Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

It’s been a dovish couple of days for central banks.

https://soundcloud.com/user-291029717/is-a-rba-rate-cut-even-more-likely

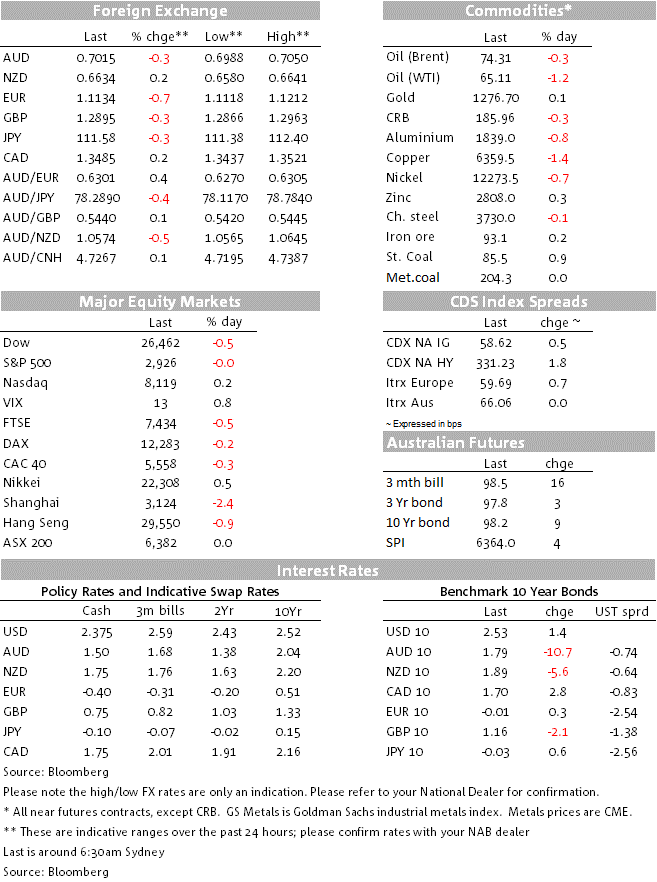

The big dollar has been soaring this week as a sequence of news continues to draw a sharp distinction between diminishing carry on offer elsewhere compared to the attractiveness of USD carry. The AUD has been at the front of the selling que this week, selling arriving in an instant upon release of Wednesday’s CPI that missed on both the headline and core measures, seeing the market price in another one third chance of the RBA going in May and now priced for two cuts this year. The RBA is set to push out reaching its 2% inflation forecast at least into 2020.

To recap, the AUD was sold down quickly from just below 0.71 to around 0.7030, probing lower levels since in the wake of other central bank news either continuing with their super-accommodative policy bias (the BoJ), or changing tack from a mild tightening bias (BoC, Riksbank). The market was also served up with a disappointing April German Ifo Survey on Wednesday and a better than expected US Durable Goods Orders report for March overnight. US weekly jobless claims jumped 30K last week, though this has been largely discounted owing the Easter seasonal adjustment problems and possible a supermarket strike across some States (since resolved).

The local market is now around 50%-plus priced for a cut in May. RBA watchers in the financial press have had different views since, James Glynn (WSJ) writing that the RBA could cut by up to four times this year (sic) to arrest the inflation undershoot while Terry McCrann contends that the better unemployment report means a rate cut is still not coming in May.

The market is now priced for two cuts this year, NAB’s view. Given the growth and inflation undershoot together with still evident global and domestic growth headwinds (centred around housing), it would not surprise too much if the RBA Board cut rates on May 7 Tuesday week, even with a still OK labour market. (NAB had pencilled in July as the first cut, contingent on the data. The inflation data of course has opened the door further for the RBA to move earlier given the more subdued outlook.)

The re-adjusted short-end rates pricing spilled over into the NZ rates market, with the OIS market pricing in 16bps of easing for the May meeting (up from 12bps) and 40bps of easing by November. As my BNZ colleague Jason Wong has also noted this morning, the RBNZ’s May MPS on 8 May is the day after the RBA’s decision, the market taking the view that the odds of the RBNZ cutting rates next month would be a lot higher if the RBA were to cut rates. NZ swap rates fell by 4-5bps across the curve while rates across the government curve were 6bps lower.

The global theme since the pre-ANZAC day close has been more dovish overtones by central banks around the world, with the Bank of Canada, Bank of Japan and Sweden’s Riksbank all offering more dovish outlooks in their policy statements.

In chronological order, the Bank of Canada kept its policy rate unchanged at 1.75% but abandoned its bias towards higher rates, instead looking to “evaluate the appropriate degree of monetary policy accommodation” and removing reference about the timing of future rate increases. Governor Poloz noted that the Bank’s policy outlook would be data dependent but added that if the Bank’s forecasts were right then interest rates were more likely to go up than down. CAD weakened after the announcement, and that has largely been sustained, with USD/CAD near 1.35. AUD/CAD is at 0.9459, about where it plunged to after Wednesday’s CPI.

The Bank of Japan amended its forward guidance on low rates, saying that would keep interest rates extremely low “through at least around spring 2020”, compared to its previous message that rates would remain low for an extended period. The Bank nudged down its inflation and growth outlook, projecting that inflation won’t hit the 2% inflation target any time before March 2022, with the final year forecast sitting at 1.6%. There was little market reaction, with the market already pricing in negative bond yields through the next 10 years anyway.

Trading in JPY has been more influenced by the long Golden Week holiday that begins next week. The yen is stronger ahead of that as traders cut short positions ahead of the holiday. USD/JPY is down to 111.33, while AUD/JPY sitting back just above 78 this morning.

Sweden’s Riksbank offered more dovish guidance, pushing out its plans to tighten monetary policy and extending its bond buying programme. SEK fell around 1.5% after the surprising announcement and this seemed to have a negative spillover effect on EUR. The euro fell to 1.1118 its lowest level since mid-2017, before finding some support.

In the previous night’s session, a weaker German IFO business survey for April did some damage as well. Note that the coverage of the German Ifo survey was widened a year ago to include services so a lower level for both the headline Business Climate index in April compared to the March quarter and the Current Assessment index. Improvement in China’s economy should show up soon. AUD/EUR has recovered half of its post-CPI loss, back to 0.63, up from 0.6270 and 0.6320 pre-CPI.

In other news, South Korea GDP unexpected fell in Q1, indicative of the recent slump in global trade, exports accounting for about half of Korean GDP. Global trade volumes are falling at their fastest pace since the GFC. Still, there is some hope that the low in growth momentum has been reached, with “green shoots” emerging in China. US economic bellwether 3M reported weak earnings, citing a China slowdown as a key factor, driving its share price down 13%. While this dragged down the Dow Jones Index, the S&P500 is slightly positive for the session.

In US economic news, durable goods orders were stronger than expected, even for the core measure. The recent plunge in jobless claims to a 50-year low proved too good to be true, with evidence that it was driven by seasonal adjustment issues with the late Easter. Claims rose 38k to 230k for the week ending 20 April.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.