Price growth edges lower despite reasonable economy

Insight

Jobs numbers from the US on Friday were well above expectations and we saw a swift response in the markets.

https://soundcloud.com/user-291029717/good-jobs-news-bad-for-a-trade-deal?in=user-291029717/sets/the-morning-call

Concerns that the US labour market might be rolling over, aggravated earlier in the week by the soft ADP employment print, were more than fully assuaged Friday by a nothing short of stunning employment report. Non-farm payrolls rose by a much stronger than expected 266k (180k expected, including returning GM strikers) added to which were 41k worth of upward revisions to the prior two months.

This was enough, aided by a fall in the labour participation rate from 63.35 to 63.2%, to see the unemployment rates fall to a new cycle low of 3.5% from 3.6%. To cap it off, average hourly earnings growth is now tracking above 3%; October was revised up to 0.4% from 0.2% to push yr/yr growth up to 3.2% from an original 3.0%, November’s 0.2% gain then pulling this down to 3.1% but still up on where we were in September.

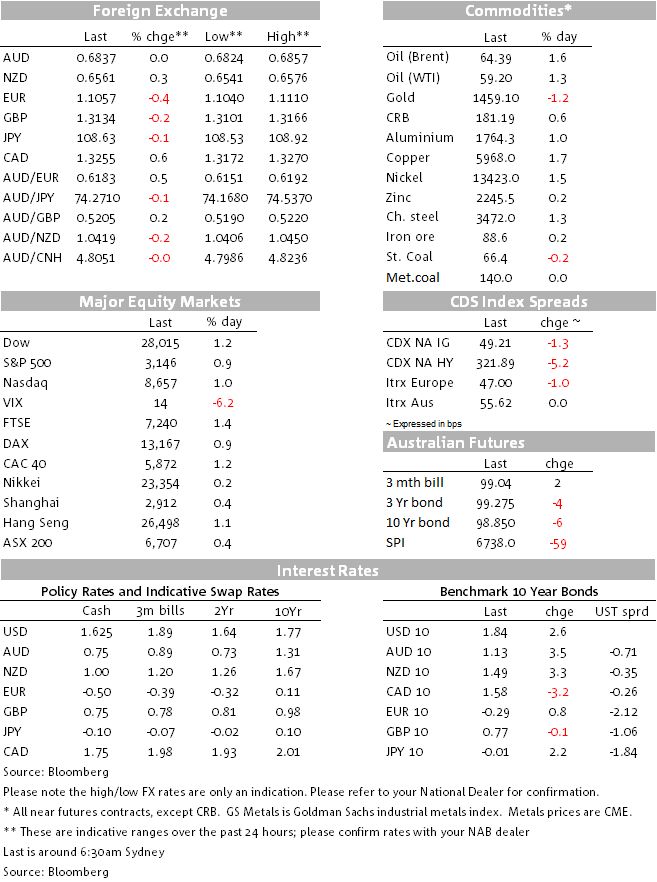

The report saw the S&P500 rising back to within spitting distance of its November 28 record closing high, +0.9% on the day to 3,146, though the index is barely up on the week (+0.16%). One reason, perhaps, for a relatively muted reaction across equities and other asset markets – e.g. two and ten year Treasury yields up about 3bps and 5bps respectively, and the USD ‘only’ up about 0.3% – is because the evidence of ongoing US economic strength lessens the pressure on President Trump to strike an early phase One trade deal with China ahead of Sunday’s current deadline for imposing new tariffs on China. The Atlanta Fed’s latest GDPNow estimate, for example, was revised up to 2.0% from 1.5% after the payrolls report.

Also helping risk sentiment on Friday and inspiring confidence in the ongoing strength of the consumer side of the economy was the preliminary University of Michigan consumer sentiment index, up to 99.2 from 96.8 an well above the 97.0 expected. Despite the strength here, doubtless driven by a combination of equity market gains during the month and the number of new people falling into work, the closely watched – by the Fed at least – 5-10 year inflation expectations reading fell back to 2.3% from 2.5%.

In sharp contrast, employment in Canada in November fell by a whopping 71.2k and its unemployment rate surged to 5.9% from 5.5%, albeit hourly earnings growth is a still strong 4.4% (unchanged on October). This meant CAD was the weakest G10 currency on Friday, followed by the EUR, the latter’s 0.4% loss driving much of the 0.3% rise in the DXY dollar index. The EUR had earlier failed to take hit, somewhat surpassingly, from a woefulGerman October industrial production report, showing 1.7% monthly fall and pushing annual growth much deeper into negative territory, -5.3%y/y down from -4.5% in September.

Weakness in CAD came despite a jump in oil prices on Friday afternoon, on ne that OPEC+ had agreed not only to maintain existing production curbs, but that Saudi Arabia would cut another 500,000 barrels from tehri output alongside a pledge by other OPEC+ members to collectively reduce production by 400,00 barrels. Cynics might suggest this has something to so with Saudi Arabia’ desire to se Aramco’s market cap. Hit $2tn in coming weeks. But be that as it may, the news had a big impact, Brent crude jumping from around $63 to almost $65 before settling at 64.40 at the NY close.

Sunday’s November China trade data contained some ‘overs and unders’ but not enough to be a major early-week market influence. In USD terms, the overall trade surplus came in a little weaker than expected at $38.7bn (from $42.8bn in October and $44.5bn expected) on a combination of stronger than expected imports, now back into positive yr/yr terrain at 0.3% from -6.4% last time (-1.4% expected) and exports were on the weak side of expectations, -1.1% yr/yr down from -0.9% previously and +0.8% expected.

The AUD was something of a bystander on Friday through appeared to draw a little support from a still-rising NZD, the latter benefiting during our time zone from upbeat comments from RBNZ deputy governor Geoff Bascand, in front of this Wednesday’s expected announcement of ;’significant’ fiscal stimulus in the HYEFO. That AUD held up in the face of USD strength was notable, though the AUD/.NZD cross continue to fall, on Friday to below 1.0420 and its lowest levels since early August. IMM positioning data published on Friday, for the week ending last Tuesday, shows speculative NZD shorts being pared back, to -26k from -36k previously (and too in AUD, from -45k to -36k).

The AUD/GBP cross pulled up[ a little on Friday from its earlier excursion below 0.52, awaiting the latest batch of opinion polls in front of Thursday’s general election. The FT’s poll tracker this morning, updated though Sunday, shows the Tories with an average 10-point lead over Labour. Enough, were that translated into actual vote on Thursday, to deliver a modest majority for Boris Johnson.

International considerations dominate the market skyline this week

The results of Thursdays UK General Election should be known during our time zone on Friday. A comfortable outright Conservative majority in predicted by the polls and 70% priced according to the bookies. The residual uncertainty is such that we would still expect a significant reaction in GBP and UK risk asset markets (with spill-overs to Eurozone markets) if this is indeed the outcome, As our BNZ chief economist remarked last week with respect to the RBNZ’s bank capital announcement, ‘Knowing the lie of the land – even if you don’t like the look of it – is usually so much better than not knowing it’

Even more important in the scheme of things, Sunday night is currently the deadline after which the United States is due to impose tariffs on a further $160bn worth of Chinese imports – most of them consumer goods – if no ‘Phase 1’ trade deal has been reached by then. Of course, the deadline could be extended, but markets will be on tenterhooks all week until we get news one way or the other. Geopolitics and structural issues aside (Hong Kong, treatment of Uyghur Muslims, China’s alleged state-subsidised capitalism, forced technology transfer/IP rights, etc.) the fate pf any Phase 1 deal appear to turn on just two factors – satisfactory numerical commitment by China on US agricultural purchase, and agreement to at least partial tariff roll-backs by the United States.

Locally, Wednesday’s NZ half year economic and fiscal update is expected to firm up on the magnitude nd form of planned fiscal stimulus to come into effect next year. In Australia, the NAB November business survey on Tuesday and Westpac read on consumer confidence on Wednesday, look like being the highlights.

The FOMC meets Tuesday and Wednesday (no change expected) and the ECB on Thursday, which will be Christine Lagarde’s first in the chair, making the post-meeting press conference of interest

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.