Price growth edges lower despite reasonable economy

Insight

It’s been a scratchy session, says NAB’s David de Garis, as markets shy away from sharp moves ahead of Friday’s payrolls data from the US.

https://soundcloud.com/user-291029717/ignoring-the-talk-waiting-for-the-facts?in=user-291029717/sets/the-morning-call

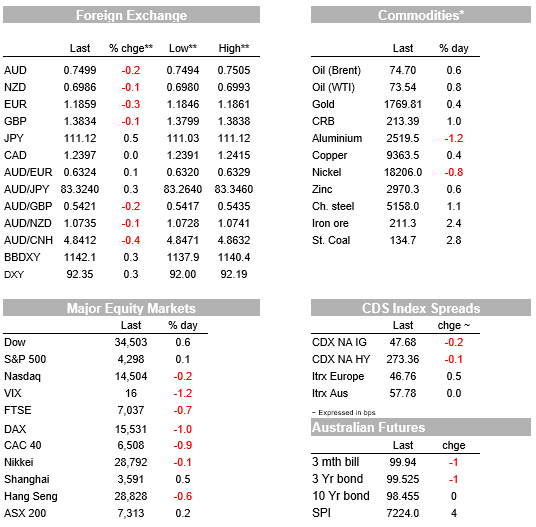

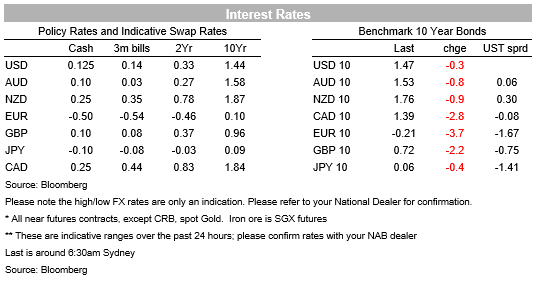

Another quiet night ahead of US Payrolls on Friday. While there was plenty of top tier data and central bank speak, the market remains cautious and fixated on payrolls. Month-end flows were evident with the USD broadly stronger into the London Fix (BBDXY +0.3%) and may have also been a factor behind an intra-day drift lower in US Treasury yields which has now been mostly reversed (US 10y -0.3bps to 1.47%). Equities were mostly in the green with the S&P500 +0.1% to another record high with the S&P500 up 2.2% in June to close out a very strong quarter (+8.2%) and half (+14.4%).

Data was mixed and largely ignored. US ADP Payrolls was slightly stronger than expected at 692k (consensus 600k), though it was no smoking gun for the million plus payrolls print that many are hoping for on Friday based on separate Home Base data. ADP of course is far from infallible, subject to heavy revision given it uses prior payrolls as an input (illustrated again overnight with the prior month revised down by 100k to 886k). A range of possibilities thus remains possible for Friday where the consensus is for 711k.

The Chicago PMI was much weaker than expected (66.1 v. 70.1 expected), though there was some nuance. Production and new orders slipped with anecdotes of “lower production levels due to material shortages”, while the prices paid index lifted to its highest level since 1979 and supplier deliveries index to its highest level since 1974. Supply chain disruptions thus appear to be weighing on production and the wider ISM Manufacturing Index released later today will be watched closely in this respect.

Some tentative easing in input costs though may be starting to occur in some sectors. Overnight lumber prices fell -5.5% and since the peak in early May lumber prices have tumbled some -57%! The price of lumber at 716 is falling back towards its pre0pandemic levels of around 400. The sharp fall in lumber prices is giving some heft to the argument that recent price increases will prove transitory with the concentration of demand for goods and home renovations fading as consumers pivot back towards services and travel.

US Fed speak was also not market moving, with both Kaplan and Bostic repeating their recent lines. Kaplan again advocated for a tapering of asset purchases sooner and noted the public discussion means markets are aware and reduces the likelihood of a taper tantrum (“People are on notice that these adjustments are coming, the only question is when.”). Fed Governor Waller yesterday post NY close also played to the view that an initial taper could be led by MBS (“ Right now the housing markets are on fire; they don’t need any other unnecessary support…And it’s an easy sell to the public.”). Across the pond outgoing BoE Chief Economist also continued his hawkish lines warning on inflation and inflation expectations.

There was also heaps of other international data with most interesting being the Chinese PMIs where the Non-manufacturing PMI fell to 53.5 (from 55.2), while the Manufacturing PMI was little changed at 50.9. The easing in the Non-manufacturing PMI continues the soft tones around China’s services sector, while chip shortages are no doubt impacting on the manufacturing sector as it is elsewhere in Asia. Japanese Industrial Production plunged in May by -5.9% m/m due to the chip shortage affecting auto production. Delta variant outbreaks also have the potential to impact on production in the near-term. Supply chain pressures so far though are not feeding into end inflation in Europe with the Core CPI at 0.9% y/y.

In terms of FX moves, it appears month-end buying of USD was the most likely driver for USD strength (BBDXY 0.3%). JPY, one of the better performers for the month, has been one of the weakest performers overnight, seeing USD/JPY blast up through 111 to reach a 15-month high. EUR is also on the soft side, down 0.3% to 1.1859. Antipodean currencies were weaker in the face of USD strength with the AUD -0.2% and NZD -0.1%. The AUD again testing below 0.75 and currently trading at 0.7499.

Finally in terms of Australia, there is an MNI sources piece out suggesting the RBA remains sceptical on the outlook for wages despite the unemployment rate falling to 5.1%. Seemingly that would suggest a need for the RBA to push back on market pricing so dovish tones could be evident at the July Board Meeting even as the RBA does not roll its 3yr YCC target and as QE is tapered (as is NAB’s view). A re-statement of the conditions for a rate hike being not likely until at least 2024 would be one way to push back on market pricing. Not tapering QE with a defined program length would be another.

Domestic focus remains on virus numbers and how long lockdowns last for in the four capital cities that are currently in lockdown (Sydney, Brisbane, Perth and Darwin). Datawise we get the Trade Balance and Job Vacancies which are unlikely to be market moving. Further afield all focus will be on the ISM

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.