Price growth edges lower despite reasonable economy

Insight

There’s been a strong reaction in the equity and currency markets to Donald Trump’s sudden decision to stop talks about a fiscal stimulus, even though he tweeted about the need for it whilst in hospital over the weekend.

https://soundcloud.com/user-291029717/markets-take-a-hit-as-trump-ditches-stimulus-talks?in=user-291029717/sets/the-morning-call

Stop! In the name of love, Before you break my heart – The Supremes

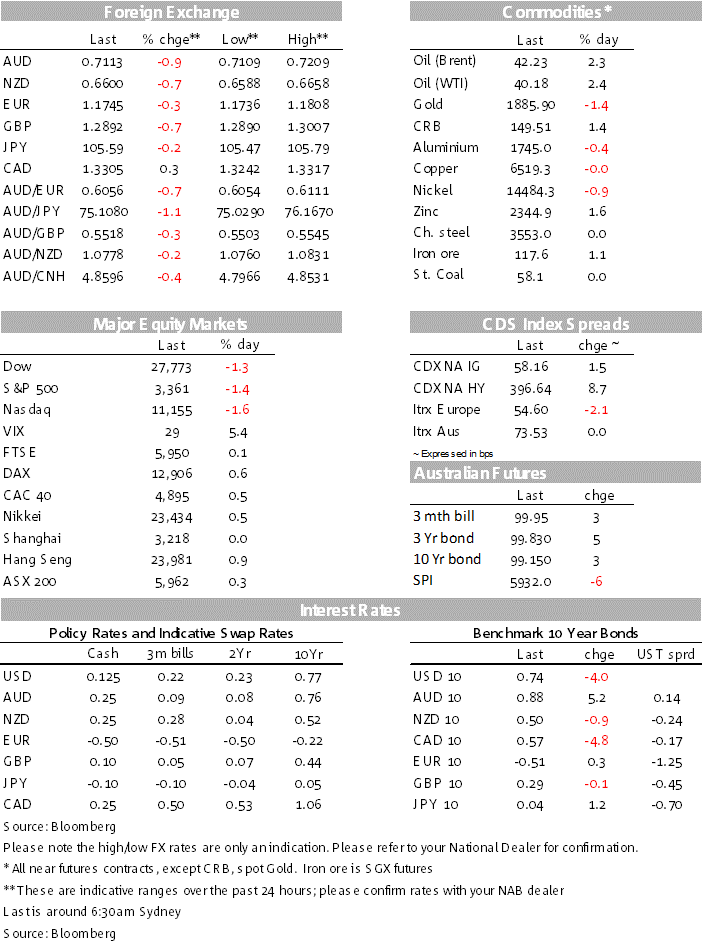

We have seen a big u turn in markets this morning following news President Trump’s has ordered his negotiators to stop stimulus talks with Democrats until after the elections. Before the news, equity markets were edging a little bit higher, but now all major US equity indices are down over 1.30%. The USD and UST yields have benefited from safe haven demand and the AUD is at the bottom of the G10 leader board amid the risk off environment and strong signal of RBA easing in November.

But around 5:50 this morning, all these positive vibes were erased in a matter of second following a series of Tweets from President Trump announcing that he had instructed his negotiators to stop stimulus talks with Democratic leaders until after the elections. Trump then added that “immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business,”.

In US equity markets with the S&P 500 down around 1.40% as I type while the NASDAQ is -1.57%. Early in the session, Fed Chair Powell warned about the risk of a weak economic recovery if there was no sufficient government support adding that “Too little support would lead to a weak recovery, creating unnecessary hardship for households and businesses, by contrast, the risks of overdoing it seem, for now, to be smaller. Even if policy actions ultimately prove to be greater than needed, they will not go to waste.”.

History tells us that the state of the economy is a big factor that can determine election outcomes, going into an election with a weakening economy more often than not means Presidents don’t get re-elected. Of course there is a blaming game going on here and whether Trump can convince the electorate that this is not his fault, but the Democrats, it remains to be seen. In recent days the market was travelling with increasing hopes that a new round of stimulus was in the offing, Trump’s halt in negotiations could be a last minute bargaining tactic (a move from the art of deal making?), but if Democrats don’t budge, then who ever is elected in November is likely to be facing a weakening US economy with an urgent need of fiscal support.

The broad risk off move in equity market has triggered safe haven demand in currencies with the USD stronger mostly stronger with JPY the only currency outperforming the greenback. DXY is up 0.13% to 93.68 and BBDXY +).34% to 1173.78. AUD (-0.90%) and NZD(-0.60 ) are closer to the bottom of the G10 leader board currently trading at 0.7113 and 0.6600 respectively. In addition to the risk off environment the AUD bigger underperformance can also be attributed yesterday’s RBA policy meeting outcome. As expected by most the Bank left its policy levers unchanged, but it also provided strong signals that further easing should be expected in November adding in its final paragraph that it “continues to consider how additional monetary easing could support jobs as the economy opens up further”, emphasising the point that reducing unemployment is an “important national priority”. NAB expects the RBA to cut rates – the cash rate target, 3-year yield target and TFF (Term Funding Facility) rate to 10 basis points – at its next meeting in November as well as introduce QE targeting purchases of longer-dated (five to 10 year) government bonds.

The government announced a range of new policy measures, mostly flagged already through media leaks, including the bringing forward of income tax cuts. The deficit is forecast to be a whopping 11%/GDP issuance in the current 2020/21 fiscal year and bond issuance will be a bit higher than previously projected (although the Australian Treasury is already ahead of the run-rate for issuance, so this shouldn’t have much impact on the bond market). See attached note for more details.

The euro is 0.20% weaker at 1.1743%. Early in the session, dovish remarks from ECB President Lagarde and chief economist Lane did not have much impact on the currency. Lane expressed concern that low inflation expectations could be entrenched, in turn reducing the room for manoeuvre with monetary policy, noting that “the less costly and more prudent approach is to add sufficient extra monetary policy accommodation”. Lagarde told the WSJ that the recovery “looks a little bit more shaky”, while observing that the ECB was “not the only game in town anymore”, with fiscal policy playing a greater role. The market expects the ECB to announce more bond buying later this year.

GBP has been a little bit more volatile with the pair now down 0.6% to 1.2902. Bloomberg reported that EU will not make concessions ahead next week’s EU Summit. UK PM Johnson had previously marked out this date a deadline to get a deal done, although he recently softened his stance on this. Brexit negotiators are currently engaged in “intensive” talks, although with little sign of a breakthrough yet. Commentators.

The u turn in risk sentiment following the halting of US stimulus talks has triggered a bull flattening in the UST curve with the 30y bond down 4.4bps to 1.547% while the 10y Note is down 4bps to 0.744%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.