Price growth edges lower despite reasonable economy

Insight

Markets in the US and Asia buoyed by news that a deal between the US and China was close.

https://soundcloud.com/user-291029717/markets-fizzle-on-false-hope

An hour ahead of the NYSE close, US stocks have reversed all of Friday’s gains and then some, the S&P an NASDAQ currently off by about 0.5% and the Dow by 1% (albeit losses for the former were closer to 1% an hour ago). Friday’s moves themselves still remain something of a mystery coming on the heels of the softer than expected US manufacturing ISM release and which offered some further evidence that US tariffs on China are hurting the US just as much as they are China.

In this respect, Bloomberg is reporting on two separate papers published over the weekend where some of the world’s leading trade economists declared Trump’s tariffs to be the most consequential trade experiment seen since the 1930 Smoot-Hawley tariffs blamed for worsening the Great Depression. They also found the initial cost of Trump’s duties to the U.S. economy was in the billions and being borne largely by American consumers (not by China, as Trump continues to claim).

This then makes today’s sell off all the more mysterious in so far as it comes in the midst of the news published at the start of our day Monday suggesting that a Sino-US trade deal was almost done and could be signed off by Presidents Trump and Xi later this month. This produced a decent risk rally across all equity markets during the APAC session yesterday (including a 0.5% jump in the S&P futures) but the New York market moves are now being read as proof that a trade deal must surely now be fairly fully priced?

We have some sympathy for this view, though wouldn’t underestimate Mr. Market’s ability to discount the ‘same news twice’ if and when a deal is done in. In this respect, one still-nagging doubt on a trade deal surrounds Huawei, where the apparent response to the weekend news that Canada has agreed to extradite the Chinese technology behemoth’s CFO to the United States, has been to accuse the two Canadians detained by China last month soon after the arrest of the Huawei CFO of spying.

Possibly of some relevance to the weaker equity tone is the soft US Construction spending release at -0.6%, though this is for December so of more relevance to possible downward revisions to Q4 GDP than what is says about Q1 (where the current ‘Nowcast’ models are – at this early stage – not painting a particularly pretty picture though will of course be reflecting the impact of the US government shutdown that lasted through January).

As for the 3%+ surge in the Shanghai Composite yesterday (but where gains were reduced to little over 1% by the close) it’s probable that speculation of new economic stimulus measures to be unveiled at this week’s National People’s Congress, may have had a hand. We’ve learned overnight that one such announcement could be a 3% cut to the VAT rate, a move some economist are suggesting could be worth some 0.6% of GDP; it would provide a significant boost to flagging Chinese corporate profitability.

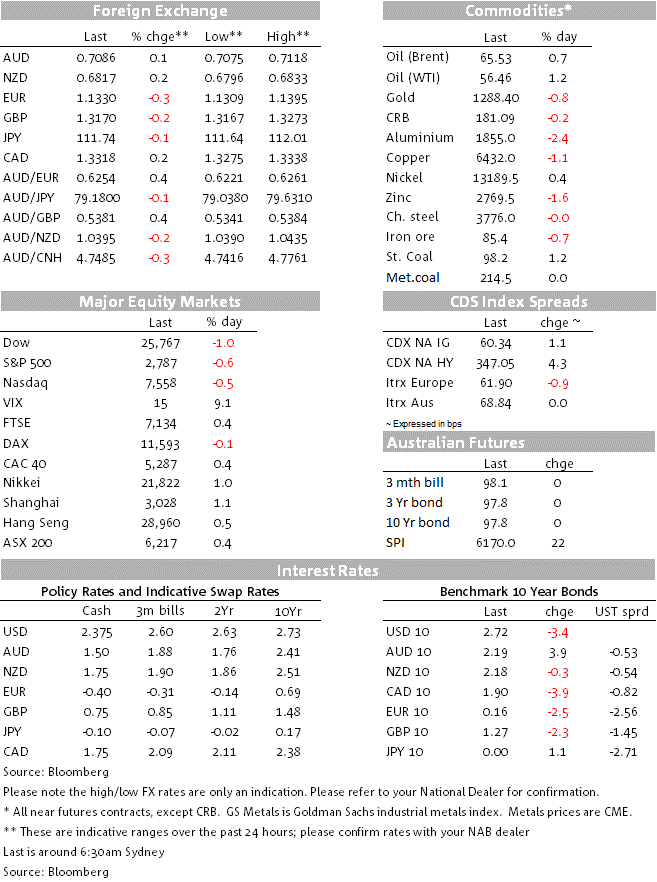

In FX, there’s not a lot of rhyme nor reason to what is a fairly disjointed set of moves across the G10 currency spectrum. The USD is overall a touch stronger which is consistent with it being a ‘risk off’ offshore session so far; then again the USD was stronger on Friday alongside higher stocks with higher US bond yields blamed but which are lower today – go figure! Seeing the AUD, NZD and JPY as the only three G10 currencies to be stronger versus the dollar sums up the difficulty of succinctly characterising FX moves of the last 24 – or rather 48 hours.

What we can say about the AUD is that yesterday’s early day-run up on the positive Sino-US trade deal was subsequently undermined by the domestic data flow – softer than expected inventories numbers which prompted some downward revisions to estimates for tomorrow ‘s GDP numbers (see Coming Up below). Our FX traders continue to flag 0.7050 as an important level which if broken portends further weakness.

Bond markets are seeing Friday’s yield back-up largely reversed, so US 10-year Treasuries down 3.5bps 2.72%, having been up by almost 4bp Friday. The 2-year yield is 1bp lower. Our 3-year futures are up 3 ticks on the day-session close ahead of this morning’s net-exports data and this afternoon’s RBA meeting outcome. Earlier, European 10-year bond yields fell on average of 2bps. News that German public sector workers have secured an 8.8% pay rise to be spread over the next 3 years – so roughly twice the current rate of inflation – is something that can help bolster confidence in a somewhat stronger domestic demand story for the German economy going forward, but doesn’t appear to have had any market impact. Do though expect the ECB to play this up when it meets on Thursday.

Not too much to say about commodities, where iron ore and most non-ferrous metals are lower, as is gold, but oil prices are 50-70- cents higher. See table below.

Australia’s Q4 balance of payments data at 11:30 AEDT, including an estimate of the net exports contribution to GDP, and government finances, provide the last GDP partials ahead of Wednesday’s GDP figures themselves. Watch out for further revisions to market estimates post these numbers (NAB is currently at 0.4% with downside risk, current consensus 0.5%). There were a few downward revisions filtering in to the survey lists on Monday, though not yet sufficient to lower ‘official’ news agency survey medians. NAB will only decide whether a revision is warranted post today’s data.

The RBA’s post-meeting statement at 2:30 AEDT will be very closely parsed. The last paragraph is unlikely to change much if at all from what has, in the past twelve months, been a studiously neutral affair and carbon copy of the February 2018 statement. There will though be keen interest in word changes elsewhere, in particular with respect to the housing market (about which Governor Lowe will give a speech on Wednesday morning). To date, the RBA has been noting that “the main domestic uncertainty remains around the outlook for household spending and the effect of falling housing prices in some cities”. No mention as yet at how the anticipated fall-off in residential investment could impact on employment in the sector (i.e. potential unemployment). Watch this space.

Internationally, focus will very much be on service sector PMI data. This included China’s Caixin version (12:45) seen at 53.5 from 53.6 (the official version fell to 54.3 from 54.7). The UK has its one and only vintage (expected at 50.0 from 50.1) and the Eurozone its final February editions. Then later tonight it’s the non-manufacturing ISM (expected 57.3 from 56.7) and also the Markit PMI version.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.