Price growth edges lower despite reasonable economy

Insight

The Bank of Canada delivered on an almost universal expectation for a 25-point rate hike last night.

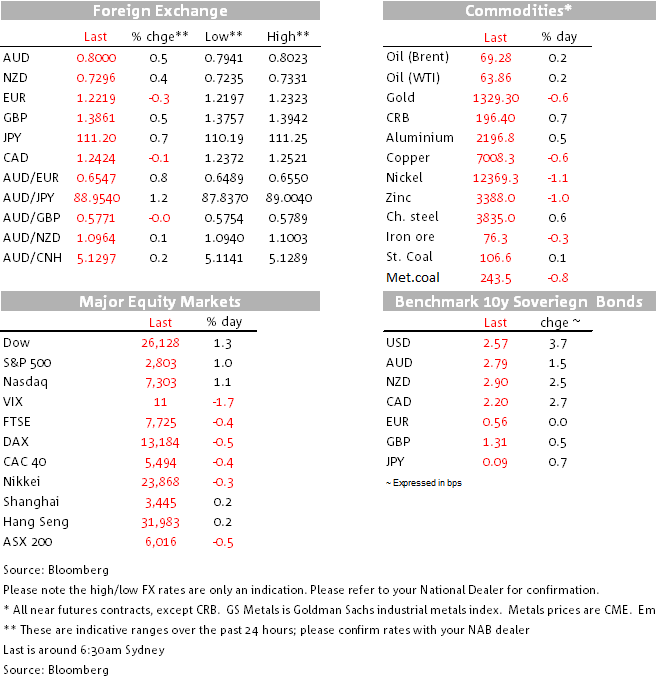

The Bank of Canada delivered on an almost universal expectation for a 25-point rate hike last night. While saying it would adopt a cautious approach to further tightening in order not to choke off growth (and also citing NAFTA as one particular concern) money market pricing continues to ascribe more than 100% probability to a further move no later than May (27.1bps on Bloomberg’s calculator). A knee jerk ‘sell the news’ response in all things CAD (USD/CAD to 1.2520 from around 1.2400) has since been fully reversed, the ‘loonie’ sitting pretty much where it was pre-decision.

A growing chorus of European Central Bankers are imploring markets to rein in their enthusiasm for the Euro. ECB’s Vice President Constancio noted overnight that “I am concerned about sudden movements which don’t reflect changes in fundamentals”, the latter reflecting the modest tick down in inflation. He signalled that there is little prospect of a change to policy language next week, arguing that officials should be careful not to “choke off growth too soon.” The ECB’s Nowotny also weighed in, saying that Euro appreciation “is not helping” and that while the ECB “has no exchange rate goal” it must be watched in terms of its impact on economic developments.

The Euro’s near term course remains important for the AUD; while we forecast significant depreciation in the AUD/EUR rate later this year, for the time being EUR strength is proving to be a ’rising tide that floats all boats’. That said, the break above the 80 cent level in AUD/USD in the last couple of hours (to 0.8023, since reversed) has come despite EUR/USD currently trading below the 1.2323 high seen around midday yesterday, albeit it has recovered most of the ECB-rhetoric inspired losses witnessed during the European session.

If today’s local employment data prints well above expectations, which NAB sees a as distinct risk (consensus 15k, NAB 35k) then last September’s 0.8125 high will come quickly into focus, probably alongside rising confidence the RBA will be lifting rates in the second half of the year.

The US dollar in general continues to ignore positive incoming news, last night’s being a consensus-busting 0.9% rise in industrial production (with net positive backward revisions), albeit flattered by a 5%+ surge in utility output due to last month’s Arctic weather. The Fed’s beige Book noted “on-going labour market tightness and challenges finding qualified workers across skills and sectors, which, in some instances, was described as constraining growth”. At the same time wages were described as increasing “at a modest pace” in most districts and price gains “modest to moderate” (Bloomberg reporting).

Also to note is Apple saying that it will bring back $38bn into the United States as a result of the changes to the tax code and requirement to pay tax on earnings stashed offshore. Apple says it will invest $30bn in the U.S, in the next five years. $328bn represents about 15% of Apple’s $252.3bn overseas cash pile (which is also the tax rate to be applied to profit held in liquid assets abroad). Given the estimate $3.1tn in profits held overseas across all of corporate Americas, 15% would amount of some $465bn of total repatriation (remember only the taxes to be paid, not the gross profits, need to be returned).

Given that taxes due can be spread over 8 years (and back-loaded) and much of the cash is already in dollars (we don’t know how much) the annual flows back into dollars from this source are hardly going to touch the sides of the FX market. Certainly they aren’t going to be the dollar-positive force we thought last year that they could be. That said, actual flows could be larger, to the extent US multinationals choose to repatriate more than just the amounts required to pay their taxes, either to invest in ‘Making America Great Again’ or (more likely?) to facilitate share buybacks and//or additional dividends.

Incoming Fed speak continue to span the hawk-dove divide, Robert Kaplan (Dallas, non-voter this year) old the WSJ he sees three rate rise this year but the risk skewed to the need for more in order to prevent overheating. He is speaking again as we write, saying that ‘cyclical inflation pressures are building’, though offset by some structural factors like technology. He’s also lamenting that tax cuts are coming just when the US is at or near full employment (he sees unemployment in the ‘3s’ by end 2018 due to the tax cuts). Chicago Fed President Charles Evans meanwhile (also a non-voter this year) says that while US fundamentals are very strong and he is confident inflation will move back to target, its important for monetary policy to support the economy. Recall a week or so again Evans said he would have preferred a six month delay to the rate hike the majority agreed to in December.

Elsewhere, we still don’t know if a US government shutdown after tomorrow will be averted (the working assumption is that it will, the dollar will suffer it is isn’t).

Bitcoin plunged below $10,000 overnight down from its $19,511 December high, but has since come back though this level. The year-on-year gain has been reduced to a mere 1,130%.

Local employment at 11:30, where the unemployment rate will be important as well as the aforementioned employment change. Consensus and NAB are both for an unchanged 5.4%.

The monthly slugs of China activity readings are currently scheduled for 15:30 AEDT, but GDP not until 18:00 (a delay was announced yesterday afternoon, for reasons unbeknown).

Offshore tonight, US housing starts and Philly Fed survey.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.