Price growth edges lower despite reasonable economy

Insight

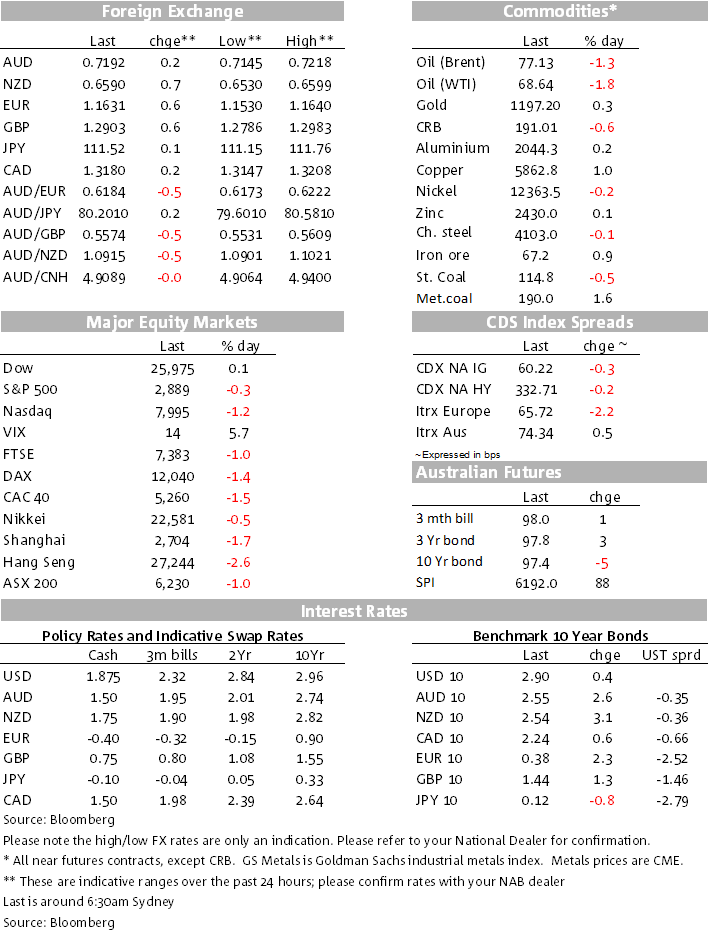

The Aussie dollar was higher despite continued woes in emerging markets, whilst the pound gained strength on positive hearsay on Brexit negotiations.

https://soundcloud.com/user-291029717/aussie-growth-brexit-hopes-and-tech-concerns

The USD has taken a breather for once as the market waits for any news from the White House as early as this week on additional tariffs on another $200bn of Chinese imports. The DXY index has pretty much pulled back to where it ended last week. The AUD and other currency pairs have clawed back some territory for now, the GBP and the NZD outperformers overnight, for different reasons

As we come in this morning, the AUD is sitting close to 0.72 having repeated its whipsaw pattern for the second day running, yesterday initially high on the stellar GDP print (even above our above-consensus pick) but relenting as USD support reversed that post-GDP spike. The AUD briefly then tested below 0.7150 in the APAC session, but there appears to be less continuing enthusiasm for the USD, despite looming news out of the White House on new tariffs on $200bn of Chinese imports. (There was very little US data overnight to swing things one way or the other.)

The Kiwi has outperformed in the past 24 hours, more likely from some unwinding of short positioning/flows with little Kiwi specific news to trouble the scorers. If anything, the NZ second tier data yesterday was mostly on the softer side. The AUD/NZD sits just over 1.09 this morning.

Sterling has had its own rollercoaster overnight, getting a big 1-1½ big figure move higher on a more conciliatory approach from Germany to Brexit. Germany and the UK are said to drop key Brexit demands, the Bloomberg headline said. Seemingly veritable anonymous sources say that Germany is ready to accept a less detailed agreement on the U.K.’s future economic and trade ties with the EU in a bid to get a Brexit deal done. The idea would be that the Europeans and the U.K. would be willing to settle for a vaguer statement of intent on the future relationship, postponing some decisions until after Brexit day. Kicking the can down the road.

Gavin Friend, our London-based strategist makes the point that given agreement on the Withdrawal Agreement is said to be 80% done, any easing up or loosening of the future economic and trade ties could make reaching a deal easier. But he fails to see how a ‘vaguer’ future trading arrangement will work with Parliament’s ‘meaningful’ vote requirement? The UK Parliament will need to be able to make an informed decision. One of the big fears of “Remainers” is that the UK exits without all this detail properly sorted and then it’s too late. Sterling sits at 1.291 this morning, (AUD/GBP at 0.557) having tested 1.2950 (AUD/GBP tested 0.554). The German government came out and said that their position was unchanged, reversing a good part of Sterling’s move higher.

Elsewhere in Europe, conciliatory remarks from Italy’s Di Maio (one of the two Deputy PMs) that Budget talks had been very productive and budget laws will keep Italy finances in order. He suggested that the flat tax and citizens’ basic income will be included with all sides working on how these are funded. Italian bond yields pulled back on the day. This is also an unfolding story not yet complete. The Euro has also made some gains against the USD.

The CAD has been relatively steady. The BoC left rates on hold as expected and continues signalling a near-term rate hike, offering some intraday support, as did news that the Canadians are back negotiating NAFTA with the Americans in Washington. As a headwind for the loonie, oil prices were lower overnight ahead.

The US trade deficit for July was very close to expectations, this report coming after the preliminary goods only trade balance released a week ago and confirming a monthly rise in the trade deficit.

Apart from oil, it’s been patchy on the commodity front, the LMEX up 0.46%, gold up even less, but the iron ore and met coal higher. Bond yields were contained and marginally higher in the main with European stocks lower as was the Nasdaq, weighed down by the FANG stocks. Netflix and Twitter stock down over 6% as key tech executives came under the spotlight on Capitol Hill.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.