one-against-the-other

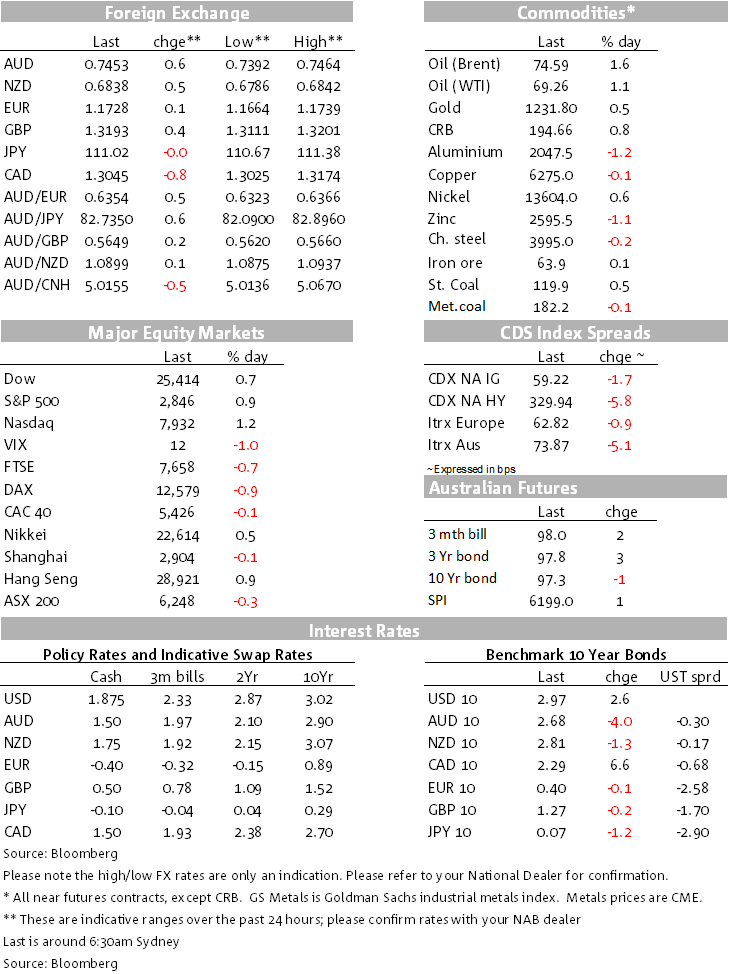

US equities have closed higher overnight, getting a late push into the close after a post-meeting press conference with President Trump and the EU’s Juncker, the bonhomie between the two also evident earlier as the talks began with flattering comments from each. The USD has been softer pretty much across the board and softened further after the rose garden presser an hour ago, with late-session support for the Euro and others as stocks have rallied into the close. Yields pushed up too. After dipping after yesterday’s CPI, the AUD was been brought along for the ride overnight and sits this morning around 0.7450.

Adding earlier to risk on sentiment was a report in the Washington Post that had earlier reported the US Commerce Department was considering a range of options to address Trump’s concern about car imports, even though it was understood that Trump’s advisors believed his preference was to use tariffs. Meanwhile, EU Trade Commissioner Malmstrom warned that the EU was preparing a list of US goods worth $20 billion for retaliatory tariffs, if Trump goes down the route of imposing auto tariffs.

The rise in equities came despite sharp falls in US car manufacturers GM and Fiat Chrysler after both companies downgraded their earnings estimates for the remainder of the year. GM cited higher raw material costs, and in particular the higher cost of steel and aluminium as a result of tariffs, for its profit downgrade.

It was the post meeting press conference that provided a further late session spark to risk appetite. Earlier press backgrounding had suggested that the Europeans were giving concessions on lowering industrial tariffs and buying more US soybeans among other concessions. The rose garden press conference came with statements that they will work to resolve steel and aluminium and retaliatory tariffs, a new phase in US-EU relations, a “close relationship”, “strong trade relations”, and more. They stated that they will work together toward zero tariffs, zero non-tariff barriers, zero subsidies on non-auto industrial goods. That’s the sort of news that’s music to the market’s ears, with little doubt that this is also tilted from the US across the Pacific to China.

The main three pieces of fundamental news were a weaker than expected US home sales report for June (suggesting activity might be fading), a somewhat stronger than expected German IFO, but the US EIA reporting a much larger than expected drawdown in US crude inventories di impact the market. The still pretty upbeat nature of the German Ifo survey added to signs from yesterday’s PMIs that the German economy is still making solid growth progress and came notwithstanding the potentially destabilising trade war/tariff news and the possibility of the US imposing auto tariffs. It’s also some growth comfort ahead of tonight’s ECB meeting.

The AUD initially softened yesterday after headline CPI inflation came in marginally lower than expectations. Both the RBA’s core measures of inflation met expectations (1.9% y/y%) and with inflation still bumping along below the bottom of the 2-3% target band and the unemployment still pointing to some spare capacity, the market came to the conclusion that the RBA remains firmly on hold for an extended period.

The AUD reversed course thought the afternoon session and overnight, the market paying more attention to the growth-supportive nature of targeted easing measures in China and in the past hour or so the positive spill-over from the Juncker-Trump talks. Also overnight, the PBOC was reported to have eased counter-cyclical capital requirements for banks in an attempt to boost lending.

Bond yields were reasonably stable for the second day running but yields pushed higher late session from the US-EU trade news. The 10 year Treasury yield is up 2.6bps to 2.9746%, the 2s-10s yield curve back out to 31bps. There were limited moves in Japanese government bonds ahead of the BoJ’s monetary policy meeting next week.

The larger news on the commodity front overnight was a lift in oil prices, WTI up $0.74 to $69.26/bbl after a 6.147mbbl draw in US crude inventories, much larger than the 2.234b expected drawdown.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.