Price growth edges lower despite reasonable economy

Insight

Australia’s latest unemployment numbers are out this morning and the rate is expected to rise.

“Made promises without fear of getting burned; Now we’re always second guessing; We think happy is expensive; But every time I’m with you I re-learn; It’s the invisible things that I, that I love the most” Lauv, 2020

Markets are still trying to grapple with the implications of rising coronavirus infections and hospitalisation rates in the southern parts of the US given there is a high bar to re-impose lockdowns. Texas is particularly worrying with an 11% rise in hospitalisation rates over the past 24 hours and hospitalisations are now up 84% since memorial day. The other factor weighing is the chances of a Democratic clean sweep come November (i.e. Presidency, House and Senate), with those chances likely bolstered following excerpts from Bolton’s new book stating the “president pleaded with Chinese leader Xi Jinping for domestic political help, subordinated national-security issues to his own re-election prospects and ignored Beijing’s human-rights abuses” (see WSJ for details).

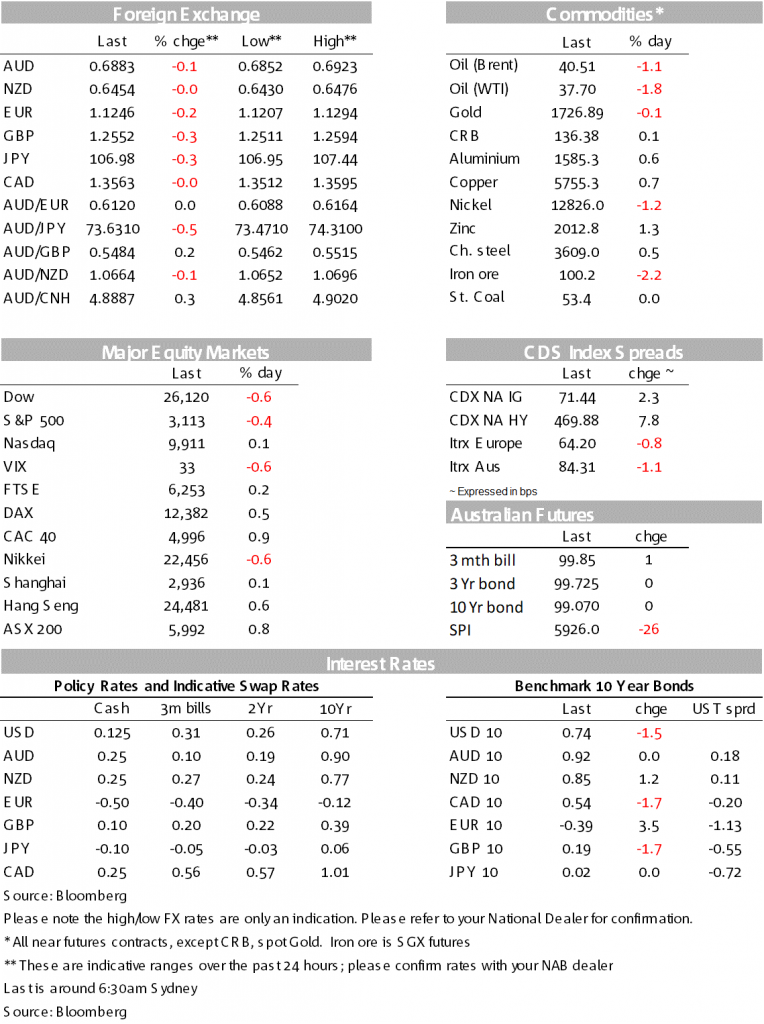

Equities were choppy and fell into the close on the Bolton headlines with the S&P500 closing down -0.4%. FX moves have been modest with mild USD strength (DXY +0.1%) amid the cautious tone with EUR -0.2% to 1.1246, GBP -0.3% to 1.2552 and USD/Yen -0.3% to 106.98. The AUD is also a touch lower, -0.1% to 0.6883 with today’s jobs numbers under focus. Weekly payrolls earlier in the week suggests you cannot rule out a positive surprise (see coming up below for details). Yields were little moved overall with the US 10yr -1.5bps to 0.75%. Data was sparse with UK CPI missing a tenth (core 1.2% y/y v. 1.3% expected), US housing starts/permits a touch softer than expectations. US Fed Chair Powell mostly re-iterated his comments to the Senate at the House today, while also urging Congress to not pull back on fiscal support too quickly.

A number of southern US states continue to see a rise in new coronavirus infections, though it has been downplayed by officials who cite greater testing numbers – including the Vice-President Pence who in a WSJ Opinion piece said “There Isn’t a Coronavirus ‘Second Wave’. With testing, treatments and vaccine trials ramping up, we are far better off than the media report” (see WSJ for details). While partly true given a ramped up testing regime, rising hospitalisation rates do point to a more worrying development. Texas overnight reported hospitalisations were up 11% overnight and are now up more than 84% since Memorial Day. In detail there are now 2,793 patients hospitalised with a coronavirus infection in the state with 1,473 spare ICU beds and 13,815 general hospital beds. Texas’s Governor Abbott continues to downplay the development, stating “We have plenty of room to expand beds, there are thousands of hospital beds that are available as we speak right now” (see CNBC for details).

It’s unclear how markets should react given the obvious high bar to re-impose restrictions in the US and states across the US are continuing to re-open their economies. High-frequency mobility indicators continue to point towards a pick-up in activity across in the US and including Texas. China in contrast is taking aggressive action in Beijing where another 31 new coronavirus cases were reported yesterday. Schools have been shut in the city and almost 70% of flights out of Beijing were cancelled yesterday but the authorities have so far taken a more targeted approach to containing its spread (compared to the lockdown imposed in Wuhan).

The chances of a Democratic clean sweep (of the Presidency, House and Senate) is now starting to gain traction with PredictIT giving it a 54% chance recently. Bolstering that view overnight was John Bolton (Trump’s former National Security Adviser) who in published excerpts of his yet to be published book, noting “The president pleaded with Chinese leader Xi Jinping for domestic political help, subordinated national-security issues to his own re-election prospects and ignored Beijing’s human-rights abuses”. While conscious of not straying too far into politics in a Daily, Bolton’s words do blunt Trump’s China strategy which he was likely to campaign hard on in the election. Either way markets have started to assign probabilities of a Democratic clean sweep and what policies would likely emanate if they control three arms of government. That should play into a weaker USD view.

UK CPI came in softer than expected with core at 1.2% y/y against 1.3% expected and down from last month’s 1.4%. US housing figures were a touch softer than expected though still strong with homebuilder sentiment pointing to an aggressive pick-up in activity in the months ahead (housing starts 974k v 1,100e; permits 1,220k v 1245e). On the positive side, the drop in Q2 activity is likely to be a lot less than initially feared with shipping companies revising their forecasts. Giant Maersk noted business was doing better than forecast and now expects volumes to fall 15-18% in the second quarter compared to a previous forecast for a 20-25% drop.

A busy day ahead with Aussie job figures and across the ditch NZ has their Q1 GDP. Offshore, the BoE meets and US Jobless Claims will be watched closely to see whether the labour market has sustained its improvement. Key releases below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.