Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

China’s M2 money supply grew less than expected on Friday.

https://soundcloud.com/user-291029717/how-fast-is-china-slowing

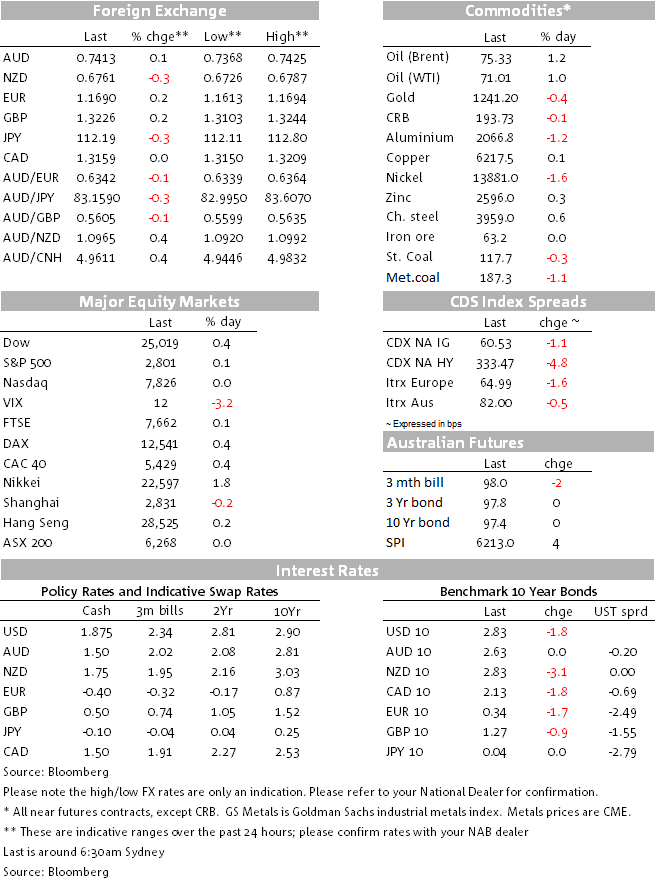

In FX, when Australia was heading home on Friday the US dollar was making gains against all currencies, the Euro and Sterling in particular were leaking lower and the offshore Chinese Yuan (CNH) had just risen above 6.72, the latter taking AUD down with it. This moves came just after China loans and money supply numbers were reported at 17:00 AEST. They showed a further fall in M2 money supply growth (8.0% y/y from 8.3% and versus 8.4% expected), while the broad Aggregate Financing credit numbers showed expansion by a much weaker than expected Y1,1180b. This is a rebound from Y760.8bn in May but well below the Y1,535bn expected. In contrast new Yuan loans grew by a bigger than expected Y1,840bn, a sign that shadow banking activities are being successfully curbed in favour of traditional bank lending. But the overall message is that credit conditions are still tightening.

Monday’s China June activity numbers will be important. Evidence of a further slowdown in growth rates for Fixed Asset Investment, Industrial Production and/or Retail Sales will be seen as adding to China’s tolerance of CNY weakening, with ramifications for Asia EM FX more broadly and with that AUD.

AUD fell to a session low of 0.7370 from an earlier high of 0.7420, but came back during the New York afternoon to land back exactly at 0.7420. It’s re-opened for the week just below here. There was no obvious catalysts for the turnaround later on Friday, though Sterling mounted a comeback after President Trump publicly apologised for his reported attack on UK PM May’s Brexit strategy and apparent support for Boris Johnson as PM. He suggested the Sun newspaper had omitted a lot of positive things he had said about the PM, and that a trade deal between the US and UK was still possible. His wants the ‘tough’ Mrs May as his friend not his enemy, he intoned. ‘Fake Schmooze’ is the Sun’s headline on all this this morning!

President Trump has since turned his fire onto the EU, telling CBS over the weekend that he considers the EU a “foe” that had taken advantage of the US with its trade practices. This on the day before Trump is due to meet with Russian President Vladimir Putin.

AUD ended up as Friday’s best performing currency (+0.22% on Thursday’s close) and NZD the weakest (-0.43%), so AUD/NZD just about matching its 3rd July of 1.0993 and its best since 31st January. DXY ended 0.16% lower at 94.67 having been as high as 95.25. On the week, the USD was stronger across the board with DXY +0.75% while AUD fared best among G10 currencies (down 0.1% versus the USD but higher against all other currencies. JPY and SEK fared worse on the week (both -1.7%) while NZD/USD lost 1.1%. The latter means that the AUD/NZD cross is back challenging the 1.10 level.

In Equities, US stocks had a good night even though bank stocks fell post the earnings reports from JP Morgan, Citigroup and Wells Fargo. JPM and Citi beat both their earnings and revenue estimates while Wells Fargo missed on both counts, despite which JP Morgan’s shares lost 0.5% and Citi 2.2% (Wells Fargo finished 1.2% lower). JPM’s EPS of $2.29 bear the $2.22 consensus and Citi’s $1.63 its $1.56 estimate. Both banks cited a strong economy and related loan growth as supporting their results.

It was industrials, consumer staples and the energy sector (latter helped by a 1% rise for WTI crude) that drove the 0.1% rise for the S&P500 with the banking sub-index -0.46%. The Dow gained 0.4% while NASDAQ was flat despite record closing highs for Amazon, Facebook and Microsoft. On the week, the S&P gained 1.5% and the NASDAQ 1.8%

In Bonds, US yields were lower across the curve despite stocks market gains, 2s -0.8bps, 5s -2.2bps and 10s -1.9bps to 2.83%. On the week, the 2yr yield is +4bps and 10s +1bp, so the 2/10s curve flatter by another 3bps to a new cycle low of 25bps. Aussie 10yr futures implied yields fell 2bps on Sycom on Friday night.

Commodities saw WTI oil gained 70 cents to $71.01 and Brent 90 cents to $75.33. Industrial metals were lower again, with LMEX -0.16% while gold lost $5.40 to $1,241. On the week, LMEX has lost another 1.8% and is now just over 14% down on its early June highs. Brent crude is $1.80 lower and WTI crude off $3.80.

In economic news, the main US data point on Friday was the preliminary University of Michigan consumer sentiment index, which at 97.1 was down on 98.2 in June and a fell a little short of the 98.0 expected, but still very strong in absolute terms and with no signs as yet that trade fictions are impacting sentiment (the sharp rise in the price of washing machines notwithstanding). Current conditions fell to 113.9 from 116.5 while expectations held up, 86.4 from 86.3. Of some significance, 5-10yr inflation expectations, closely watched by the Fed, fell to 2.4% from 2.6%

Atlanta Fed president Raphael Bostic spoke Friday, saying he favours one more interest rate hike this year ‘as things currently stand’. ‘I may be okay with four’ moves this year if the economy dictates that stance, he said.

The Fed released the formal text for Jay Powell’s semi-annual testimony to Congress this week, in which the Fed outlines its base line view for further gradual rates rises. Of some note and at a time when President Trump is railing against high petrol prices and demanding higher OPEC production, the report notes that “much and of the negative effect on GDP from lower consumer spending is likely to be offset by increased production and investment in the growing U.S. oil sector. Consequently, higher oil prices now imply much less of a net overall drag on the economy than they did in the past, although they will continue to have important distributional effects.”

Locally, weekend auction clearance rates as supplied by CoreLogic showed a preliminary nationwide clearance rate of 55.8% versus last weekend’s final 52.6 on still-declining auction volumes (1,172 down from 1,411). Sydney cleared a preliminary 52.4% vs a final 50.1% last week and Melbourne 60.0% (56.1%). Final clearance rates should be lower than this.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Labour market strong, housing supply falling behind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.