Price growth edges lower despite reasonable economy

Insight

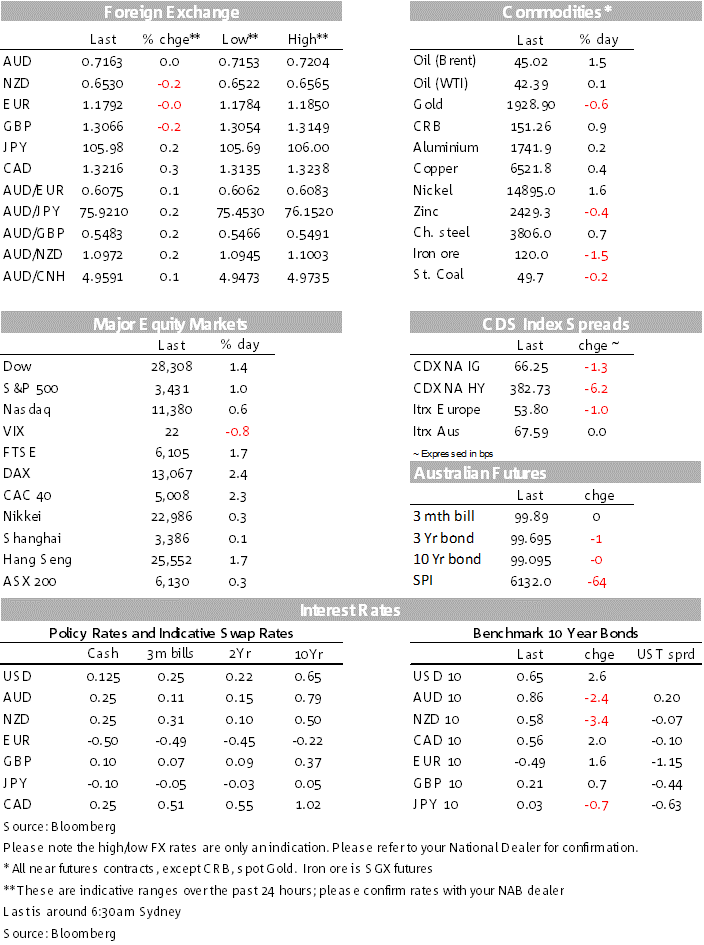

US equities reached new highs again, with big gains also in Europe.

Everybody is special in their mind’s eye

Oh, oh, oh, oh, oh…

Night, up all night, up all night, up all night – The Young Knives

Equities are higher on both side of the Atlantic, US Treasuries have led the move up in core global bond yields and the USD is also higher, although only modestly. CAD is the notable G10 underperformer while the AUD and NZD are little changed.

Equity investors are looking at the bright side of life with positive virus news outweighing the negative ones. US and European indices have started the new week with a spring in their step, the S&P 500 is +1%, NASDAQ +0.60% and the Stoxx Europe 600 Index surged 1.6%. Equity gains have been broad based with companies likely to benefit from economies reopening leading the gains.

Markets have warmly embraced the weekend news that the Trump administration is considering bypassing normal US regulatory standards to fast-track an experimental coronavirus vaccine from the UK for use in America ahead of the presidential election. The other positive virus treatment development has been the news that the U.S. Food and Drug Administration is working to expand access to a virus treatment involving blood plasma from recovered patients.

New COVID19 cases in the US dropped to around 35,000 for the day, the lowest level in more than two months with California, one of the US hotspots averaging 6k cases a day for the first time since June (4946 tested positive on Monday, down from 6777 on Sunday).

All these positive news have overshadowed the sharp rise in European infections with countries such as France, Germany and Italy recording their highest daily number of virus cases since April-May.

Hong Kong researchers recorded the first genetically proven case of COVID19 re-infection some 4½ months after the patient originally caught the virus, although symptoms were milder in the patient’s second case. The finding provides early evidence that COVID19 might behave like the common cold, continuing to circulate for years to come.

Although the BBC notes that experts have also said that reinfections may be rare and not necessarily serious. Those infected develop an immune response as their bodies fight off the virus which helps to protect them against it returning. The strongest immune response has been found in the most seriously ill patients. But it is still not clear how strong this protection or immunity is – or how long it lasts.

Particularly for US tech companies has been a report that White House officials have reassured American businesses that a ban on its WeChat app won’t be as broad as feared. This is good news for US companies like Apple and of course Tencent, WeChat’s owner.

The USD has again gone against its negative relationship with equities that has dominated since the start of the COVID-19 crisis. Albeit only modestly, the USD has also gained some ground on a broadly positive day for equities. BBDXY is up 0.09% while DXY is up 0.07%.

Price action in FX has been very subdued with changes within +/-0.2% against the USD for all the key majors. CAD is the major exception, down 0.40% notwithstanding a positive night for oil prices. Brent is up 1.56% and WTI +0.20%. Hurricane threat from storms Marco and Laura Gulf of Mexico have prompted the evacuations of off-shore energy platforms. Bloomberg reports that analysts estimate more than 15% of US oil production has been affected and should weigh on supply over the near term.

Evident in equity markets, the AUD is essentially unchanged relative to yesterday’s opening levels. The pair currently trades at 0.7163, closer to its overnight low of 0.7154, than its overnight high of 0.7204. The AUD continues to find resistance above the 72c mark. The NZD has traded a tight range and is a tad softer at 0.6529, after trading to an overnight high of 0.6565. EUR is back to 1.1800, after running up to 1.1850 overnight.

Although the broad theme is higher core yields led by the move up in UST yields. The US 10-year rate has been confined to a 3bps range of 0.62-0.65% and currently at the top of that range. 10y Bunds closed at -0.491%, up 1.6bps.

President Trump kick started his official nomination for a second term with a fiery speech alleging that his opponents were attempting to steal the November election, questioning the safety of voting by mail and accusing Democratic nominee Joe Biden of being a puppet of Beijing. So for now we have not learned anything in terms of Trump policy plans over his second term, the president is scheduled to speak nightly during the four-day convention, so hopefully we get a bit more colour over the coming days.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.