Price growth edges lower despite reasonable economy

Insight

The market found some relief on the notion that the FOMC Minutes revealed a broad consensus for 50bps hikes in June and July and the possibility for a pause later in the year.

https://soundcloud.com/user-291029717/markets-accept-rate-hikes-if-they-tame-inflation?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

As it is often the case the FOMC minutes had something for everyone, but the market found some relief on the notion that the Minutes revealed a broad consensus for 50bps hikes in June and July and the possibility for a pause later in the year. After opening lower, US equities have ended the day in positive territory with European counterparts also recording a rebound. There was a mild flattening of the UST curve led by a move up in the front end while the USD is a tad stronger with EU currencies the major underperformers. Premier Li acknowledge China is currently faring worse than in 2020 calling on officials to ensure unemployment falls and the economy “operates in a reasonable range”.

The FOMC Minutes revealed a broad consensus for the need to tighten the policy rate by 50bps over the next couple of meetings with “many participants” judging that “expediting the removal of policy accommodation would leave the committee well positioned later this year to assess the effects of policy firming and the extent to which economic developments warranted policy adjustments.”.

The headline was welcomed by the US equity market, but as it is often the case there was more to the Minutes than just that. The text also revealed a universal agreement that not only inflation was too high, but also that the labour market was too tight with the Minutes noting the elevated level of both job openings and the quit rate. This view reinforces the FOMC plan to get to “neutral” expeditiously, but importantly, in our view it also highlights the need for inflationary pressures and tightness in the labour market to show signs of easing before the Fed looks to take its foot of the tightening pedal. So, while the FOMC would like to pause sometime later in the year, this decision remains data dependent.

A 100 bps lift in the Fed Funds rate over June July would take the target rate to 1.75%-2%, in theory at the lower end of where the Fed sees the “neutral” rate (i.e. 2% to 3%). That set the stage for the Fed’s Jackson Hole Symposium late in August as the event to watch, often in the past the Fed Chair speech at the symposium has revealed important conclusions on the Fed policy thinking. Importantly too, the Jackson Hole gathering is likely to set the tone for what to expect out of the September FOMC meeting which also includes a new set of forecasts as well as a new dot plot.

Currently the rates market is very focused on whether the Fed will look to take the funds rate above neutral what the Fed reveals in September will be important for the market rationale on how high 10y UST yields can go in this cycle as well as the outlook for the USD.

QT also got a mention in the Minutes noting “several” policy makers saw risk of “unanticipated effects” on markets from the Fed’s plans to let billions of UST bonds mature each month without replacing them.

After struggling at the start of the session, the S&P 500 rebounded following the release of the FOMC minutes, embracing the comments over the prospect of a possible pause to the tightening cycle sometime before the end of the year . The S&P 500 closed the day up 0.95%, reversing a bit more than half of the losses recorded in the previous day. The NASDAQ also enjoyed a positive day, gaining 1.51%, partly reversing the 2.51% decline on Wednesday. Early in the session, EU equities closed higher with the Swedish market the notable exception ( -0.96%). The Euro Stoxx 600 index gained 0.63%, essentially reversing the previous day’s losses.

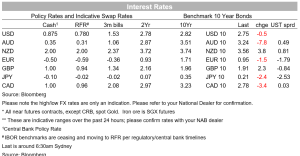

Reaction to the FOMC minutes in the UST market triggered a small sell off in the front end of the curve with the 2y UST yields climbing 2.4bps to 2.497% while the 10y Note was little changed at 2.745%. Early in the session 10y Bunds closed 1.6bps lower at 0.947%. The market continues to price 50bs hikes in June and July with the pace of hikes easing thereafter ~25bps per meeting, taking the Fed Funds rate to 2.65% by the end of the year.

More ECB officials have come out in support of Lagarde’s plans to exit negative rates by the end of September, as set out in a blog post a few days ago. The question for the market is whether that it involves 25bps hikes in July and September or whether there might a 50bps at one of the meetings. On that front, overnight Vice President Guindos refused to rule out a 50bps hike in July, saying “it will depend on the outlook…let’s see what happens”. That’s consistent with Lagarde’s recent comments to Bloomberg TV where she said “when you’re out of negative, you can be at zero, you can be slightly above zero .” The market is pricing around 65bps of hikes by the end of September, implying a slightly better-than-even chance of one 50bps hike by then. Meanwhile, several ECB officials, including Knot and Panetta, have suggested that the central bank is in no rush to start ‘quantitative tightening’, unlike the Fed and Bank of England, which will be a relief to peripheral European government bond markets.

The ECB comments provided little help to core EU yields or the euro. Indeed the euro and EU currencies are the notable underperformers over the past 24 hours with SEK down 1.12% while the euro is down 0.52% to 1.0682, the union currency is finding it hard to sustain a move above 1.07 and arguably ahead of the ECB meeting in June, the market is now well priced for a hawkish message, suggesting we may be heading towards a classic buy the rumour sell the fact event.

Movement in other currencies have been relatively subdued. GBP somewhat surprisingly is at the top of the leader board, up 0.39% to 1.2574, probably benefiting from the euro selling pressures. Meanwhile after trading lower late yesterday (overnight low of 0.7036), the AUD has recovered some ground to 0.7089, essentially unchanged over the past 24 hours. T he kiwi on the other has given back all of its RBNZ gains, the currency spiked to above 0.65 in the wake of the MPS, but it has since given back most of those gains overnight and trades this morning at 0.6476. Global factors, rather than the RBNZ policy outlook, remain the key drivers for the NZD and they are generally pointing downwards.

On this latter point and also of relevance for the AUD, Chinese Premier Li admitted the Chinese economy might struggle to grow in Q2, which was “a far cry from our 5.5% [annual GDP growth] goal.” . The premier outlined 33 support measures aimed at helping businesses, including more than 140 billion yuan ($21 billion) of additional tax reductions including one for vehicle purchases. Li also called on officials to ensure unemployment falls and the economy “operates in a reasonable range” in the second quarter of this year, but with covid restriction still in place, a materlai rebound in China’s economic activity looks limited.

China covid news remain a concern , Beijing capital reported 47 new Covid cases for Tuesday, compared with 48 on Monday and 99 on Sunday, the highest of the current outbreak. While the numbers are still low, Beijing has been recording several dozen infections a day for the past month, suggesting mass-testing drives, work-from-home orders in some districts and other Covid Zero measures haven’t been enough to extinguish the outbreak. Meanwhile while the nearby port city of Tianjin locked down its city centre amid a simmering flareup. The lockdowns in China are part of the growing narrative around the risk of a global recession.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.