Price growth edges lower despite reasonable economy

Insight

There’s a risk on mood in the markets today.

https://soundcloud.com/user-291029717/markets-respond-to-a-glimmer-of-hope?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

If I don’t listen to the talk of the town, Then maybe I can fool myself…

‘Cause I’m the king of wishful thinking (king of wishful thinking) – Go West

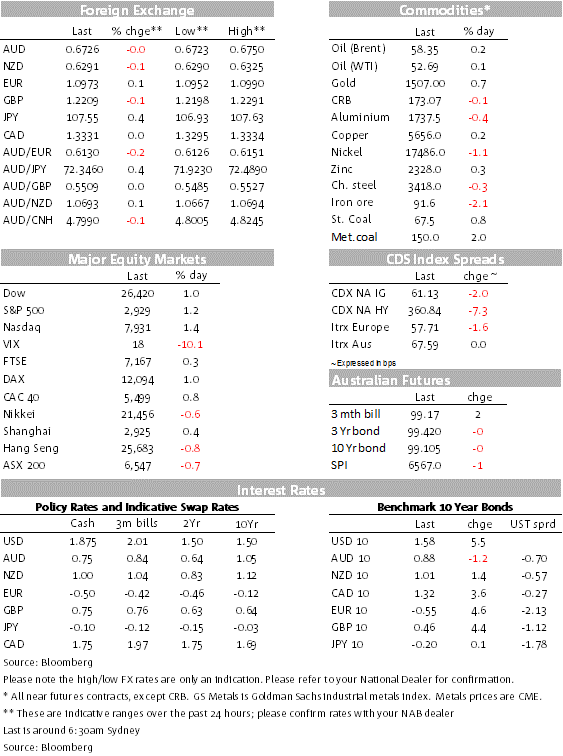

Risk assets had a good night on the back of news reports suggesting China is still keen on striking a partial trade deal with the US, notwithstanding recent US sanctions and blacklisting of Chinese companies and entities. UST yields edged higher with shorter dated tenors getting a mini boost post the FOMC minutes as a few officials saw the need to pushed back against market Fed rate cut expectations. Movement in G10 FX were very subdued with JPY and CHF weakness the only highlight.

After a long hiatus, following the collapse in negotiations in May, high level US-China trade talks are scheduled to resume today in Washington and China’s Vice Premier Liu He arrival in the capital city overnight has coincided with a flurry of headlines suggesting China is still keen on a partial deal which would entail buying more agricultural products, but without making any concessions on major sticking points such as protection of intellectual property and or a pullback in government subsidies for state firms. The FT, reported that China is offering to increase purchases of American soybeans to 30m tons annually from 20m presently ( basically back to pre-trade tensions levels).

Last month the idea of a partial deal was floated by some US officials comprising a delay and even the potential to roll back some US tariffs if China made some commitments on intellectual property and buying agricultural products. At the time, the news triggered a boost in risk sentiment, but the move proved short lived after President Trump expressed an aversion to the idea.

So the market either has a short term memory or it has high hopes President Trump could change its mind. Overnight news that China is keen on a partial deal that does not include any concessions on the key contentious issues has triggered a decent rally in EU and US equity markets. The STX Europe 600 index closed the day at 0.42% with IT (+1.37% ) and Consumer Discretionary (+1.09%) sectors leading the gains. Similarly in the US, the S&P 500 closed the day at +0.91% with IT (+1.46%), Materials (+1.08%) and Financials ( +1.03%) the big winners. The NASDAQ ended the day +1.02% and the Dow was +0.70%.

Markets jitters along with increasing evidence that trade tensions are contributing to the slowdown in US, China and global growth, suggest that not only the US but also China could benefit from making an interim deal. But making a soft trade deal carries the risk of triggering a strong political backlash ahead of the US elections next year. President Trump has sold himself as a deal maker and making a deal without gaining any concessions on key structural issues, is not only politically risky, it also means that it may not last very long. That uncertainty is unlikely to reverse the pullback in trade activity and Capex decision. Let’s see what the next two days bring.

The FOMC Minutes released early this morning didn’t elicit a big market move, other than a small uptick in shorter dated UST yields. The Fed Minutes revealed greater concerns over downside risk from slowing global growth and trade tensions with subdued inflation also seen as a reason to cut. But a few officials saw the need to pushed back against market Fed rate cut expectations. UST yields were already edging higher ahead of the release but the latter comment appears to have contributed to the small bear flattening evident later in the session.

Movement in FX have been remarkable subdued. The USD is little change in index terms ( DXY @99.12) and the AUD is unchanged relative to yesterday’s opening levels ( now at 0.6725) and the NZD is 0.09% lower, now trading at 0.6292. The AUD showed little reaction to yesterday’s news that Australian consumer confidence fell to a more than 4-year low – but it was interesting to note the lack of confidence despite tax rebates and three rate cuts.

Safe haven JPY ( USD/JPY -0.44 @ 107.56) and CHF ( -0.34%, 0.9961) lost a bit of ground amid the increase in risk appetite while the only currency with a bit of a pulse has been GBP. The Times reported that the EU was ready to a make a major concession over the contentious Irish backstop, seeing GBP spike up towards 1.23 but the DUP said that any demand to keep Northern Ireland inside the customs union after Brexit would be “beyond crazy”, seeing GBP fall all the way back down to its current level around 1.2215.

Turkey has begun a military offensive into north-eastern Syria, three days after President Donald Trump said the U.S. wouldn’t stand in the way. The TRY is the EM FX underperformer, down 0.57%

| September | NAB | Consensus | Previous |

| Headline m/m | 0.1 | 0.1 | 0.1 |

| Headline y/y | 1.8 | 1.8 | 1.7 |

| Core m/m | 0.1 | 0.2 | 0.3 |

| Core y/y | 2.3 | 2.4 | 2.4 |

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.